It has been four years since the Shanghai-Hong Kong Stock Connect was officially launched on November 17, 2014.

Over the past four years, what is the development of the Shanghai-Hong Kong Stock Connect, what are its interesting characteristics, and what new changes have it brought to the cross-strait market? Let's review it together.

1

Overall changes in the Shanghai-Hong Kong Stock Connect

Since the opening of the Shanghai-Hong Kong Stock Connect, as said by Li Xiaojia, chief executive of the Hong Kong Stock Exchange, the Shanghai-Hong Kong Stock Connect system has been operating smoothly over the past four years, constantly optimizing and improving, continuously promoting the integration of the mainland and Hong Kong markets, and winning the favor of domestic and foreign investors. the continuous growth of turnover has brought new liquidity and investment choices to both markets.

Data show that as of November 16, 2018, the Shanghai-Hong Kong Stock Connect has a cumulative turnover of 10.31 trillion yuan over the past four years. Among them, the Shanghai Stock Connect has a total of 930 trading days, with a trading amount of 6.05 trillion yuan, with an average daily trading amount of 6.502 billion yuan, while the Hong Kong Stock Connect has a cumulative total of 912 trading days, with a trading amount of 4.27 trillion yuan and an average daily trading amount of 4.677 billion yuan.

Since the end of March this year, the trend of northward capital inflows into the A-share market has become increasingly obvious, with a cumulative inflow of about 150 billion yuan, demonstrating the confidence of foreign funds in the A-share market.

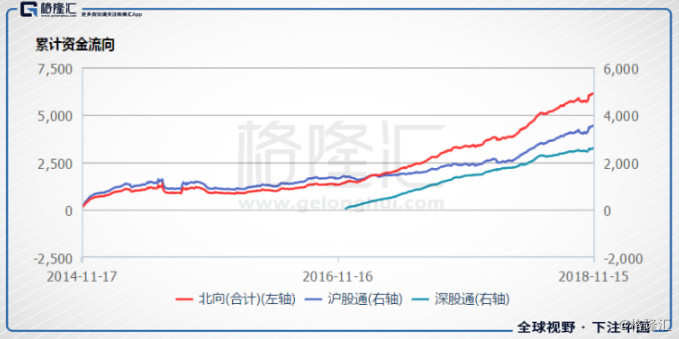

At the same time, data show that as of November 16, the cumulative net inflow of northbound transactions (including Shanghai Stock Connect and Shenzhen Stock Connect) under the Shanghai-Shenzhen-Hong Kong Stock Connect was 615.664 billion yuan, and the inflow trend accelerated again in the second half of the year. Of these, the total net inflow since the opening of the northbound Shanghai Stock Exchange was 356.092 billion yuan, accounting for 41.6% of the total net inflow. In June this year alone, the net inflow reached 103.535 billion yuan, accounting for 29% of the total net inflow of the channel. Since the opening of the Shenzhen Stock Exchange, the net inflow was 259.573 billion yuan. Since June this year, the net inflow is 59.556 billion yuan, accounting for 22.9%.

(source: wind)

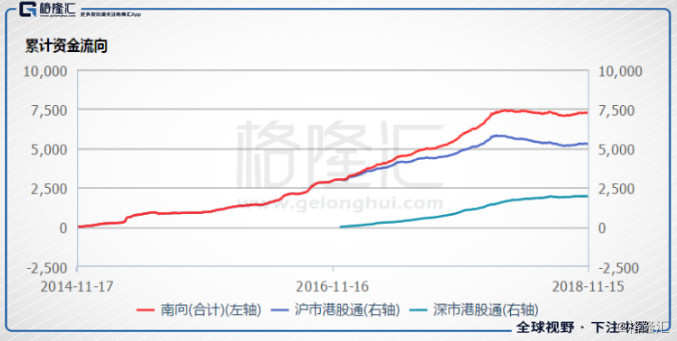

The cumulative net inflow of southbound trading (Hong Kong Stock Connect) is 727.523 billion yuan, but there has been a net outflow of 9.945 billion yuan since June this year, showing an outflow trend. Of these, the cumulative net inflow of the Shanghai-Hong Kong Stock Connect was 532.291 billion yuan, accounting for 73.16% of the total inflow, with a net outflow of 28.335 billion yuan in recent June; and the cumulative net inflow of 195.232 billion yuan since the opening of the Shenzhen-Hong Kong Stock Connect, but contrary to the Shanghai-Hong Kong Stock Connect, in recent June, Shenzhen Hong Kong stocks had a net inflow of 18.39 billion yuan.

(source: wind)

In addition, northbound trading recorded the highest trading volume since the opening of the Shanghai-Shenzhen-Hong Kong Stock Connect on November 2, 2018, with a total of 42.803 billion yuan in buying and selling on that day, while the record for southbound trading occurred on February 6, 2018. the combined turnover of buying and selling on that day reached HK $43.801 billion.

(data as of November 15, photo source: HKEx website)

From the perspective of the industry of the Shanghai-Hong Kong Stock Connect, as of the latest data, as the company targets mainly mature listed companies under the Shanghai-Hong Kong Stock Connect mechanism, there is little difference between the two cities.

Up to now, the industry average PE and average PB of Shanghai-Hong Kong Stock Connect companies in the two markets are not very different. Due to the continuous decline of the two stock markets in recent years, the average PE of the two stock markets is mainly in the range of 10-20 times, and the PB is also mostly in the range of 0.9-1.6. the overall valuation level is more reasonable.

(source: wind)

In addition, in 2018, the Shanghai-Hong Kong Stock Connect experienced three major events: the expansion of the daily quota, the inclusion of A-shares in the global index system, and the launch of the northbound investor identification code system.

On April 11, 2018, Yi Gang, governor of the people's Bank of China, announced at the Boao Forum for Asia that the daily quota of the Shanghai-Hong Kong Stock Connect would be quadrupled from May 1. On the same day, the China Securities Regulatory Commission and Hong Kong Securities Regulatory Commission issued a joint announcement that the daily quota of the Shanghai Stock Connect was adjusted from 13 billion yuan to 52 billion yuan, and the daily quota of the Shanghai-Hong Kong Stock Connect was adjusted from 10.5 billion yuan to 42 billion yuan. Effective from May 1st. The substantial expansion of the daily quota is a further deepening of the interconnection mechanism, expands the two-way opening of the mainland capital market, better meets the investment needs of investors in the two places, and plays a positive role in helping A-shares to be smoothly included in the MSCI index and maintaining the smooth operation of the market.

After the close on May 31, 2018, 226 A-shares were officially included in the MSCI emerging Markets Index, with an inclusion ratio of 2.5%. After the close on August 31, 10 A-share constituent shares were added and the inclusion ratio was increased to 5%. In addition, on September 27th, FTSERussell announced that A shares would be included in its global stock index system, which will take effect from June 2019. The successful inclusion of A-shares not only reflects the affirmation of foreign investors on the achievements of China's capital market reform and opening up, but also expresses their confidence in the future development prospects of China's capital market. The inclusion of A-shares in the global index system will promote more international investment funds to flow into China's capital market, improve the investor structure, and further improve the internationalization level of the A-share market.

On September 26, 2018, the northbound penetration mechanism of the Shanghai-Hong Kong Stock Connect was officially launched, and the northbound transaction declaration front-end control function based on investor identification number was officially launched on October 22 to reject orders for transactions that do not meet the requirements. The Shanghai-Hong Kong Stock Connect system not only attracts foreign capital, but also brings a test for market supervision. Today, with both opportunities and challenges, the establishment of the northward penetration mechanism will help the Shanghai Stock Exchange to give full play to its first-line regulatory functions, improve the cross-border regulatory cooperation mechanism, and crack down on illegal activities such as cross-border market manipulation. maintain the stable operation of the A-share market and provide a good market environment for investors at home and abroad.

2

Which stocks are being bought and sold by northbound funds?

According to wind statistics, since the opening of the Shanghai-Hong Kong Stock Connect, Guizhou Moutai, Ping An Insurance, Midea, Yili shares, Gree Electric Appliances, Anhui Conch Cement, Wuliangye and other large white horse shares have topped the list in northbound trading. The main characteristics of this kind of stocks are stable performance, definite growth, reasonable valuation, industry leader and other characteristics, indicating the relatively sound and rational investor style of overseas institutions and investors.

The following are the top 10 stocks traded by northbound funds of the Shanghai-Hong Kong Stock Connect over the past year, of which Ping An Insurance, Wuliangye, Guizhou Moutai and Wuliangye all bought more than 13 billion yuan this year, while Qingdao Haier topped the list with a net sale of 2.124 billion yuan. the following are Shanghai Airport, Industrial Bank, Baiyun Airport, Haitian flavor industry and other blue chips.

3

What stocks are southward funds buying and selling?

From a statistical point of view, southbound funds under the Shanghai-Hong Kong Stock Connect channel mainly favor large companies with unique and high quality in the Hong Kong stock market, such as Tencent, HSBC Holdings PLC, Sunac China, HKEx, Geely Automobile, Sunny Optical Technology, AAC Technologies Holdings Inc., and so on. at the same time, they are also keen to buy and sell high-quality stock markets in A + H shares, such as major bank financial stocks.

These stocks have been at the top of the top 10 trading list for a long time, with mainstream hot stocks dominating the list almost all the time, and only a few trading days have a stock on the list because of special events.

Judging from the southward fund trading stocks for nearly a year, HSBC Holdings PLC topped the list with a net purchase of 35.646 billion yuan, Industrial and Commercial Bank of China ranked second with a net purchase of 23.207 billion yuan, and the net purchase amount of the second echelon was far less than that of Foreign Exchange Control and ICBC. Sunac China, who bought the most net, was only 3.391 billion yuan. In the list of sellers, Tencent became the company with the largest net sales due to the slowdown in performance this year, with a net sales of 12.66 billion yuan, almost equal to the total net sales of the last nine companies. Ping An Insurance also ranked second with a net sale of 5.104 billion yuan.

In fact, if you look at the end of 2017, if it were not for the continuous decline in the A-share Hong Kong stock market this year, the list would have changed dramatically. Tencent should be the company that investors bought the most, and Ping An Insurance's data would also be very good-looking. AAC, Shunyu and other companies are also likely to enter the top 10 net buyers.

4

The premium of A + H shares has not been significantly repaired.

Before the opening of the Shanghai-Hong Kong Stock Connect, the AH premium index was already in operation and fluctuated obviously. The AH premium index rose to an all-time high of 213.47 before the 2008 crash, but repaired as A-shares fell back in the following years and fell back to a low below 90 in mid-2014.

After the opening of the Shanghai-Hong Kong Stock Connect, the ah-share premium of the two markets did not have the obvious repair effect imagined by investment, and at one point in the month of opening, it quickly took advantage of the bull market to push up the high of nearly 150 again.

(source: wind)

As of November 16, under the Shanghai-Hong Kong Stock Connect channel, of the 580 Shanghai Stock Connect, 59 companies still have an A-share premium of more than 30%, and 10 companies have an A-share premium of 20% and 30%.

(source: wind)

The A-share premium rate of 22 stocks is more than 100%. Luoyang Glass tops the list with an AH premium rate of 516.82%. Zhejiang Shibao, which has been discussed by the market for many years, still has a four-fold premium, and the changes since the opening of the Shanghai-Hong Kong Stock Connect have not changed much.

However, judging from the changes in the premium of individual stocks, there are also some divergences:

First, the A-share premium of most of the long-standing AH shares has indeed fallen, and this part of the company is generally reasonable in valuation, mature in business and financially sound. However, the A-share premium of many companies has not changed much with the opening of the Shanghai-Hong Kong Stock Connect.

Second, some companies with obvious AH premium expansion after the opening of the Shanghai-Hong Kong Stock Connect, especially those in advanced industries with relative concepts.

Third, the A-share premium in the AH premium is highly related to the overall market environment. At the same time, the A-share premium found in H-share A-share market is due to the speculation of new shares, which often leads to the rapid opening of the premium for a period of time.

5

Conclusion

Shanghai-Hong Kong Stock Connect is a policy launched under the background of China's gradual opening up of the capital market and the internationalization of RMB. From a market point of view, it does show the significance of very successful interconnection. At the same time, from the operation of the fourth anniversary of the Shanghai-Hong Kong Stock Connect, it has also brought a lot of reference significance to investors, including the logic of capital layout, investment values and so on.

Judging from the recent trend of increasing northward capital inflows, A shares are indeed favored by overseas investors, and whether the next market is really going to usher in a wave of market, let's wait and see.