Authors: Jiang Chao, Yu Bo, Chen Xing

Source: Jiang Chao Macro Bond Research

Abstract

The economic start was weak in November. Terminal demand is still low, real estate sales growth is still dragged down by the decline in third-and fourth-tier cities, while passenger car wholesale and zero sales growth is still bottoming out. It is difficult to say that industrial production has improved, and the operating rate of iron and steel blast furnaces continues to rise, but it is mainly due to the loosening of environmental protection policies. the operating rate of chemical and other industries that are not restricted by environmental protection production is still on the low side, while the reduction of coal consumption for power generation has narrowed, but it is also mainly due to the low base last year.

The economy is still bottoming out in October, especially when consumption growth hit a staggering low. Of course, this is related to the dislocation of the Mid-Autumn Festival holiday and the postponement of the release of demand during the "Singles Day", but the trend decline in consumption growth this year is still an indisputable fact, essentially due to the weakening purchasing power brought about by residents' leverage to buy houses combined with the economic downturn. We believe that stimulating consumption still needs a two-pronged approach. While raising residents' income through individual tax reform, we should also start from the price side to promote VAT relief, so as to reduce residents' consumption costs and encourage consumption!

Demand: downstream real estate, passenger cars, home appliances, textile clothing are weak, cultural and recreational improvement. In the middle reaches, steel and cement are stronger, while chemical industry is weaker. Upstream coal differentiation, non-ferrous stronger. The transportation is not bad.

Price: the year-on-year increase in house prices in 70 cities expanded in October. Last week, domestic raw capital prices rose and fell, while international oil prices fell.

Inventory: removal of downstream real estate, replenishment of passenger cars. In the middle reaches, steel and cement are demineralized, and chemical industry is replenished. Upstream coal is flat and non-ferrous.

Downstream industries:

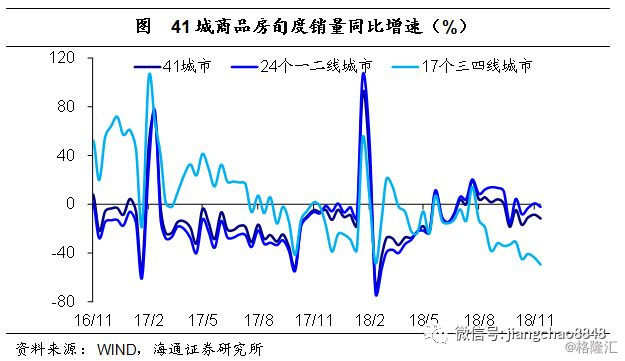

Real estate: the increase in house prices in 70 cities expanded in October, and real estate sales in 41 cities split in the first ten days of November. Against the backdrop of a low base in the same period last year, the decline in national property sales narrowed only slightly to 3.1 per cent in October, pointing to still low demand. The loan rate for the first suite in the 35th city rose to 5.71% on October. In October, the year-on-year increase in house prices in 70 cities widened to 9.7%, mainly due to the expansion of house prices in second-and third-tier cities. In the first ten days of November, the growth rate of 41 urban land production and sales slowed to-9.9%, of which sales in third-and fourth-tier cities continued to weaken, while sales in first-and second-tier cities stabilized, and real estate inventories in ten major cities were removed again, and the inventory-to-sales ratio fell to 40.5 weeks. Last week, the land market transaction was still deserted, and the growth rate of land transaction was still declining.

Passenger cars: the growth rate of automobile production and sales was low in October, and the inventory of dealers reached a new high in the same period. In October, the growth rate of national automobile production narrowed slightly to 9.2%, the growth rate of retail sales of cars above the quota narrowed to 6.4%, and the passenger car sales of the China Automobile Association and the Federation of passengers both grew by-13%. Under all caliber, automobile production and sales are basically the same as in September, and are still at a low level. In October, the inventory coefficient of automobile dealers rose to 1.88, a new high, pointing to no improvement in terminal demand and passive replenishment of channel inventory. In the first week of November, zero growth continued to fall to-38% and-41%, meaning demand may not have bottomed out. The continued downturn in early demand has led manufacturers to operate cautiously. Manufacturers' inventories have been eliminated for two consecutive months, and the production side has also begun to recover slowly. The operating rate of semi-steel tires has continued to pick up since October, and the operating rate of semi-steel tires rose to 69.9% last week.

Home appliances: the growth rate of retail sales of home appliances above the quota slowed down in October, and demand slowed down. In the case of a low base in the same period last year, the audio-visual growth rate of above-quota retail home appliances fell back to 4.8% year-on-year in October, pointing to a marked slowdown in demand. Over the past 18 years, the growth rate of audio-visual retail of home appliances has been high before and low after, with a monthly growth rate of less than 6% in the second half of the year, lower than the low growth rate in the first half of the year. Under the background of residents' purchasing power overdraft, the trend of audio-visual consumption of home appliances has become a microcosm of the overall trend of consumption.

Textile and clothing: the retail growth rate above the quota hit a new low in October, with both internal and external demand weakening. The growth rate of retail sales of clothing, footwear and hats above the quota fell back to 4.7% in October from a year earlier, the lowest since April 16. On the one hand, the base rose slightly in the same period last year, but on the other hand, more importantly, the slowdown in growth may be related to the delay in consumer demand during the "Singles Day". In October, the export growth rate of the textile and clothing sub-industry rose less and fell more, pointing to the simultaneous weakening of internal and external demand.

Trade and retail: retail growth hit a new low in October, and necessary consumption generally fell sharply. In October, the growth rate of retail sales above quota fell to 8.6% and 3.6% respectively compared with September. Excluding oil, building materials and cars, the year-on-year growth rate was only 4.7%. Consumption growth declined across the board and hit a new low. By category, the growth rate of necessary consumption generally declined sharply in October, mainly due to the impact of the wrong month during the Mid-Autumn Festival holiday and the delay in the consumption of some commodities before the "Singles Day", while optional consumption rose less and fell more. From January to October, the growth rate of online retail sales of physical goods was 26.7% compared with the same period last year, although it also declined, but it remained high and the proportion remained stable.

Sports and entertainment: last week, the box office attendance of the film both rebounded from the same period last year, and demand picked up somewhat. Last week, the growth rate of box office revenue and cinema attendance rose to 55% and 48% compared with the same period last year, while the month-on-month growth rate also rose to 135% and 120%, mainly due to a decline in the base in the same period last year and a pick-up in demand due to the release of excellent films. Last week, the box office of the film focused on the head, and "Venom" topped the box office with about 770 million of weekly box office receipts, while other films grossed less than 100 million yuan.

Mid-stream industry:

Iron and steel: October crude steel production and sales double rise, inventory elimination, steel prices fell last week, start up. In October, the growth rate of crude steel output of the whole country and key steel enterprises rose to 9.1% and 7.3% respectively, and the apparent consumption of crude steel increased by 14.4%. With the simultaneous increase in output, the average weekly blast furnace operating rate also rebounded significantly compared with September, and last week the blast furnace operating rate rose to 67.7%. Pointing to the marginal relaxation of environmental protection policy, supply and demand have improved. The improvement in demand has also led to the elimination of both steel enterprise inventory and social inventory. Last week, steel price thread, hot plate fell, steel prices downward, rising costs per ton of steel gross margin has also declined.

Cement: the average national cement price continued to rise last week, and the storage-volume ratio is still bottoming out. Last week, the average national cement price continued to rise, the month-on-month growth rate dropped to 1%, and the storage-volume ratio continued to fall to 48.3%, a new low for the year. In mid-November, there was rainy weather in some parts of the south, but due to the continuous rush of downstream projects, the overall demand was relatively stable, and at the same time, affected by off-peak production and environmental production restrictions, the supply was slightly insufficient, and enterprises continued to push cement prices upward. In view of the good relationship between supply and demand in the market, and local enterprises still have plans to push up, we expect cement prices to rise steadily in the later stage.

Chemical industry: the price of PTA industry chain fell last week, and the inventory number of polyester POY reached a new high. Last week, the prices of PTA industrial chain products generally fell, and the industry boom continued to decline. Weaker demand has led to passive replenishment of polyester POY inventories. Last week, polyester POY inventory days continued to rise to 17 days, a new high for the year and a new record for the same period of the year. Last week, the load rate of the PTA industry chain rose less or lower, while only the PTA factory rebounded. The weak pattern of supply and demand in the industry has not changed.

Electricity: the growth rate of power generation rebounded in October, and the decline in coal consumption narrowed in the first half of November. The growth rate of electricity generation rebounded slightly to 4.8% year-on-year in October, but it is still at the low point of the year, confirming that the growth rate of industrial value added has rebounded slightly and is weak. The growth rate of coal consumption for power generation among the six major groups in the first half of November was-10 per cent, a decline significantly narrower than that in October, but mainly due to a low base in the same period last year, with the growth rate of coal consumption for power generation plummeting to 1.8 per cent in November from 16.5 per cent in October. Given that demand is still low and profits are at their peak, industrial production is still hard to improve.

Upstream industry and transportation:

Coal: last week, coal prices rose and fell evenly, the inventory of power plants was eliminated, and the inventory of steel mills flattened. Coal prices rose and fell evenly last week, among which coal prices in Qinhuangdao Port rebounded. In the first half of November, the year-on-year growth rate of coal consumption for power generation in the six major groups narrowed slightly, but the rebound was still weak mainly due to the influence of a low base. Last week, the number of days of coal stocks in power plants fell to 33.2 days, pointing to slightly destocking, but still at the highest level of the year. The operating rate of blast furnace rebounded slightly last week, while the inventory of coking coal in steel mills remained flat at 14.2 days.

Non-ferrous: LME copper and aluminum prices rose last week, copper and aluminum stocks are both replenished. The prices of base metals were mixed last week. The trade dispute between China and the United States sent a positive signal, and the dollar index fell slightly, pushing the average price of copper higher. A Brazilian judge upheld Hydro's ban, Alunorte was unable to restore full capacity, the market was tight and aluminum prices rebounded last week.

Commodities: crude oil prices fell last week, the CRB index rose slightly, and the dollar index fell. Crude oil prices fell sharply last week, thanks to a rapid rebound in shale production, US crude oil production hit a new high, and EIA also raised its forecast for US crude oil production for 18 and 19 years. The average price of CRB rose slightly last week. Last week, the trend of the dollar was high before and after, the average value fell, and the dust of the US mid-term elections settled, basically in line with market expectations.

Transportation: the growth rate of highway freight volume and foreign trade cargo throughput both rebounded in October. The growth rate of road freight volume rebounded to 10% year-on-year in October, confirming that the growth rate of industrial value added has rebounded slightly. In October, the growth rate of cargo throughput of the country's major ports slowed to 6.3%, but the growth rate of foreign trade cargo throughput rebounded to 3.5%, confirming that export growth continued to pick up in October. Last week, the performance of container transportation outperformed bulk transport, with the BDI index falling and the CCFI index rising. The index of road logistics freight rates rebounded last week.