Guide reading

When we mentioned that the central bank has a high probability of cutting interest rates, people generally question the exchange rate, inflation, house prices and so on. In fact, interest rates have always been one of our policy tools.

Abstract

President Yi's speech released five important messages, which further increased the probability of "interest rate cut" becoming an alternative monetary policy in 19 years.

If interest rates are cut in 2019, it will mark another asynchronous period of interest rate policy between China and the United States. Behind the policy decoupling is a cyclical mismatch superimposed by the impact of a trade war.

In the cycle of raising interest rates by the Federal Reserve, the monetary policy of the people's Bank of China has also cut interest rates. From 1998 to 1999, in the Fed's interest rate raising cycle, China cut interest rates twice in December 1998 and June 1999 respectively. That was the second of three strong dollar cycles since the 1970s (the three dollar appreciation cycles were 1980-1985, 1995-2001 and 2011 to the present).

At present, China is at the top of the super-financial cycle that began in 2009, while the United States is in the upswing of the financial cycle that began in 2013. The mismatched Sino-US financial cycle encounters a trade war, which has an extremely complex impact on the economy and policy. In the face of economic downward pressure and uncertainty, it is a general trend to "cut interest rates, cut taxes, and the central government increases leverage to speed up economic transformation".

Risk hint: domestic inflation (expectations) is rising rapidly, causing the currency policy anchor to give priority to curbing "inflation".

Text

Recently, President Yi Gang pointed out that "trade frictions bring great downside risks to the economy" and "there is still considerable room for monetary policy tools, including interest rates, reserve requirements and monetary conditions", which has aroused widespread concern in the market.

How on earth should this be understood? We believe that because of the relatively uncertain external environment and the delayed substantial improvement in the financing environment of domestic enterprises, the downward pressure on the economy in 2019 has increased, and it is imperative to cut interest rates and taxes, but the market is considering an increase in interest rates in the United States. China maintains its exchange rate stability, and it is generally believed that there is not much room for monetary policy, especially interest rates.

President Yi's speech further increases the probability that "interest rate cuts" will become a 19-year monetary policy option.

We believe that under the current capital account management and RMB exchange rate pricing mechanism, China's monetary policy has a certain degree of independence, and the policy operation of the central bank will be dominated by the Chinese economy. Sino-US monetary policy will be decoupled (the reduction of the reserve requirement is the first manifestation).

Therefore, with the increasing downward pressure on China's economy, it is only a matter of time for the central bank to cut interest rates (asymmetrically cut benchmark interest rates). We expect there is a higher probability at the end of this year and early next year-- there is a more obvious difference in the economic cycle between China and the United States. as a result, the monetary policies of the two countries will be decoupled sooner or later.

We understand that the "stability" of the RMB exchange rate should not be the unilateral exchange rate of the RMB against the US dollar, but the relative stability of the effective exchange rate or a package of exchange rate indices, as well as cracking down on speculative transactions that are too short the RMB.

In November 2017, we made a forecast that the combination of monetary policy in 2018 would be an "increase in open market interest rates (i.e. policy rates)" and "(targeted) reserve reduction". At that time and for a long time to come, the market thought the forecast was too strange and unlikely, but now it has been fully fulfilled.

Now we expect the central bank to cut reserve requirements and benchmark (asymmetrically) in the coming year, perhaps more than once. We are very confident about this. This forecast is still based on the judgment of the fundamentals of the global and Chinese economy.

I. five important information revealed by President Yi Gang

1. Judgment of economy and inflation: economic growth in 2018 is stable, and it is expected to achieve a growth rate of 6.5% or more. CPI is expected to be slightly higher than 2% in 18 years, and PPI is between 3 and 4%.

2. Views on the impact of trade frictions: trade frictions bring huge downside risks to the economy, and have an obvious structural impact on China's economy. We still sincerely hope to find a constructive solution based on the "multilateral" principle and "prepare for the worst".

3. Put forward four ways to solve the structural problems in China's economy. The principle of "competitive neutrality" is first mentioned to treat state-owned enterprises. (1) to speed up domestic reform and opening up to the outside world; (2) to strengthen the protection of intellectual property rights; (3) to consider treating state-owned enterprises with the principle of "competitive neutrality"; and (4) to vigorously promote the opening up of service sectors, including the financial industry.

Note: the principle of "competitive neutrality" was first put forward by the Australian government in the 1990s; the Organization for Economic Cooperation and Development (OECD) has formulated eight standards for its further development, such as "tax neutrality, regulatory neutrality, debt neutrality and subsidy constraints, and government procurement". There is a special chapter on the competitive neutrality of state-owned enterprises in TPP (Trans-Pacific Partnership Agreement).

4. views on Sino-US monetary policy: considering that the Federal Reserve is raising interest rates, the current level of interest rates in China is appropriate. The overall leverage ratio has stabilized in 17 and 18 years and is no longer rising rapidly; the basic purpose of cutting the required reserve ratio or introducing other instruments is to provide sufficient liquidity to the financial system; and other indicators such as M2 and the scale of social financing have grown moderately. The liquidity injected into the financial system is appropriate and the level of leverage will remain stable.

5. Views on the future monetary policy space: the current monetary policy remains sound and neutral, neither loosening nor tightening. In dealing with the risk of trade friction, there is still considerable room for monetary policy tools, which "includes interest rates, reserve requirements and monetary conditions". There will be no special policies to promote the internationalization of the RMB. "the basic balance of the current account is a good thing" and "do not deliberately seek a current account surplus". At present, cross-border capital flows are in a normal state. The recent progress in the internationalization of RMB is a market-driven process.

President Yi's speech further increases the probability that "interest rate cuts" will become a 19-year monetary policy option.

Second, why do we think that it is possible and probable to cut interest rates?

The main concern about interest rate cuts is that monetary policies between China and the United States are out of sync, and concerns about exchange rates, inflation and real estate prices may further lead to internal and external imbalances. We will discuss our logic below.

1. "interest rate" has always been one of our policy tools. In the process of all previous economic slowdowns, the central bank has opened a relatively loose monetary policy, including cutting reserve requirements and interest rates.

China has experienced the following several significant slowdowns in economic growth. The Asian financial crisis of 1998-1999, the global financial crisis of 2008-2009, the European debt crisis of 2011-2012, and the domestic economic restructuring of 2015-2016.

Reviewing the process of economic slowdown, we find that the central bank has opened a relatively loose monetary policy, which includes cutting reserve requirements and interest rates. (1) in the two years from January 1998 to the end of 1999, there were two reserve requirement cuts and four interest rate cuts; (2) in the four months from September to December 2008, the central bank cut reserve requirements four times and interest rates five times. (3) from the end of 2011 to July 2012, there have been three reserve requirement cuts and two interest rate cuts. (4) from the beginning of 2015 to March 2016, a total of 5 reserve reserve reductions, 5 directional reserve reductions and 5 interest rate cuts have been taken.

In all previous economic downturns, the effects of interest rate and reserve rate cuts are as follows: (1) the volume-M2 growth rate of money has rebounded significantly after the beginning of the easing policy; (2) the price-interest rate of money (interbank offered rate or R007). After the opening of the easing policy, there is a relatively obvious decline; (3) the monetary counterpart-credit growth (and broad social finance growth), it also rebounded significantly following the monetary growth rate. (4) loose monetary policy is the main driving force of economic recovery. However, the transmission time of loose monetary policy to the real economy is getting longer.

2In the cycle of raising interest rates by the Federal Reserve, the monetary policy of the people's Bank of China has also cut interest rates. From 1998 to 1999, in the Fed's interest rate raising cycle, China cut interest rates twice in December 1998 and June 1999 respectively.

Since 1989, Sino-US monetary policy has been roughly divided into four stages. From 1989 to 1992, China and the United States were in the channel of simultaneous interest rate cuts, while from 1993 to 2000, there was an obvious asynchronous period in Sino-US monetary policy. This period is also the three strong dollar cycles since the 1970s (1980-1985, 1995-2001, 2011 to the present). If interest rates are cut in 2019, it will mark another asynchronous period of interest rate policy between China and the United States. Behind the policy decoupling is a cyclical mismatch superimposed by the impact of a trade war.

At present, when China is in the decline of the financial cycle, there is an obvious mismatch with the rising financial cycle of the United States. The mismatched Sino-US financial cycle under the "strong dollar cycle" encounters a trade war, which brings greater impact and uncertainty to the market, while the impact on the economy and policy is more complex. Faced with the double pressure of trade war to strengthen the dollar cycle, it may be a general trend to "cut interest rates, cut taxes, and the central government increases leverage to speed up economic transformation".

3. How to treat the restriction of exchange rate and inflation on monetary policy?

(1) Exchange rate issue: in the case of strengthening capital controls and expanding the fluctuation range of RMB exchange rate, the central bank's interest rate policy is gradually decoupled from the Federal Reserve, dominated by the domestic economy, and it is feasible to maintain independence.

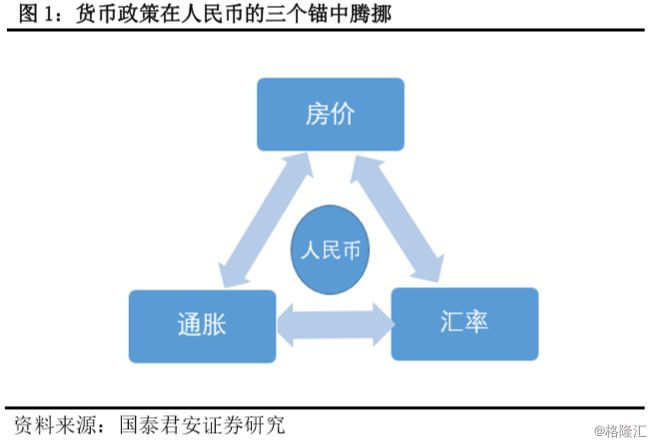

At present, monetary policy moves among the three anchors of RMB (figure 1): external currency price level: exchange rate; domestic general price level: inflation; special monetary anchor in the financial cycle: housing prices.

As far as the "skinny dipping" under the linked exchange rate system of Hong Kong is concerned, China's monetary policy has a "separation wall" constructed by capital controls and exchange rate management mechanisms. This is also the institutional basis on which China's monetary policy can be "decoupled" from the Federal Reserve under the trade war, at the expense of the internationalization of the exchange rate. In this speech, President Yi Gang also mentioned that "there will be no special policies to promote the internationalization of the RMB."

(2) inflation: monetary policy anchor "economic growth" is better than "inflation" in 2019.

First, the monetary policy goal of 2019 (that is, the monetary policy anchor will appear in the short term, "economic growth" takes precedence over the suppression of "inflation" (expected).

From President Yi Gang's speech, we will have a clear answer to this. President Yi did not show obvious concern about rising inflation expectations, instead emphasizing the "huge downside risks to the economy" caused by trade frictions. This shows that the monetary policy anchor in 2019 takes "economic growth" as the first goal. According to our estimates, if the tariff is implemented in 200 billion, it will affect GDP by more than 1.2 percentage points, that is, without policy hedging, the growth rate of GDP will be reduced to a range of 5% and 6% (refer to the special report "quantitative calculation of the impact of Trade War on China's GDP: based on two methods-the ninth series of Sino-US trade frictions").

Second, for our country, inflation is a stage pressure, and the more medium-and long-term risk comes from the breaking of the belief in housing prices and the "deflationary pressure".

(1) historically, inflationary debt crises occurred in countries with large foreign debts, while deflationary debt crises occurred in countries with large domestic debts.

Our current pressure on domestic debt is greater than that on foreign debt. The internal cause of debt risk is the breaking of the belief in "currency". Debt crisis occurs when monetary policy is "passive" tightening, that is, debt crisis often occurs when monetary policy is powerless.

From the point of view of the three anchors of "currency", the falling exchange rate and inflation will break the belief in "currency". The two inflation is linked and occurs in economies with large foreign debts, resulting in an inflationary debt crisis. For example, in resource-based emerging economies, currency depreciation → capital outflows → inflation. In an economy with a large amount of foreign debt, the debt crisis occurs when creditors (foreigners) stop borrowing. Real estate is an important channel for internal currency (credit), and the belief in "house price" is a part of monetary belief. The breaking of the belief in monetary anchor is likely to lead to deflationary debt crisis. For an economy with a lot of domestic debt, the pressure of "passive" tightening of monetary policy comes more from the absence of an opening or channel to absorb money (credit), that is, the "push rope effect" occurs. The debt crisis occurs when debtors (ordinary people, enterprises, local governments) do not dare to borrow, and the trigger is that the expectation of "house prices" is broken.

(2) in the case of weak demand performance, cost factors push up inflation, which is a typical feature of stagflation. However, the change in the output gap brought about by the downward pressure of the economy will have an important moderating effect on the inflationary pressure.

We estimate that the cumulative elasticity of CPI to the output gap is about 1.96, referring to the special report "exploring the Seven contexts of inflation Trends". Geopolitics push up oil prices and pig prices push up food prices, which puts upward pressure on inflation, but cost-driven stagflation is a disturbing factor. At the same time, we find that CPI has the greatest elasticity to the output gap.

4. As far as monetary policy tools are concerned, it is expected that the simultaneous implementation of "interest rate cut" and "large water release" (wide credit) in 2019 is less likely, and the high probability is "reserve rate reduction + interest rate reduction + moderate credit".

Since 2018, we can see that under the "broad currency", M2 growth has stabilized and interest rates have fallen, but social finance growth shows no sign of stabilizing. Before July 2018, it was still in a state of "broad money-tight credit". It is necessary to change to "moderately broad credit" in the follow-up. Why do we think that the probability of simply "releasing water" is low?

Because under the simple "broad credit", the strength of the economy should rely more on local governments, enterprise departments, and residents to add leverage, and so on. Obviously, this part of the space is relatively small at present. The current policy logic mainly depends on the central government plus leverage. By cutting interest rates, monetary policy can better hedge against the crowding-out effect of fiscal policy, and at the same time reduce the financial pressure on local governments, enterprises and other stock debt.

Of course, we also note that "interest rate policy" is the best way to combat the Fisher effect of rising inflation expectations. The risk judged above is that domestic inflation (expectations) will rise rapidly, causing the currency policy anchor to shift to giving priority to curbing "inflation".