Source: the finishing touch of Zhongjin

Author: Liu Gang, Chen Nanding, Kou Yue, etc.

Since the Fed began its rate-raising cycle in March 2022, the HKMA has followed suit by raising benchmark interest rates (Base rate), triggering a series of chain reactions:

1) the HKMA intervened continuously after the Hong Kong dollar triggered the 7.85 weak party convertibility undertaking in May.

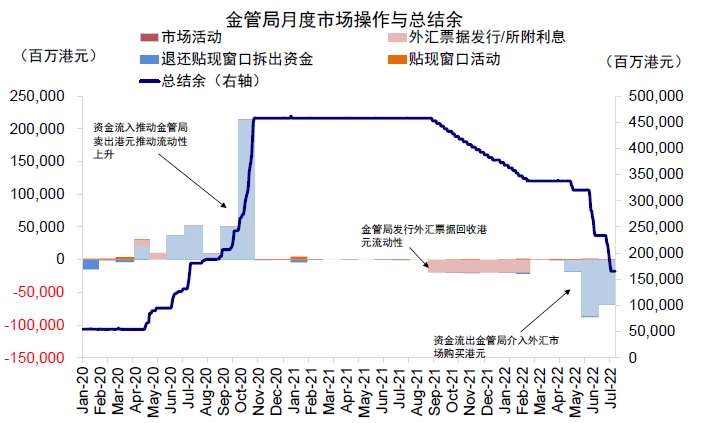

2) the aggregate balance of the HKMA banking system decreased from nearly HK $360 billion at the beginning of 2022 to less than HK $125 billion.

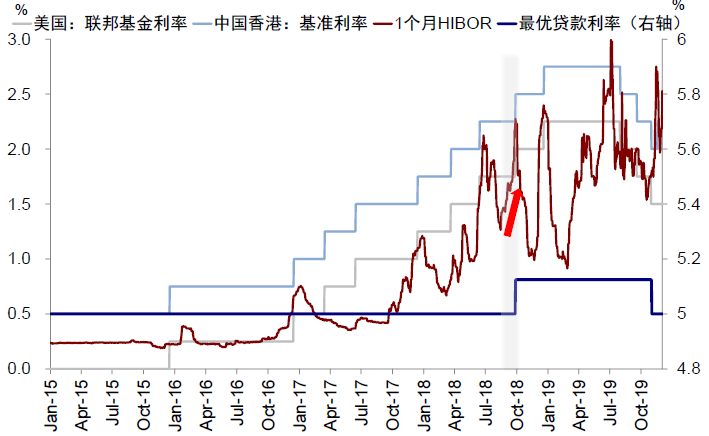

3) the Hibor has increased from 0.25% to 1.85% in one month.

However, these can basically be seen as a "fixed operation" after the Fed raises interest rates, rather than the Hong Kong dollar linked exchange rate system or the financial system that the market is worried about.

Next, we expect Hong Kong to also raise the optimal lending rate (Prime rate or Best lending rate, the lending rate for the best businesses or residents), last raised in September 2018. So what is the composition of Hong Kong's interest rate system? What is the relationship between the optimal lending rate and other interest rates? How does the Fed's interest rate hike affect Hong Kong policy? What is the impact on markets and assets?

Abstract

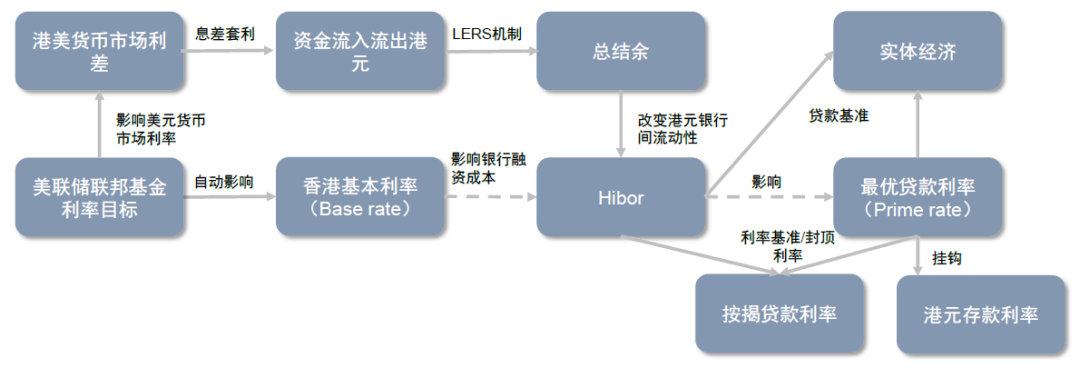

Hong Kong dollar interest rate system and interest rate raising mechanism: benchmark interest rate (Base rate), Hibor and optimal lending rate (Best lending rate)

The linked exchange rate system in which the Hong Kong dollar is pegged to the US dollar makes the policy formation mechanism of Hong Kong different from that of other regions. There are three main interest rate systems:

1) benchmark interest rate (Base rate):The overnight Hong Kong dollar liquidity discount rate provided by the HKMA discount window. Under the linked exchange rate system, the HKMA has given up the independence of monetary policy, so the benchmark interest rate follows the Federal Reserve and is generally higher than the lower 50bp of the federal funds rate.

2) Hibor:The average interest rate quoted by 20 major banks in Hong Kong every day reflects the liquidity of the interbank market. Hibor is the benchmark for major commercial loans in Hong Kong, including housing mortgage loans. In addition, Hibor is also one of the main tools for the HKMA to maintain exchange rate stability under the linked exchange rate mechanism.

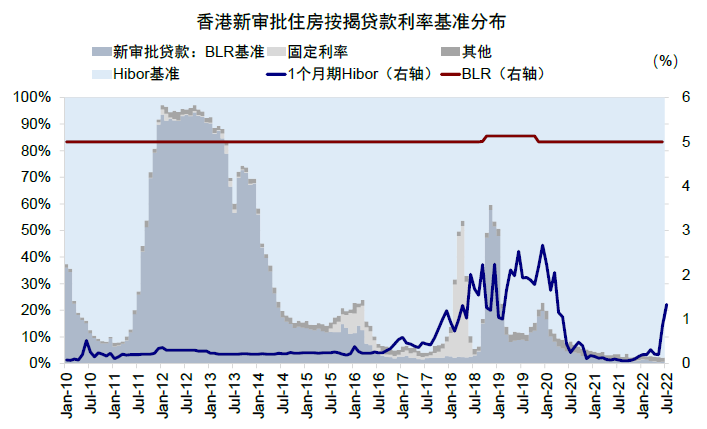

3) the optimal lending rate (Best lending rate or Prime rate):The lending rate that Hong Kong bank adjusts independently, the quotation announced by HSBC at the end of each month is often the main reference index of the market (currently 5%). Although it is called the lending rate, continued loose liquidity after the financial crisis has dominated Hibor-based loans with lower interest rates (98 per cent of new mortgage loans issued in June 2022, while mortgages based on the optimal lending rate account for less than 2 per cent), but since the optimal lending rate is still the capping rate of Hibor-based mortgages, the impact cannot be ignored. In contrast, the optimal lending rate is more closely related to the deposit rate of banks, so its increase will also affect the financing costs of banks.

How does the Federal Reserve affect interest rate hikes and interest rates in Hong Kong? Benchmark interest rate pegged, Hibor following, optimal lending rate lagging behind

1) benchmark interest rateIt is directly linked to the Fed's federal funds rate and is determined by the HKMA, so the response is the fastest and there is little lag.

2) HiborThe changes are related to the design of the linked exchange rate system, which may not be completely synchronized but basically follow. After the Hong Kong dollar triggered the weak-side convertibility undertaking, the HKMA intervened to tighten the interbank aggregate balance, pushing up Hibor to support the Hong Kong dollar.

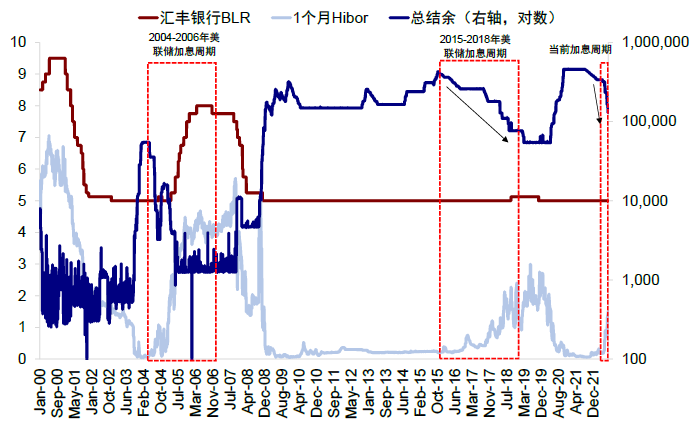

3) the optimal loan interest rateIt is decided by the banks spontaneously, most lagging behind and not necessarily following completely. Hong Kong banks will not adjust until the Hibor rises to a certain extent. In the 2015-2018 interest rate hike cycle, Hong Kong banks did not raise the optimal lending rate until September 2018, nearly three years later than the benchmark rate.

When will Hong Kong raise the optimal lending rate? The aggregate balance decreased significantly and Hibor rose rapidly.

Hong Kong banks usually raise the optimal lending rate when the liquidity pressure of the Hong Kong dollar is high.For example, the aggregate balance decreased significantly (such as less than HK $150 billion) and Hibor rose rapidly. Referring to the experience of the Fed's rate-raising cycle in 2015-2018, the aggregate balance of Hong Kong banks fell to less than HK $100 billion in August 2018, and the one-month Hibor rate rose from 0.2% to 2%. As a result, HSBC raised its BLR 12.5bp to 5.125% at the end of September 2018.

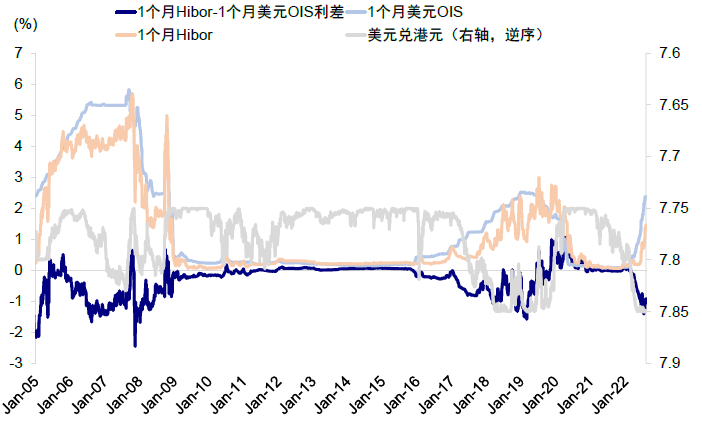

Compared with the current, since the Fed raised interest rates in March 2022, the aggregate balance of the banking system has fallen from nearly HK $360 billion in early 2022 to less than HK $125 billion, and one-month Hibor has risen from 0.25 per cent to around 1.85 per cent, which is not as nervous as it was in 2018. However, as the Fed has raised interest rates more aggressively this time, the economies of Hong Kong, China and Chinese mainland have slowed, the aggregate balance has fallen and capital outflows have been faster (Hibor- dollar OIS is still significantly upside down)Therefore, it does not rule out the possibility that Hong Kong banks will raise interest rates earlier to cope with potential pressure.

The impact of raising the optimal lending rate: or marginal increase in bank costs, push up mortgage rates, but the incremental impact on the overall market financial conditions is limited.

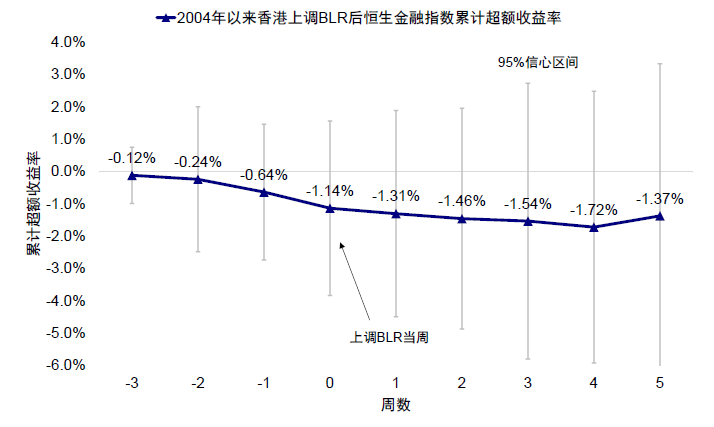

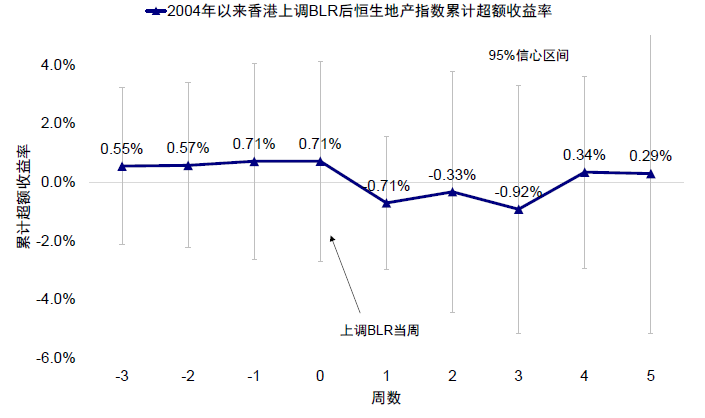

Based on the above analysis, we believe that an increase in the optimal lending rate in the future may marginally increase bank costs and push up the real estate mortgage interest rate, but because the increase in the optimal lending rate lags behind the already higher capital interest rate, therefore, the incremental impact on the overall financial conditions of Hong Kong stocks is limited. So as a result,The increase in interest rates may be negative to the profits of Hong Kong banks and increase the pressure on Hong Kong's real estate market and house prices (Hong Kong property prices fell by 8.4% in the last round of interest rate hikes), but it has a limited impact on the marginal increment of liquidity in Hong Kong stocks as a whole.Based on the CAPM model, we retroactively measure the changes of excess returns of Hong Kong stocks and sectors before and after 9 increases in optimal lending rates since 2004, and get similar results, that is, Hong Kong stocks do not change significantly before and after interest rate increases; the financial sector begins to weaken before interest rates are raised, and the real estate sector is the same, but it is repaired gradually after interest rate increases.

Learning from History: a Review of Hong Kong's interest rate hikes in 2005 and 2018

After reviewing the historical experience of Hong Kong's two rounds of raising optimal lending rates in 2005 and 2018, we find that, in addition to the same tightening pressure on banks and real estate sectors, the overall market and capital flows are very different (market performance was stronger in 2005 and capital inflows were much stronger. The weak performance of Hong Kong stocks and capital outflows in 2018 is more related to the differences in the fundamental environment of China's growth, which is also the key to determining the medium-term trend of the market, especially Chinese stocks; in addition, the Hong Kong dollar is expected to get some support after raising interest rates.

Text

Hong Kong's interest rate system and interest rate hike mechanism

Since the Federal Reserve began its current rate-raising cycle in March 2022, the Hong Kong Monetary Authority (HKMA) has simultaneously raised its benchmark interest rate (Base rate). Against this background, Hong Kong's financial conditions have significantly tightened and triggered a series of chain reactions:

1) after the Hong Kong dollar triggered the weak-side convertibility undertaking in May, the HKMA continuously intervened in the foreign exchange market and bought more than HK $200 billion from banks to defend the exchange rate of the Hong Kong dollar.

2) the aggregate balance of the HKMA banking system has decreased from nearly HK $360 billion at the beginning of 2022 to less than HK $125 billion at the latest (figure 4)

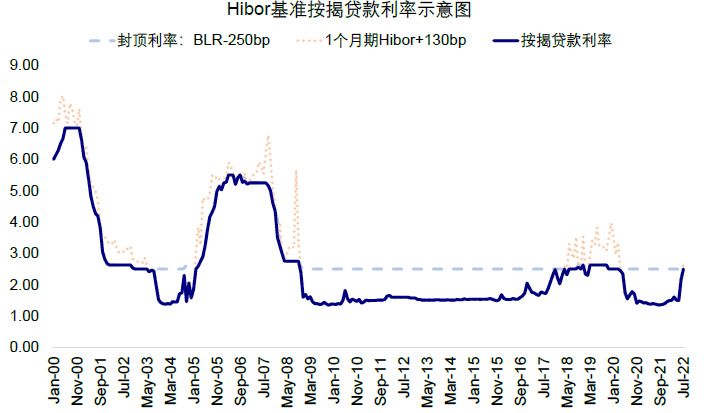

3) the one-month Hibor has increased from 0.25% at the end of March to the current 1.85% (figure 3).

However, the above changes can basically be regarded as a "fixed operation" under the currency board system, not the Hong Kong dollar linked exchange rate system or the financial system that the market is worried about. In addition, if Hong Kong banks raise the optimal lending rate (Prime rate, or Best lending rate,BLR, the lending rate directly aimed at the best commercial or residential customers) in the future, it may have an impact on physical demand and assets. The last time the best lending rate was raised was in September 2018 (chart 3). In this paper, we will explore the interest rate hike mechanism in Hong Kong, the relationship between BLR and other interest rates and its impact on asset prices.

Hong Kong dollar interest rate system: benchmark interest rate, Hibor and optimal lending rate

Hong Kong's status as an international financial center, especially the linked exchange rate system pegged to the US dollar, makes its policy formation mechanism and interest rate system different. There are three main types of interest rates in Hong Kong:

►Benchmark interest rate (Base rate): the HKMA discount window discount rate, which closely follows the US federal funds rate.Base rate is the discount rate for overnight Hong Kong dollar liquidity provided by the HKMA discount window, which is usually the higher of the following: 1) the lower limit of the Federal Reserve funds rate + 50bp and 2) the average of the 5-day moving average of overnight and one-month Hibor (Hong Kong Interbank offered rate). The main auxiliary Hibor setting of Base rate allows banks to obtain liquidity when necessary, while stabilizing and restraining excessive volatility of Hibor.

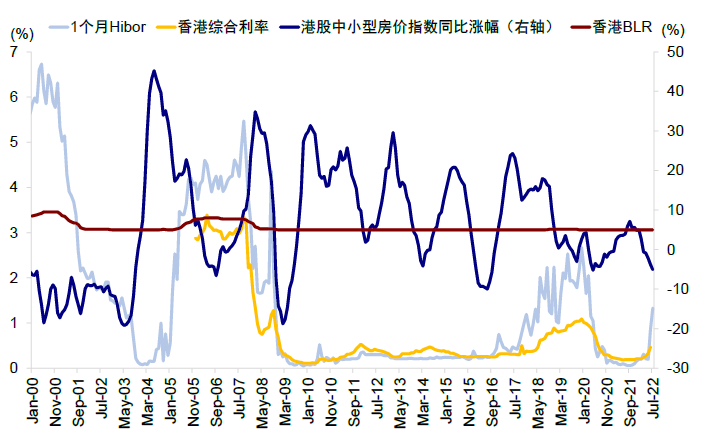

►Hibor (Hong Kong Bank offered rate): reflects the liquidity conditions of the interbank market.Similar to Libor, Hibor is the average interest rate obtained by combining the overnight lending rates of 20 large banks in Hong Kong every day, and is an important indicator of financing costs in the Hong Kong interbank market. Among them, 1-month and 3-month Hibor are important benchmarks for major commercial loans in Hong Kong. According to the HKMA, the Hibor-based assets of Hong Kong's banking system were about HK $3.4 trillion at the end of 2018, accounting for 36 per cent of Hong Kong dollar assets of HK $9.8 trillion at that time. Hibor is also the main interest rate benchmark for housing mortgage loans in Hong Kong, accounting for nearly 98 per cent of new mortgage loans issued in June 2022 (chart 6). In addition, Hibor is one of the main tools to maintain the exchange rate stability of the Hong Kong dollar under the linked exchange rate mechanism. When Hong Kong's capital outflow pressure rises and the Hong Kong dollar triggers a weak side guarantee, the HKMA will automatically purchase Hong Kong dollars from the banking system to tighten Hong Kong dollar liquidity (a decrease in the aggregate balance), which will push up Hibor to reduce Hong Kong-US interest rate spreads, thereby stabilizing capital outflows and exchange rates.

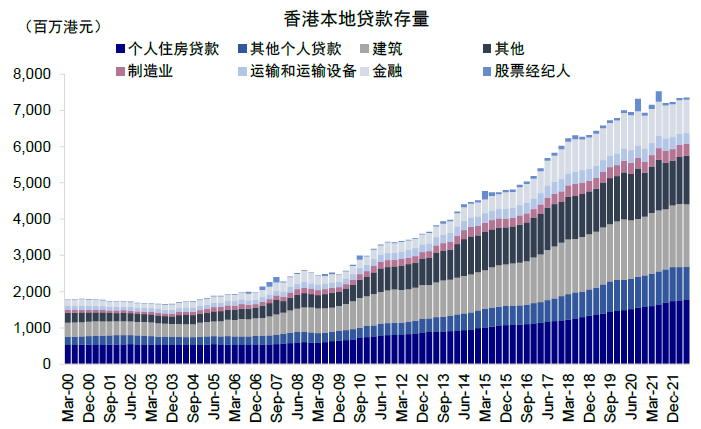

►Optimal lending rate (Best lending rate,BLR or Prime rate): the lending benchmark adjusted by the bank itself, linked to the deposit rate and may reflect more of the bank's cost side (the deposit rate is usually around BLR-500bp).BLR is the best lending rate for Hong Kong banks, and each major bank has its own BLR, but the BLR quoted by HSBC at the end of each month is often the main reference indicator of the market (currently 5 per cent). However, while BLR is literally linked to assets, the proportion of loans linked to direct BLR in Hong Kong bank assets may not be high. On the contrary, BLR is more closely linked to deposit rates (deposits account for 71 per cent of Hong Kong dollar liabilities of banks in Hong Kong), so their changes are likely to have a greater impact on banks' funding costs (chart 2). This is particularly true in a liquidity environment that continues to be abundant in the wake of the financial crisis. In other words, Hong Kong banks currently rely mainly on cheaper deposits, while interest-bearing assets are mostly linked to Hibor (figure 5).

In spite of this, BLR is still the capping rate of home mortgage loans based on Hibor.The long-term low interest rate environment since the financial crisis has made home buyers more willing to choose a lower Hibor as the benchmark for mortgage loans (currently BLR accounts for less than 2% of newly approved mortgage loans in June 2022), but changes in BLR will still affect the mortgage interest rate ceiling because mortgage loans usually still set the BLR ceiling (chart 10).

Chart 1: transmission mechanism of interest rates and liquidity in Hong Kong

Source: Haver, China International Capital Corporation Research Department

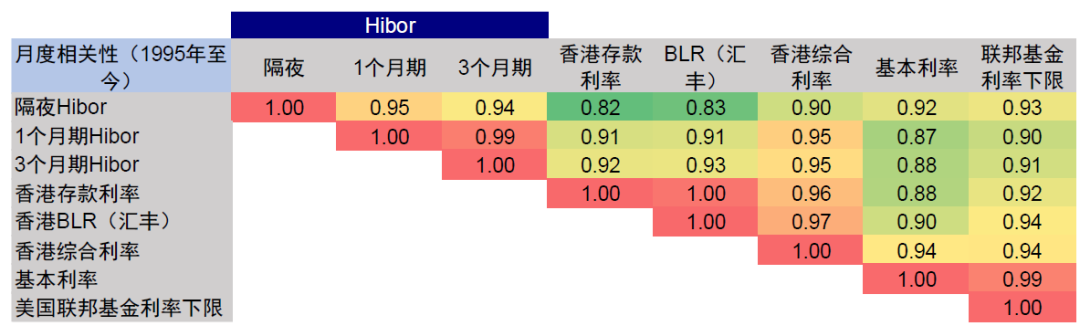

Chart 2: Hong Kong BLR and deposit interest rates are synchronized and highly correlated with Hong Kong composite interest rates

Source: Haver, China International Capital Corporation Research Department

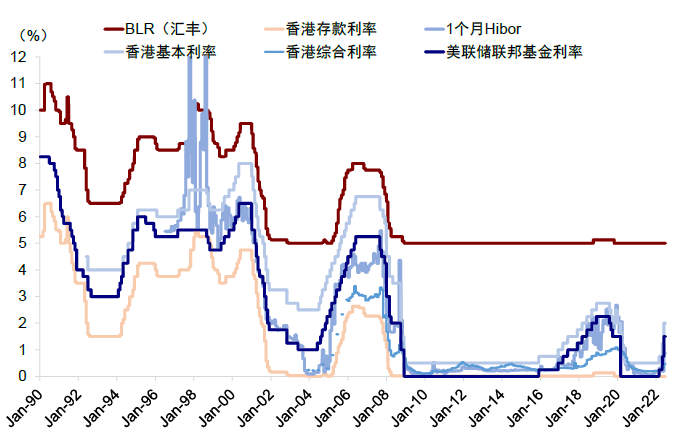

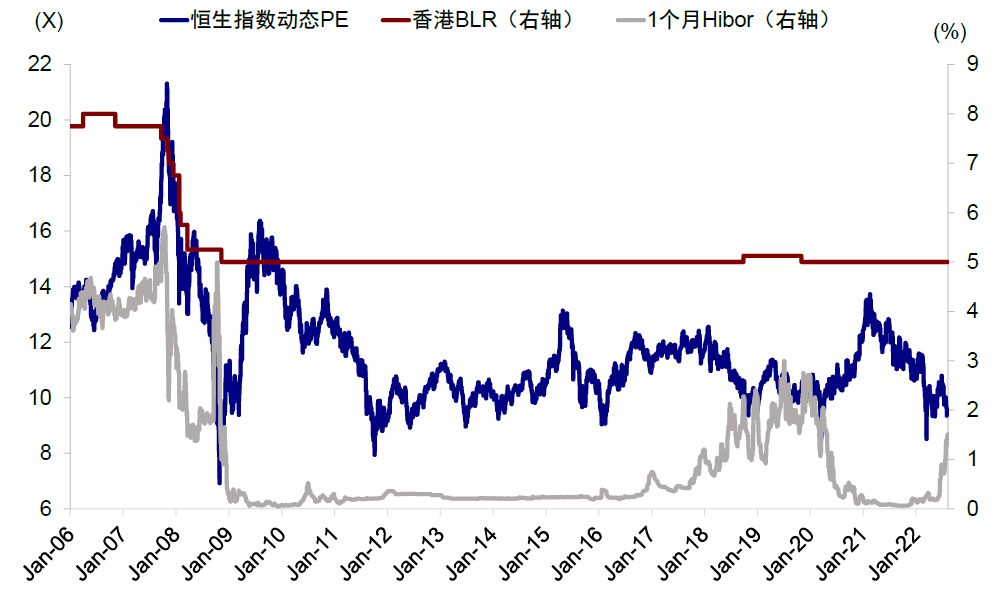

Figure 3: in the Fed's interest rate hike cycle, base rate takes the lead in rising, Hibor follows, and BLR lags behind.

Source: Haver, China International Capital Corporation Research Department

Chart 4: under the pressure of capital outflow, the HKMA has recently intervened many times in the foreign exchange market to defend Hong Kong dollar interest rates, which has also contributed to the decline in the aggregate balance.

Source: HKMA, China International Capital Corporation Research Department

Figure 5: in a low interest rate environment, the current BLR reflects the bank financing cost (deposit interest rate) rather than the loan yield.

Source: Haver, China International Capital Corporation Research Department

Chart 6: currently nearly 98% of home loans use the Hibor benchmark

Source: Haver, China International Capital Corporation Research Department

How does the Federal Reserve affect interest rate hikes in Hong Kong? Benchmark interest rate pegged, Hibor following, optimal lending rate lagging behind

Under the linked exchange rate system, the HKMA will follow the Fed in raising interest rates in the order that the HKMA is pegged to the Fed to raise base rate,Hibor and follow higher, while banks' spontaneous BLR often reacts in the end and has a long time lag.Specifically,

1)Base rate is directly linked to the Fed's federal funds rate and is determined by the HKMA, so it is the first to react and there is little lag.

2) The changes in Hibor are related to the design of the linked exchange rate system, which is not necessarily completely synchronized but basically follows. The upside-down of Hong Kong-US interest rates (such as Hibor- US dollar OIS) will lead to arbitrage capital outflows and the weakening of the Hong Kong dollar, and when the Hong Kong dollar triggers the weak-side convertibility undertaking, the HKMA intervenes to tighten the interbank aggregate balance, which in turn pushes up the interbank financing cost Hibor, thus supporting the exchange rate of the Hong Kong dollar.

3) BLR is decided spontaneously by banks, so it is the most lagging behind and does not necessarily follow completely. Hong Kong banks will adjust their Hibor only after the BLR rises to a certain extent. On the one hand, BLR directly affects the cost side of banks, so banks will only take the initiative to raise interest rates to attract deposits when Hong Kong dollar liquidity tightens to a certain extent. On the other hand, BLR is linked to the capped interest rate of mortgage loans, and mortgage lending is an important business of Hong Kong banks (accounting for 24% of banks' local loans, chart 9) and fierce competition, so banks are often reluctant to raise the interest payment cost of mortgage loans to reduce their competitiveness. In the US interest rate hike cycle of 2015-2018, Hong Kong banks did not raise BLR until September 2018, nearly three years later than base rate.

When will Hong Kong raise the optimal lending rate? The aggregate balance decreased significantly and Hibor rose rapidly.

Hong Kong banks usually raise BLR and deposit rates when the liquidity of the Hong Kong dollar is under pressure and need to attract deposits.As analyzed above, when liquidity is abundant, banks do not need to raise deposit interest rates to attract deposits. On the contrary, when external financial conditions tighten and capital outflows cause Hong Kong dollar liquidity to shrink to a certain extent, banks are willing to raise BLR and deposit rates to attract more Hong Kong dollar deposits.

The main indicators to describe the liquidity of the Hong Kong dollar are:

1) the aggregate balance of the banking system in HKMA liabilities

2) Hong Kong interbank offered rate Hibor.

Historically, banks have usually raised BLR during the period of significant decline in aggregate balance and rapid rise in Hibor.Referring to the experience of the Fed's rate-raising cycle of 2015-2018, the Fed began to raise interest rates at the end of 2015. The aggregate inter-bank balance in Hong Kong continued to decline from HK $410 billion at the end of 2015 and fell to less than HK $100 billion in August 2018. The one-month Hibor rate rose from 0.2 per cent to 2 per cent. Against this backdrop, HSBC raised its BLR 12.5bp to 5.125% on September 27th, 2018. The next day, Standard Chartered Bank and Bank of China Ltd. raised their BLR 12.5bp to 5.375% and 5.125%, respectively.

In contrast to the current rate-raising cycle, since the Fed raised interest rates in March 2022, the aggregate balance of the HKMA's banking system has fallen from nearly HK $360 billion in early 2022 to less than HK $125 billion. At the same time, the weak-side convertibility undertaking triggered by the Hong Kong dollar in May also prompted the HKMA to continuously intervene to defend the exchange rate of the Hong Kong dollar. One-month Hibor rose from 0.25% at the end of March to around 1.85% today.It can be seen that neither the aggregate balance nor Hibor interest rates are as tight as they were when BLR was raised in 2018.However, as the Fed has raised interest rates more aggressively this time, the economic growth of Hong Kong, China and Chinese mainland has slowed, and the rate of capital outflows and the aggregate balance have fallen faster.Therefore, it does not rule out the possibility that Hong Kong banks will raise BLR earlier to cope with potential pressure.

Looking ahead, the Fed will continue to raise interest rates or increase the pressure on Hong Kong banks to raise BLR.Although expectations of the Fed's interest rate cut have risen recently as a result of recession and falling inflation expectations, the 3.5 per cent "end point" and inflation that has not yet fallen sharply suggest that the Fed still has at least the task of raising interest rates by 100bp (CME interest rate futures implicitly expect to raise interest rates by 50bp in September and 25bp in December, respectively), which means that Hong Kong's financial conditions may continue to tighten.Considering that the current short-end Hibor- US dollar OIS spreads are still significantly upside down (figure 8), which may increase the pressure on capital outflows and depreciation of the Hong Kong dollar, banks may raise BLR at some point in the future.

Figure 7: compared with the previous interest rate hike cycle, the Hong Kong dollar liquidity environment tightened more rapidly in the second interest rate hike cycle.

Source: Bloomberg, China International Capital Corporation Research Department

Chart 8: the current short-end Hong Kong-US interest rate spread is obviously upside down, which means that the pressure on capital outflow may still be large.

Source: Haver, China International Capital Corporation Research Department; Note: reference bank mortgage loan

Figure 9: personal housing loans account for about 24% of local loans in Hong Kong

Source: Haver, China International Capital Corporation Research Department

Figure 10: the current mortgage rate in Hong Kong may have exceeded the capped rate

Source: Haver, China International Capital Corporation Research Department

The impact of interest rate hikes in Hong Kong: marginal increase in bank costs, push up mortgage rates; limited impact on overall financial conditions

Synthesize the above analysis of the interest rate hike mechanism in Hong Kong and the relationship between different interest ratesIf the BLR is raised in the future, it may marginally increase bank costs and push up the real estate mortgage interest rate; but because the increase in the optimal lending rate lags behind the already higher capital interest rate, the incremental impact on the overall financial conditions of Hong Kong stocks is limited.Specifically:

►Banks: or marginal increase in bank costs.BLR is closely related to the cost side (deposit interest rate) of Hong Kong banks, so an increase in BLR may have a marginal impact on banks' net interest margin. Hong Kong's composite interest rate, which measures banks' overall funding costs, is highly correlated with deposit rates and BLR, suggesting that the increase in BLR could mean that the period in which Hong Kong's net interest margin has risen sharply in the interest rate hike cycle is over. Judging from the correlation between BLR-Hibor and bank net interest margin, the current increase in BLR may have a negative impact on the profit margins of Hong Kong banks.

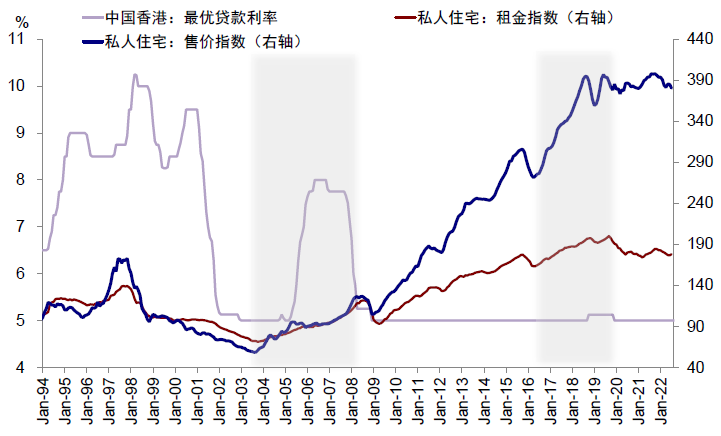

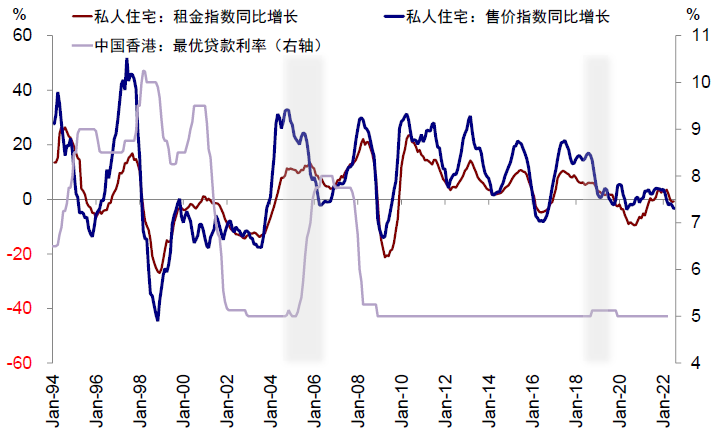

►Real estate: push up the cost of mortgage loans or increase the pressure on the Hong Kong real estate market.Against the backdrop of the upward Hibor, Hong Kong's Central Plains property price index (Centa-city Index) has fallen year-on-year since March 2022, while the small and medium-sized housing price index fell 5.1 per cent in July, the biggest decline since the epidemic. If the BLR is further raised in the future, it may increase the interest payment pressure on housing mortgage loans. Historically, house prices have often come under pressure after Hong Kong banks raised their BLR. Hong Kong property prices fell by about 8.4 per cent in February 2019 after banks raised BLR by 12.5 per cent in September 2018.

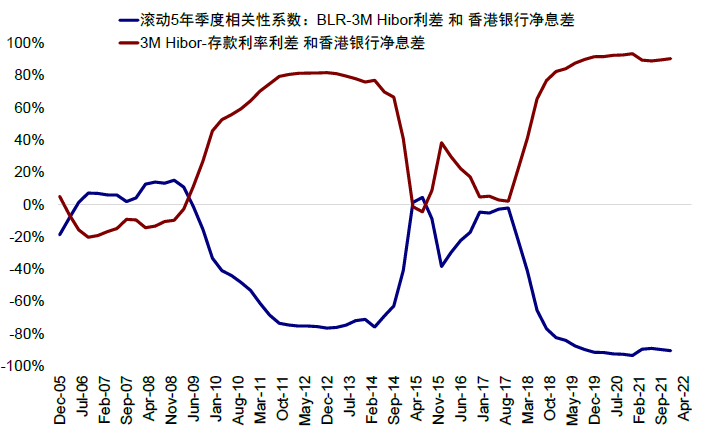

►Hong Kong stock market: the marginal impact on financial conditions is relatively limited.As the BLR adjustment lags behind, the marginal impact of changes in BLR on the financial conditions of Hong Kong stocks is relatively limited when the financial conditions of Hong Kong stocks have been taken into account (figure 15).

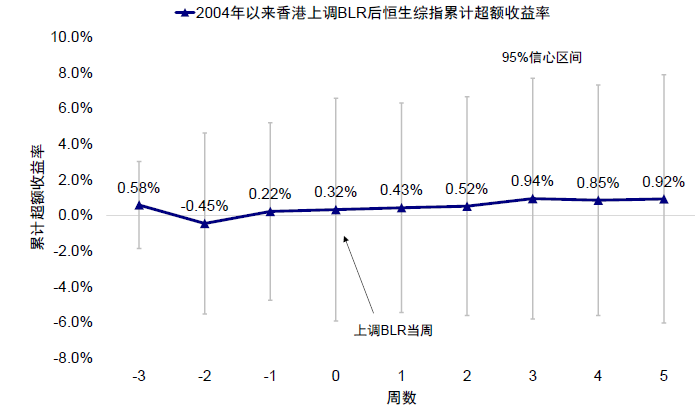

We use backtracking to measure the changes in excess returns in Hong Kong stock markets and sectors before and after the BLR increase to capture the impact of this event. In the specific calculation, based on the CAPM model, we measure the changes of Hong Kong stocks (Hang Seng Composite Index) relative to MSCI global excess returns before and after 9 BLR increases since 2004.

The results show that there is no significant return change in the Hong Kong stock market before and after the increase of BLR.Within five weeks of the BLR increase, the cumulative excess return of Hong Kong stocks was only 0.92% higher than that before the increase, and was significantly lower (figure 12). By contrast, the financial sector (the Hang Seng Financial Index) began to weaken a few weeks before the BLR increase, with cumulative excess returns of-1.72 per cent in the fourth week after the BLR increase (chart 13). The real estate sector (Hang Seng property index) weakened slightly after the BLR increase, but basically recovered its decline in the fourth week after the increase (chart 14).Thus, the upward adjustment of BLR has no significant impact on the overall short-term performance of Hong Kong stocks, but has a greater impact on the financial and real estate sectors, which is basically consistent with the conclusions we have analyzed above.Looking ahead, the future trend of Hong Kong stocks depends more on China's growth and earnings prospects, as well as expected changes in Fed policy.

Chart 11:BLR increases are often accompanied by further declines in house prices

Source: Bloomberg, China International Capital Corporation Research Department

Figure 12: banks' upward adjustment of BLR has no significant impact on Hong Kong stock market.

Source: Bloomberg, China International Capital Corporation Research Department

Chart 13: the financial sector of Hong Kong stocks tends to weaken before and after the BLR increase

Source: Bloomberg, China International Capital Corporation Research Department

Chart 14: the Hong Kong real estate sector weakened in the week when BLR was raised, but recovered within a few weeks

Source: Bloomberg, China International Capital Corporation Research Department

Chart 15:BLR increases significantly lagging behind other capital interest rates, so the marginal impact on the Hong Kong stock market is relatively limited.

Source: Bloomberg, China International Capital Corporation Research Department

Learning from History: the experience of Hong Kong's interest rate hike cycle in 2005 and 2018

The policy and economic background of previous adjustments to the optimal lending rate

First, in the context of the global monetary policy cycle:The optimal lending rate adjustment is in the Fed interest rate raising cycle, and Hibor is the leading indicator. Specifically,

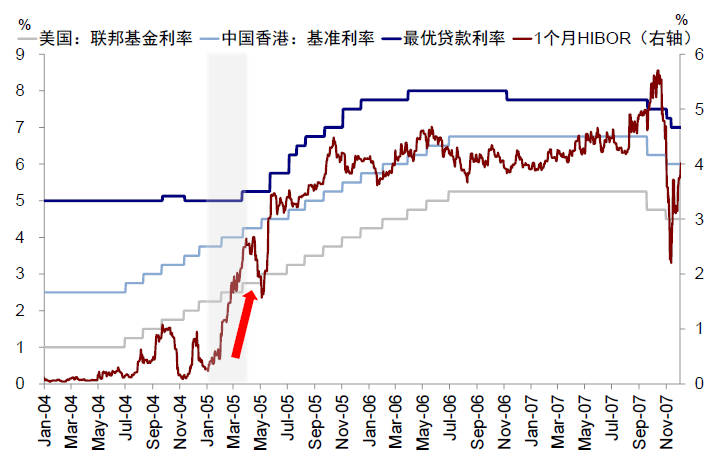

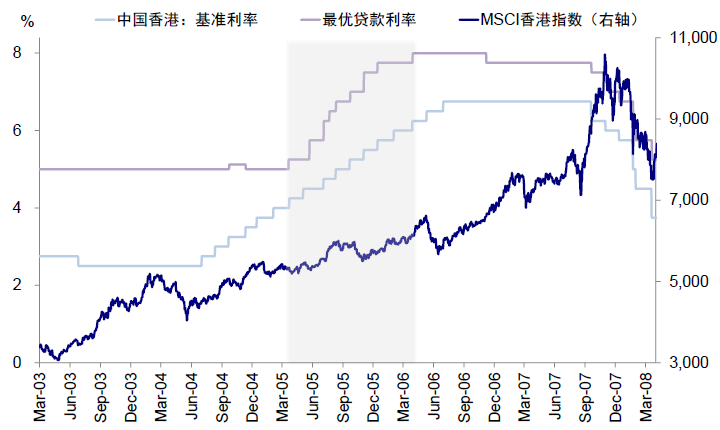

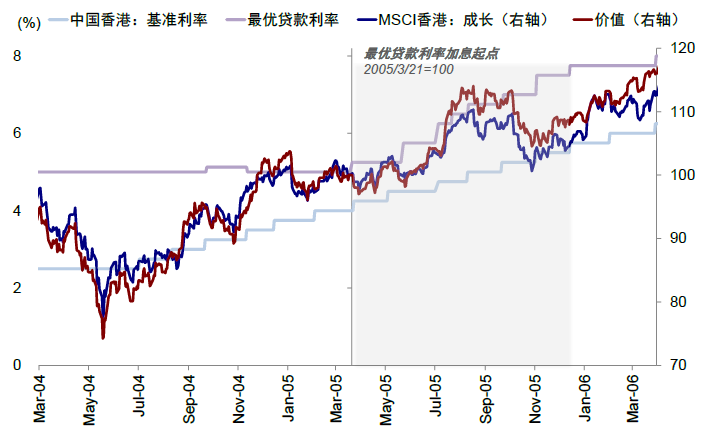

►The 2005 rate hike was in the midst of the Fed's interest rate hike cycle, and the benchmark interest rate was raised nine months after it raised the optimal lending rate.The Federal Reserve raised interest rates 17 times in a row from June 2004 to June 2006. About nine months after the HKMA began the benchmark interest rate hike cycle in June 2004, the Bank of Hong Kong raised the optimal lending rate on March 21, 2005.

Furthermore, from the perspective of the more market-oriented Hibor, before raising the optimal lending rate in 2005, there was a significant rise in Hibor in one month, rising sharply from less than 0.25% to about 2.5% in the first three months of 2005, thus confirming that to a certain extent, Hibor can also be regarded as a leading indicator of raising the optimal lending rate in the future.

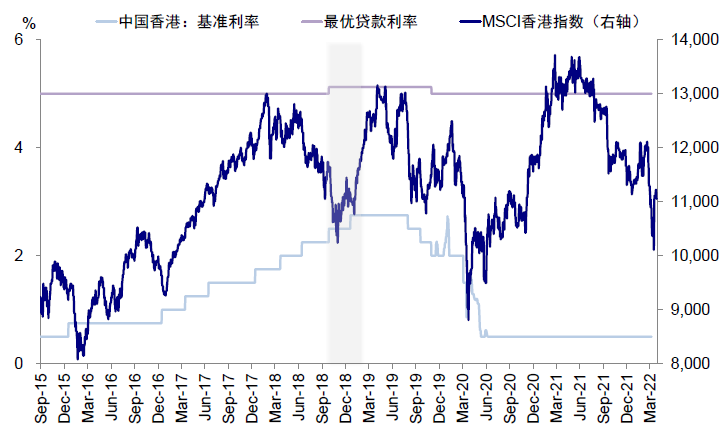

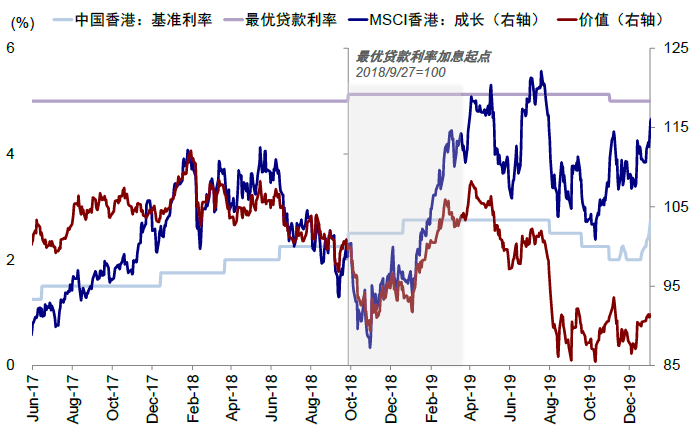

►During the 2015 interest rate hike cycle, the Hong Kong Monetary Authority also followed the pace of the Federal Reserve to adjust the benchmark interest rate, and about three years later, Hong Kong banks raised the optimal lending rate.On December 17, 2015, the Fed officially began a slow cycle of raising interest rates to 0.25-0.5%, raising benchmark interest rates nine times to 2.5% by December 2018. Following the pace of interest rate hikes by the Federal Reserve, the HKMA raised the base rate of the discount window nine times in December 2015. Until September 27, 2018, after the Federal Reserve and the Hong Kong Monetary Authority raised the base rate for the eighth time (the third time this year), HSBC took the lead in raising the optimal lending rate, effective September 28. Then Hang Seng Bank, Standard Chartered Bank and BOC Hong Kong (Holdings) Limited also raised their 12.5bp to 5.125%, the first increase since 2006.

In terms of Hibor, one-month Hibor rates fell for most of 2017 until September, when they began to climb rapidly, rising from a low of less than 0.5 per cent to about 1.2 per cent today, breaking 1 per cent for the first time since the end of 2008.

Second, from the macro background, the economy is usually in the post-cycle, with growth peaking and inflation rising.

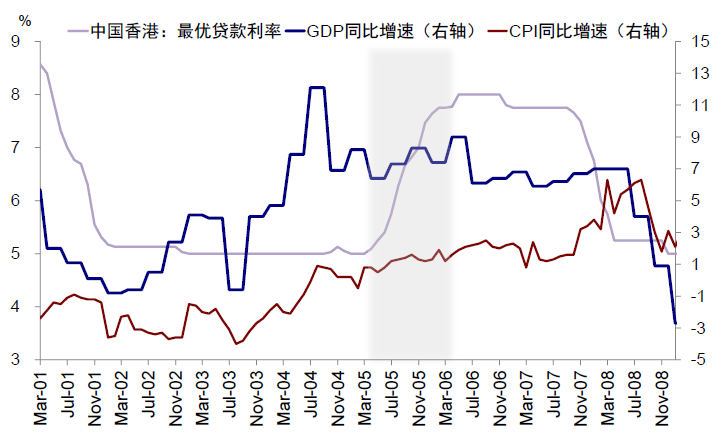

►From a macro perspective, the cycle of raising interest rates at the optimal lending rate in 2005 coincides with the rapid growth of Hong Kong's economy.(during the one-year interest rate hike cycle from March 2005 to March 2006, the year-on-year growth rate of Hong Kong's GDP rose from 6.4% to 9%) andAn environment in which inflation is moderate and upward(when interest rates were raised in March 2005, CPI was 0.8% year-on-year, but continued to rise throughout the interest rate hike cycle, with an average of 1.24%.

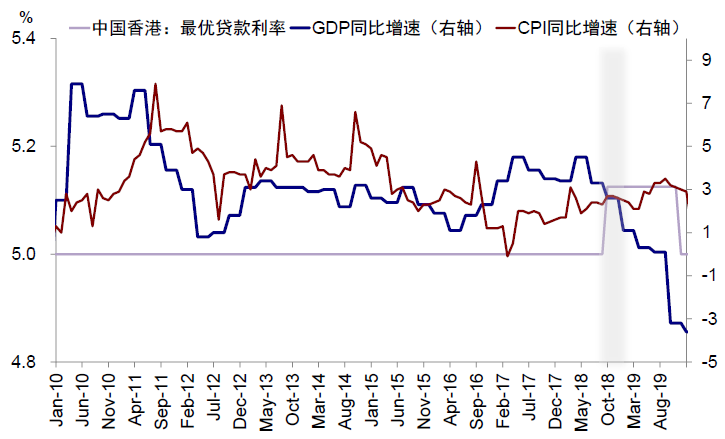

► 's GDP growth rate in the first three quarters of 2018 was 4.5 per cent, 3.3 per cent and 2.6 per cent respectively, and overall began to peak and decline. CPI rose from 1.7 per cent year-on-year at the beginning of 2018 to 2.7 per cent in September, with inflation picking up moderately.

In contrast, the economy has been repeatedly affected by the epidemic more weakly than before, and inflation remains moderate.The overall economy of Hong Kong recovered significantly in 2021, but the pace of growth in the second half of 2021 was slower than that in the first half of the year. Hong Kong's exports have benefited from the global economic recovery, the high growth of private consumption expenditure, the improvement of the local labour market and the consumption voucher scheme, which have jointly contributed to the moderate growth of Hong Kong's GDP. GDP grew 5.1 per cent year-on-year in the second half of 2021, compared with 7.8 per cent in the first half. For the whole of 2021, the economy grew 6.4% year-on-year, achieving positive growth for the first time since 2019. However, the fifth wave of the outbreak in the first quarter of 2022, superimposed by the Federal Reserve's monetary tightening, the conflict between Russia and Ukraine and many other uncertain factors, added another cloud to Hong Kong's local economic activity. Inflationary pressures in Hong Kong have increased since the second half of 2021, but remain moderate. Looking ahead, the Hong Kong government forecasts that the headline inflation rate will be 2.1% in 2022.[1]。

Third, from the point of view of the Hong Kong real estate market, which is more related to the optimal lending rate, housing prices are usually in the upward channel.

Before ► raised prime lending rates in March 2005, house prices in Hong Kong had risen for 20 months from the bottom in July 2003, rising 62 per cent, while the rent index rose 15 per cent over the same period.

During the ► interest rate hike cycle in 2015, if you calculate the upward cycle of Hong Kong house prices from the bottom at the end of 2008 to September 2018 for nearly 10 years, the cumulative increase is 257%, and the rent index is also up 112%.

Unlike the previous two interest rate hikes, house prices and trading volumes in Hong Kong have softened since mid-2021 due to the spread of the local epidemic and the tightening of local social distance measures. The private housing price index fell 0.3 per cent year-on-year in February 2022, falling into the range of negative growth for the first time since December 2020, with a 3.4 per cent year-on-year decline in June.

Figure 16: from the Hibor point of view, before the optimal lending rate was raised in 2005, there was a significant rise in Hibor in one month.

Source: Bloomberg, China International Capital Corporation Research Department

Chart 17: also during the 2015 interest rate hike cycle, one-month Hibor began to climb rapidly in September 2018, rising from a minimum of less than 0.5% to about 1.2%.

Source: Bloomberg, China International Capital Corporation Research Department

Chart 18: the cycle of raising the optimal lending rate in 2005 coincides with the rapid growth of the Hong Kong economy, with inflation rising moderately; similar in 2018

Source: Bloomberg,Wind, China International Capital Corporation Research Department

Chart 19: judging from the Hong Kong real estate market, which is more related to the optimal lending rate, house prices continued to rise before the start of the interest rate hike cycle.

Source: Wind, China International Capital Corporation Research Department

Impact on the economy and asset prices

In the two cycles of raising Hong Kong's optimal lending rates from March 2005 to March 2006 and September 2018, we have found some historical experiences in terms of Hong Kong's overall economy, the real estate market, the Hong Kong dollar exchange rate, capital flows, the stock market, and the rotation of different styles and sectors.

1) growth and inflation: the Hong Kong economy remained robust during the 2005 interest rate hike cycle.Although it did not accelerate upward as much as it did before the rate hike, it maintained rapid growth, with GDP growth averaging 7.7 per cent year-on-year throughout the rate hike cycle. At the same time, inflation as a whole remains moderately upward, with CPI averaging about 1.2 per cent year-on-year. This is also basically in line with the general law that the interest rate hike cycle usually corresponds to the overall economic recovery and expansion cycle.

In the 2018 interest rate hike cycle, Hong Kong's economy maintained strong growth in the first half of the year, but slowed significantly in the second half of the year. In 2019, the warming of Sino-US trade frictions and local social events made Hong Kong's economy into recession, and GDP showed negative growth in the third quarter of 1919. Overall inflationary pressures remained broadly moderate, with CPI around 2.8 per cent year-on-year (mainly due to rising pork prices).

2) House prices: the growth rate slows down, and the later period has a stronger correlation with the overall economic situation.As the increase in optimal lending rates had a direct impact on Hong Kong's real estate industry, interest rate increases in 2005 and 2018 had an immediate effect on Hong Kong real estate prices, with year-on-year growth falling sharply throughout the interest rate hike cycle. even fell slightly to negative at one point. House prices only regained their upward momentum after the end of the interest rate hike cycle in March 2006 and did not end until the outbreak of the global financial crisis in 2008. However, after the cut of the optimal lending rate in October 2019, house prices are still relatively weak in the context of poor economic conditions, which is similar to the conclusion made by IMF in a working paper Determinants of Property Prices in Hong Kong SAR: Implications for Policy in November 2011, that is, in the medium to long term, the most fundamental factors that determine housing prices in Hong Kong are real per capita GDP and land supply (but there is a significant time lag). Other factors, such as the level of real interest rates, real construction costs and domestic credit conditions, are relatively weak.[2]。

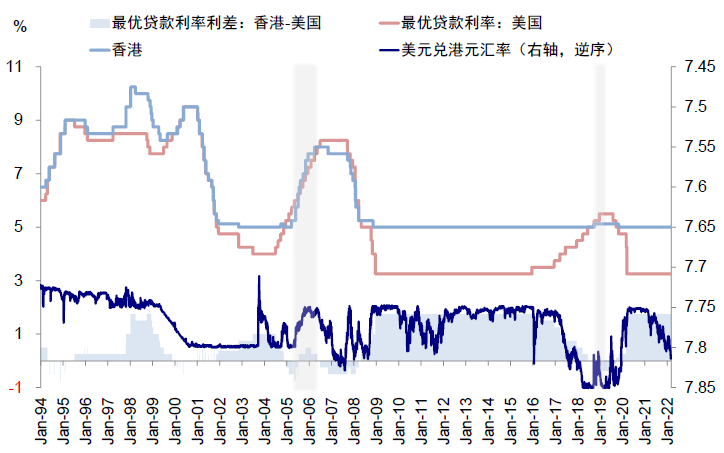

3) Exchange rate: the exchange rate of the Hong Kong dollar is supported to some extent.Based on the experience of the 2005 and 2018 interest rate hike cycles, an increase in the optimal lending rate will widen the spread between Hong Kong and the US again, so the exchange rate of the Hong Kong dollar against the US dollar will also be supported throughout the interest rate hike cycle.

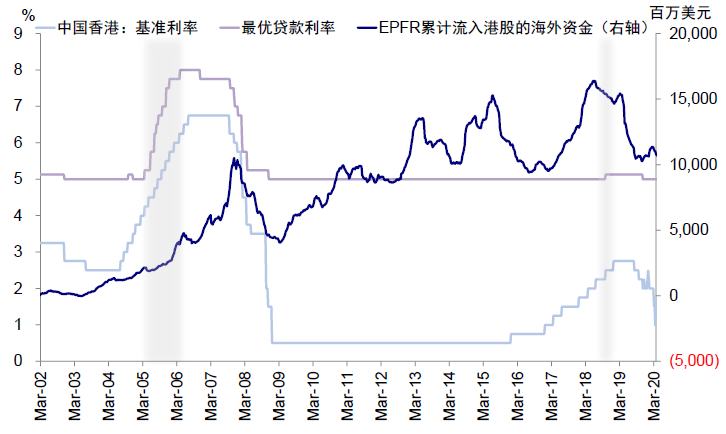

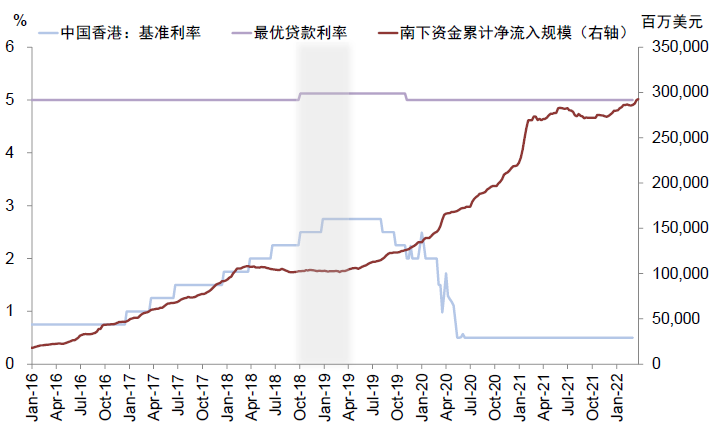

4) Capital flows: foreign capital flows asynchronously in two cycles, and interest rate hikes may not be a decisive factor.During the interest rate hike cycle in 2005, overseas funds continued to flow into Hong Kong stocks under the caliber of EPFR, which lasted until the 2008 financial crisis. On the eve of interest rate hikes in 2018, overseas capital began to flow out in July under the influence of China's economic slowdown and a strong dollar; on the other hand, mainland investors' optimism about Hong Kong stocks pushed southward capital inflows moderately during this period.

Comparing the different pace of overseas funds in the two interest rate raising cycles, we find that interest rate increases are not actually the decisive factor affecting capital flow, but also lie in the economic and profit fundamentals, that is, the relative attractiveness of the return on investment of assets, especially in different markets. As we analyzed above, the interest rate hike cycle in 2005 coincided with the overall improvement of the Hong Kong economy, so it was able to attract sustained capital inflows, while the economic growth in 2018 was under downward pressure, and the decline in profits led to a more cautious sentiment among foreign investors.

Chart 20: during the 2005 interest rate hike cycle, the Hong Kong economy remained robust and inflation rose moderately.

Source: Bloomberg,Wind, China International Capital Corporation Research Department

Chart 21: during the interest rate hike cycle in 2018, against the backdrop of global economic weakness, Hong Kong's economic growth slowed significantly and inflationary pressures remained generally moderate.

Source: Bloomberg,Wind, China International Capital Corporation Research Department

Chart 22: two rounds of optimal lending rate increases in 2005 and 2018 had an immediate effect on Hong Kong real estate prices, with year-on-year growth falling sharply throughout the interest rate hike cycle.

Source: Bloomberg,Wind, China International Capital Corporation Research Department

Chart 23: the increase in the optimal lending rate has widened the spread between Hong Kong and the United States again, so the exchange rate of the Hong Kong dollar against the US dollar has also been supported throughout the interest rate hike cycle.

Source: Bloomberg,Wind, China International Capital Corporation Research Department

Chart 24:EPFR statistics show that overseas capital continued to flow into Hong Kong stocks during the interest rate hike cycle in 2005, while there was a net outflow in the 2018 cycle.

Source: Bloomberg,Wind, China International Capital Corporation Research Department

Chart 25: during the 2018 interest rate hike cycle, mainland investors' optimism about Hong Kong stocks pushed southward capital inflows to maintain a moderate level.

Source: Bloomberg,Wind, China International Capital Corporation Research Department

5) performance of Hong Kong stocks: slightly weaker near the rate hike in 2005, but continued to rise as a whole; shock fell in 2018.Under the background of the overall improvement of economic growth and the rebound of corporate profits, the increase of the optimal lending rate in 2005 did not have much impact on the stock market. Specifically, although the MSCI Hong Kong index was slightly weak in the 1-3 months before and after the first rate hike, it was only basically flat rather than falling sharply; in the second half of the rate-raising cycle (6-12 months), the market regained its upward momentum and continued a strong upward trend.

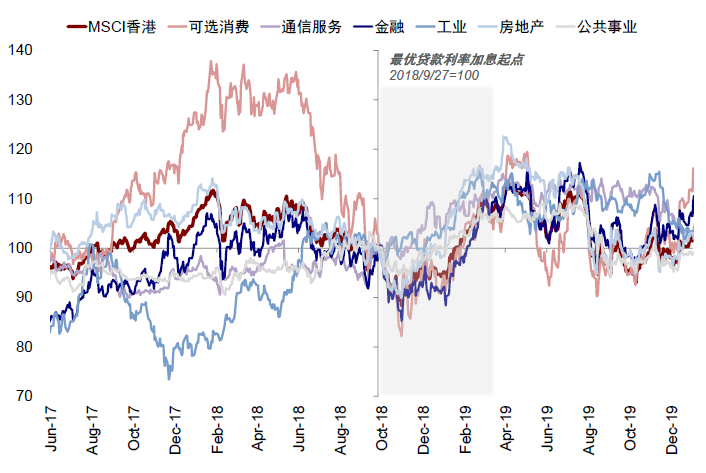

In contrast, the global economic growth slows in the second half of 2018, and there are many uncertainties in internal policies and external environment.Hong Kong stocks fluctuated lower during interest rate hikes in 2018The volatility of Hong Kong stocks has also been further reinforced by the turmoil in peripheral US stocks and emerging markets. Specifically, the MSCI Hong Kong index fell 10.6 per cent one month after the rate hike in September 2018, narrowed its decline (- 5.3 per cent) three months later and rose again six months after the rate hike.

6) driving factors: the initial contraction of valuation is obvious, and profit is the key factor affecting the market trend.The specific impact of the interest rate hike cycle can be better understood by further decomposing the contribution of valuation and earnings to the market. Specifically:

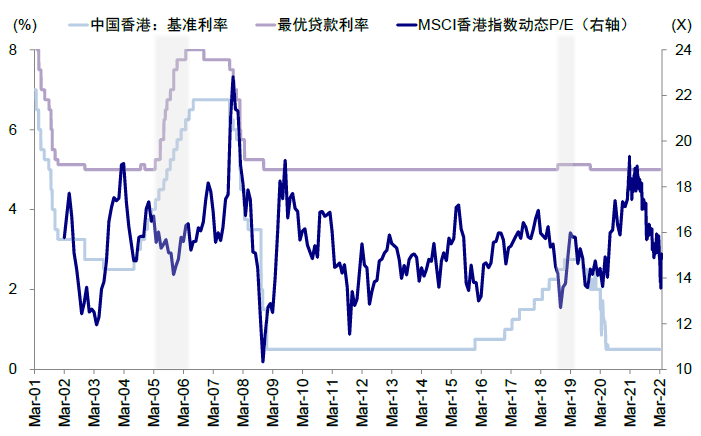

► The rise in interest rates initially suppressed market valuations.Looking at the market as a whole, the decline in valuations began three months before the rise in the optimal lending rate (around December 2004 and May 2018, respectively). In the two interest rate hike cycles, the 12-month dynamic valuation of the MSCI Hong Kong market fell back from the beginning to the bottom (from the end of December 2004 to the end of October 2015 and from the end of May to the end of October 2018) by 18.4% and 21.9%, respectively.

► Profit is the key to whether it plays a supporting role in the market performance under the contraction of valuation.We note that during the interest rate hike cycle in 2005, corporate earnings rose steadily in line with the overall economic fundamentals at that time, offsetting the contractionary impact of higher valuations, so the market was still able to rise. However, with the middle and later stages of interest rate hikes (after October 2005), valuations regained their upward momentum and expanded significantly again, making a positive contribution to the index performance. In the 2018 interest rate hike cycle, dynamic earnings forecasts in Hong Kong dollar terms continued to be lowered due to lower earnings forecasts and exchange rate movements by analysts, and the market was hit by a double blow of valuation contraction and earnings decline. It was only after the valuation was fixed in November 2018 that the MSCI Hong Kong index rebounded periodically.

7) style performance: the value outperforms the growth in 2005, and the growth is more resilient in 2018. In the 2005 cycle of raising Hong Kong's best lending rates, value stocks outperformed growth stocks as a whole, with the MSCI Hong Kong value index and growth index rising 16.2 per cent and 12.8 per cent respectively. AndDuring the 2018 interest rate hike cycle, growth stocks were significantly more resilient than value sectors.Specifically, three months after the rate hike, the MSCI Hong Kong growth index fell 4.3 per cent. The Personality MSCI Hong Kong value index fell 6.3 per cent. Six months later, growth rose 11.1 per cent, while the value rebounded by about 3.1 per cent. And the market capitalization factor performance, the two rounds of interest rate increase cycle, the size of the difference is not big.

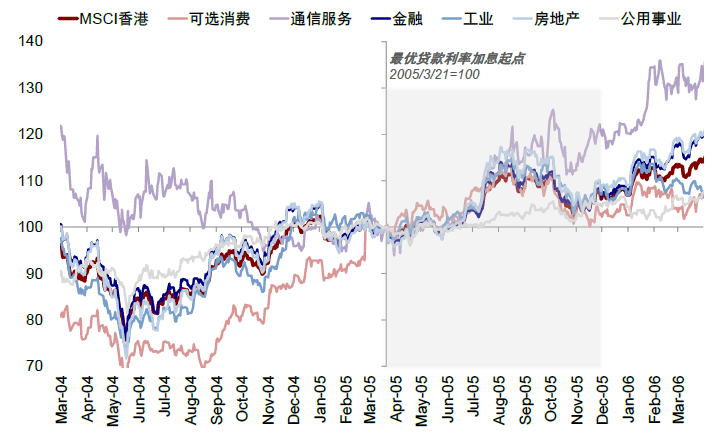

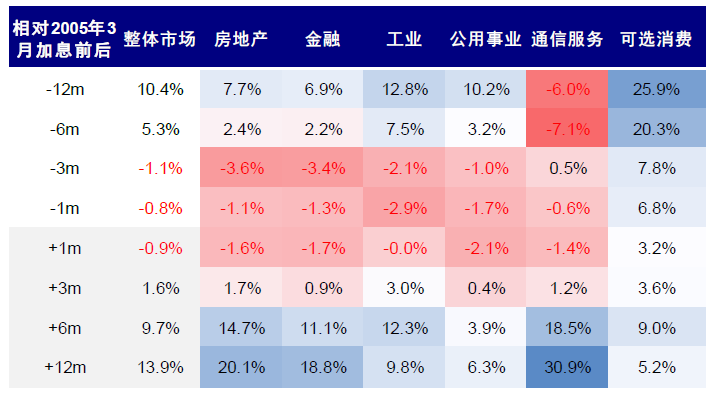

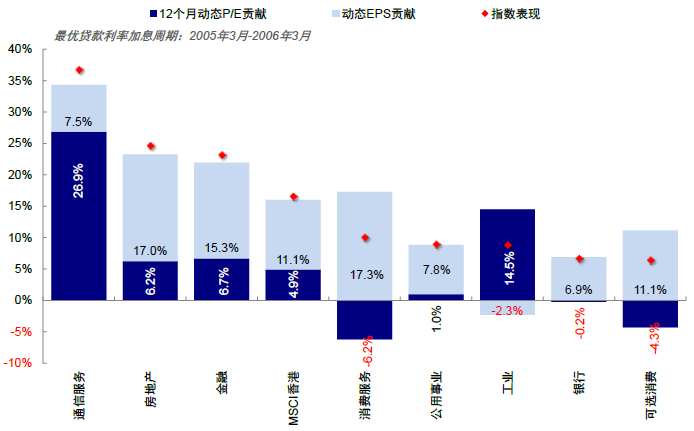

8) the performance of the plate: the financial, real estate and communications services sectors led the rise in the middle and later stages of interest rate hikes.We noticed thatThere are obvious signs of rotation between plates before and after the 2005 interest rate hike cycle.Within 6-12 months before interest rate hikeOptional consumer, industrial, and utilities performed best, but after the interest rate hike cycle began, the leading sectors began to switch to financial, real estate and communications services.However, near the rate hike (within 1-3 months), all sectors were relatively weak under the influence of mood. Further unraveling the contribution of valuation and profitability to its performance at the sector level, we note that the sectors with greater profit contribution are consumer services, real estate, finance, etc.; the larger expansion of valuation is the telecommunications, industrial, real estate and financial sectors.

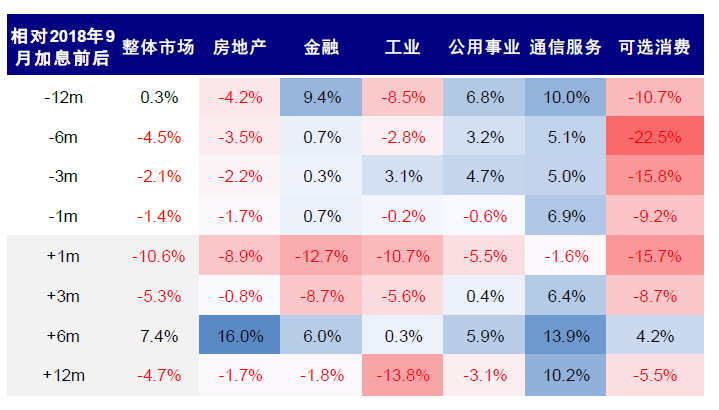

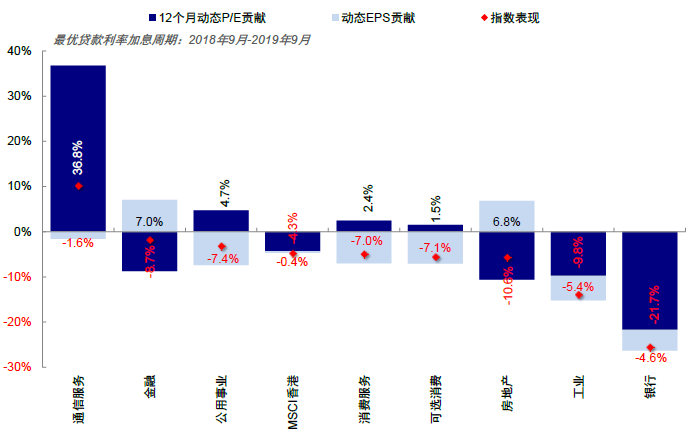

In the 2018 interest rate hike cycleThe communications services, finance and utilities sectors performed better before and after the exchange rate hike. Real estate that performed poorly before the rate hike led the rise in the six-month cycle after the rate hike. Further dismantling, profits make a greater contribution to communications services and public utilities, while the financial and real estate sectors have a larger valuation expansion.

Chart 26: the increase in the optimal lending rate in 2005 did not have much impact on Hong Kong stocks

Source: Bloomberg,Factset,Wind, China International Capital Corporation Research Department

Chart 27: but Hong Kong stocks fluctuated lower during the 2018 interest rate hike and regained their upward momentum only after six months of interest rate hike

Source: Bloomberg,Factset,Wind, China International Capital Corporation Research Department

Figure 28: the rise in interest rates initially suppresses market valuations

Source: Bloomberg,Factset,Wind, China International Capital Corporation Research Department

Chart 29: corporate earnings rose steadily in 2005 in line with the fundamentals of the economy as a whole, offsetting the contraction in valuations due to higher interest rates; but the market was hit by a double whammy of shrinking valuations and falling earnings in 2018

Source: Bloomberg,Factset,Wind, China International Capital Corporation Research Department

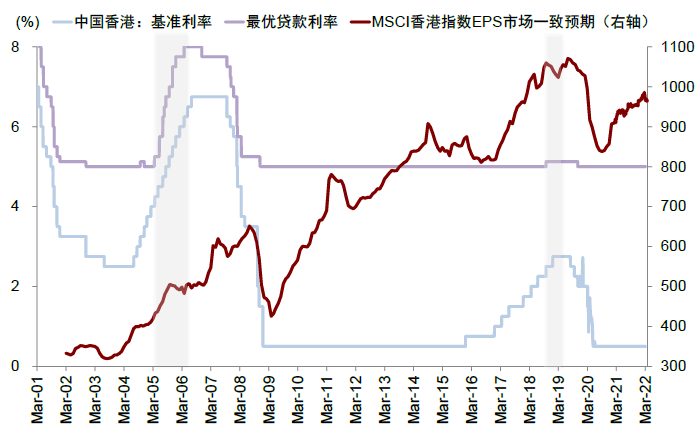

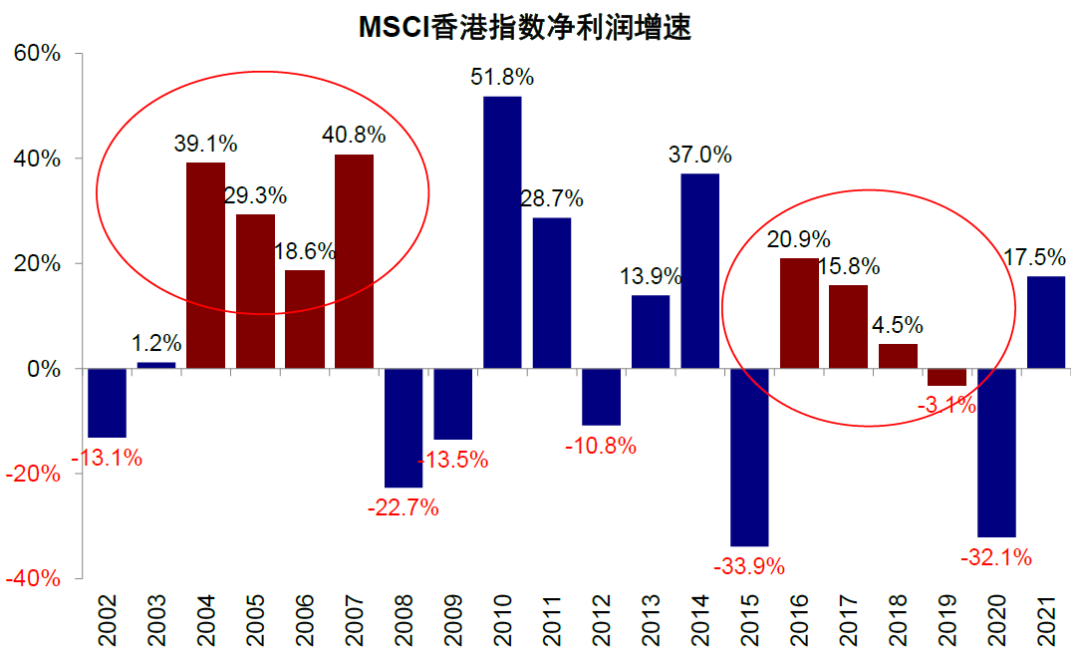

Chart 30 MSCI Hong Kong Index earnings growth during the period 2004-2006 was very strong, which was in line with the trend of economic fundamentals at that time, while profits continued to decline during the period 2016-2019.

Source: Bloomberg,Factset, China International Capital Corporation Research Department

Chart 31: in the interest rate hike cycle of Hong Kong's optimal lending rate in 2005, value stocks performed significantly better than growth stocks as a whole.

Source: Bloomberg,Factset, China International Capital Corporation Research Department

Chart 32: during the 2018 interest rate hike cycle, growth stocks are significantly more resilient than value stocks.

Source: Bloomberg,Factset, China International Capital Corporation Research Department

Figure 33: there are obvious signs of rotation between plates before and after the 2005 interest rate hike cycle

Source: Bloomberg,Factset,Wind, China International Capital Corporation Research Department

Chart 34: there is a similar rotation in the 2018 interest rate hike cycle.

Source: Bloomberg,Factset,Wind, China International Capital Corporation Research Department

Chart 35: after the start of the interest rate hike cycle in 2005, the leading sectors began to switch from optional consumer, industrial, and public utilities to financial, real estate, and communications services.

Source: Bloomberg,Factset,Wind, China International Capital Corporation Research Department

Chart 36: during the 2018 interest rate hike cycle, the communications services, finance and utilities sectors performed better before and after the exchange rate hike; real estate picked up momentum.

Source: Bloomberg,Factset,Wind, China International Capital Corporation Research Department

Chart 37: in the 2015 cycle, the sectors with large profit contributions are consumer services, real estate, finance, etc.

Source: Bloomberg,Factset,Wind, China International Capital Corporation Research Department

Chart 38: among the interest rate hikes in 2018, profits make a greater contribution to communications services and public utilities, while valuations support finance and real estate.

Source: Bloomberg,Factset,Wind, China International Capital Corporation Research Department

Edit / roy