Source: Zhongjin Dianqing

Although the summer high temperature period is passing, we believe that the tension in the global seaborne thermal coal market may continue and there may still be some price upside risks this winter. The core logic of high overseas thermal coal prices still lies in the risk of rising natural gas shortage in Europe and other places, and behind it is the great challenge faced by the European energy supply system under the background of short-term "Russia-Ukraine" shock and long-term green transformation.

There have been one global heat wave after another this summer, and the demand for coal has soared.

There are one heat wave after another in the northern hemisphere this summer. A number of overseas countries, such as the United Kingdom, France and other European countries have set high temperature records, and the China Meteorological Administration predicts that the hot weather above 35 ℃ in the Middle East, Southern Europe, the Midwest of the United States and other places may continue in the short term.

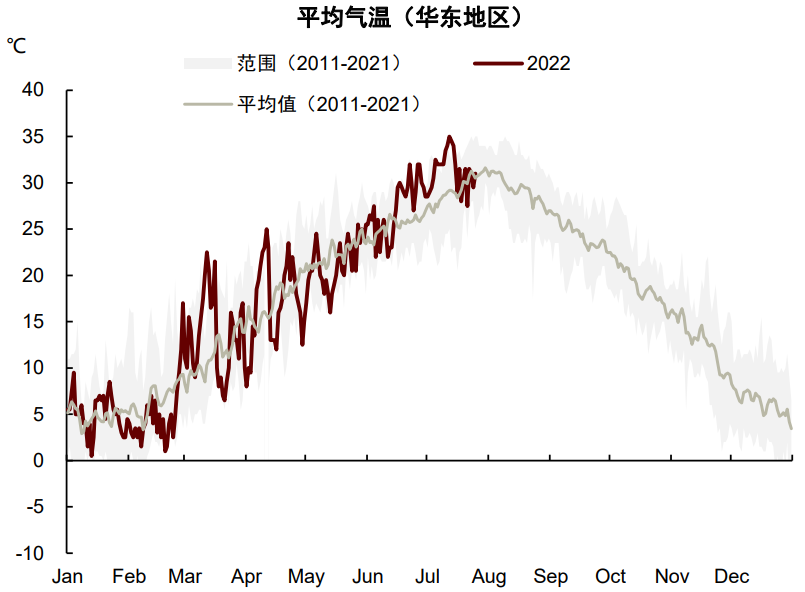

In China, the average temperature in July was 23.2℃, 1 ℃ higher than that in the same period of the normal year, the second highest in the same period in history since 1961 (second only to 2017). The daily highest temperature at 245 national weather stations broke through the July peak. The China Meteorological Administration predicts that the continued high weather in central and eastern China will be alleviated after the 9th of this month.

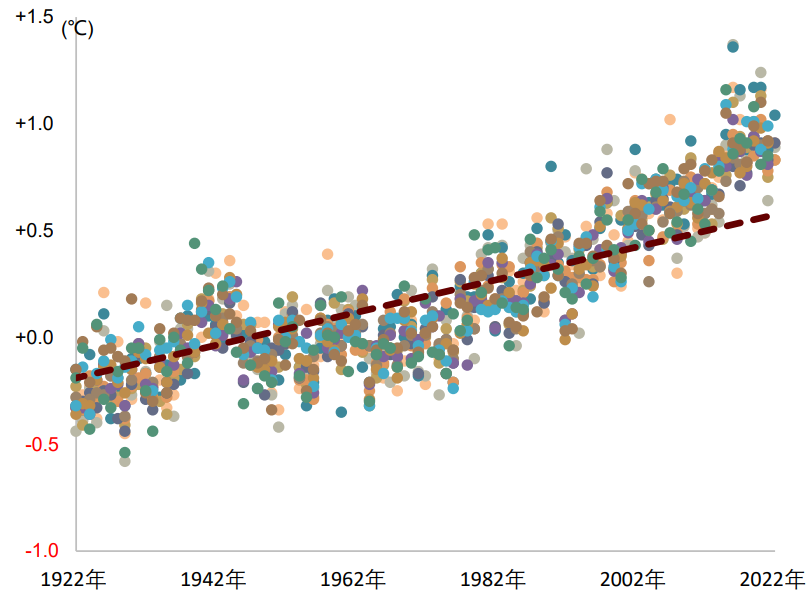

Globally, according to NASA, global temperatures have risen in almost all months since 1980, especially in the past decade. The National Climate Center's view also suggests that extreme high temperatures may become more frequent.

Chart 1: the domestic temperature this summer is significantly higher than the historical average.

Source: iFind, China International Capital Corporation Research Department

Figure 2: the monthly global temperature has risen significantly since 1922

Source: NASA, CICC Research Institute, China International Capital Corporation Research Department

While the temperature is high, the demand for coal has increased around the world. Coal consumption in Europe, the United States and other developed economies has continued to decline over the past 20 years, but coal demand has bucked the trend since last year. Gas-coal conversion caused by the risk of natural gas supply in the context of the conflict between Russia and Ukraine is still the most important factor. We believe that the extra energy demand in extreme weather may make the energy shortage "worse".

IEA expects global coal demand to grow 0.7 per cent to 8 billion tonnes in 2022, returning to the highs of a decade ago.

With geopolitical risks uncertain, we expect gas tensions in Europe to be difficult to ease in the short term, and high gas prices may continue to support coal demand during the year. We have seen European countries delay the coal withdrawal process. For example, the German government issued a decree allowing some closed coal-fired power plants to restart until April next year, and the Dutch government decided to lift restrictions on coal-fired power generation between 2022 and 2024.

WoodMac estimates that Europe has rescheduled 10GW's coal power capacity, corresponding to an annualized coal demand of about 3000-40 million tons. Data show that coal consumption in Europe has risen anti-seasonally since June. Coal consumption in Germany has increased by about 14.5% year-on-year, an increase of 34.7% over the average of the past three years, while coal consumption in the Netherlands has increased by 25.2% year-on-year, an increase of 61.2% over the average of the past three years.

IEA expects European coal consumption to grow by another 7% in 2022 and 14% in 2021. The demand for coal in India, Japan, South Korea and other places has also increased to varying degrees.

Figure 3: German coal consumption is rising against the trend this summer

Source: Refinitiv, China International Capital Corporation Research Department

Figure 4: Dutch coal consumption is rising against the trend this summer

Source: Refinitiv, China International Capital Corporation Research Department

High temperatures also support high domestic coal demand, but coal prices remain generally stable: in China, even with negative factors such as manufacturing recovery slightly less than expected, strong electricity consumption at high temperatures also supports high demand for thermal coal, but the overall performance of coal prices remains stable.

The epidemic situation at the end of the first quarter and the beginning of the second quarter repeatedly suppressed the demand for electricity and coal, but the economic repair after the epidemic was superimposed by high summer temperatures, and we saw a rapid rebound in electricity consumption and greater power pressure in some areas during the rush hour.

Hydropower, which produced more power in the early stage, was not sustainable, which also increased the burden of thermal power. The average inflow of the three Gorges Hydropower Station in July decreased by 35.3% compared with the same period last year, and it also decreased by 16.8% in June compared with the same period last year. The national hydropower generation capacity has turned into a negative growth range since mid-July. At the same time, thermal power generation across the country increased in mid-July compared with the same period last year, and the daily thermal coal consumption of power plants in eight coastal provinces reached the highest level since 2017 in early August.

Chart 5: the inflow of the three Gorges has declined since July.

Source: Wind, China International Capital Corporation Research Department

Chart 6: national thermal power generation became regular in mid-July compared with the same period last year.

Source: CCTD, China International Capital Corporation Research Department

Figure 7: daily thermal coal consumption of power plants in eight coastal provinces reached the highest level since 2017 in early August.

Source: CCTD, China International Capital Corporation Research Department

Figure 8: daily thermal coal consumption of power plants in 17 coastal provinces also continues to rise.

Source: CCTD, China International Capital Corporation Research Department

But at the same time, some energy-intensive manufacturing industries are still relatively weak, dragged down by the real estate side. The manufacturing PMI data in July showed that the manufacturing sector fell into a contraction range, with production, new export orders and other indicators falling, or suppressing the growth of electricity consumption in the manufacturing sector as a whole.

In terms of industrial coal, cement production has declined significantly compared with last year, the capacity utilization of weekly cement clinker has dropped by about 19.8ppt compared with the same period last year, and methanol production has rapidly fallen back to the year-on-year contraction range since July.

Figure 9: cement clinker capacity utilization continues to decline

Source: Mysteel, China International Capital Corporation Research Department

Figure 10: methanol production has fallen rapidly since July to a year-on-year negative growth range

Source: Wind, China International Capital Corporation Research Department

Looking ahead, we expect that the persistence of high-temperature-driven coal demand may be weak and may fall back after the high-temperature weather abates. But we have seen some signs of a pick-up in the physical workload of infrastructure recently. The indicators such as infrastructure investment and medium-and long-term loans for enterprises in the first half of the year all reflect the relatively strong potential energy of infrastructure growth, but affected by the epidemic situation, transmission delay and other factors, the construction is obviously lower than expected.

We expect that the early investment in the second half of the year may be effectively implemented, and the demand related to infrastructure may increase month-on-month, which will give a boost to the demand for coal. Overall, we believe that the high level of daily coal consumption this summer may be over, and demand will gradually slow down later on.

The pressure of energy supply remains this winter, overseas may face greater risks.

Although the summer high temperature period is passing, we believe that the tension in the global seaborne thermal coal market may continue and there may still be some price upside risks this winter. Basically consistent with our price performance judgment in the 2H22 outlook "from supply outage panic to volume reduction balance", the order of overseas energy price performance since the second half of the year is natural gas > coal > crude oil.

Although overseas is also facing the possible drag on energy consumption caused by the slowdown in demand after the opening of the interest rate raising cycle, thermal coal prices in Europe and other places have recently fallen slightly from high levels, but still remain at an all-time high of more than US $300 / tonne. We believe that the core logic of high overseas thermal coal prices still lies in the risk of rising natural gas shortages in Europe and other places. Behind it is the great challenge faced by the European energy supply system under the background of short-term "Russia-Ukraine" impact and long-term green transformation.

Chart 11: overseas coal prices have recently fallen from their highs, but they are still substantially inverted with those at home.

Source: Wind,Bloomberg, China International Capital Corporation Research Department

Figure 12: the price of natural gas is much higher than the conversion parity price of gas and coal

Source: Refinitiv, China International Capital Corporation Research Department

► high fossil energy prices may force Europe to accelerate the development of renewable power, but "distant water cannot quench its thirst": as can be seen from the recently proposed plans such as RePowerEU, Europe may accelerate its energy decarbonization process in the medium to long term to get rid of its dependence on Russian fossil energy imports, but we believe that Europe may still have to restart coal power to meet its immediate needs in the short term.

WoodMac data show that Fengfeng water accounts for about 52% of the total installed capacity of EU power generation in 2021, but together they accounted for only about 32% of EU electricity generation that year. The share of coal electricity increased from 13.7% in 2020 to 17.3% in 2021, while the share of natural gas power generation fell from 20.4% to 17.8%.

Subject to natural conditions, the number of hours of power generation of renewable energy is generally lower than that of fossil energy and nuclear power, and the room for improvement is limited. CICC Dianxin Group expects that the new installed capacity of photovoltaic in Europe will increase by 60% 100% to 40GW-50GW in 2022 compared with the same period last year, and there is also more room for growth in the new installation of wind power.

RePowerEU plans to increase the EU's share of renewable energy from 40 per cent to 45 per cent by 2030. In view of the high price of fossil energy, the economy of global new energy is indeed better than that of traditional fossil energy in terms of unit power generation cost. according to CICC, the average costs of centralized photovoltaic and wind power in 2021 are 7.5 times and 1.6 times lower than those in 2009, respectively.

However, it can not be ignored that the improvement of the permeability of renewable energy in the power system will magnify its intermittent and volatile defects, which will also increase the cost of the power system to ensure stable operation. While fossil energy is still a natural energy storage medium, before the large-scale application of energy storage technology, the matching of electricity demand and supply will still rely on natural gas and coal inventory.

Therefore, we believe that on the power generation side, the replacement of renewable energy to fossil energy may be difficult to achieve overnight, and the uncertainty of natural gas supply overlaps the limited utilization efficiency of renewable energy. Coal may still be an important part of the energy balance this winter. The gap in energy consumption will be filled by the increase of coal power generation or the reduction of its own energy consumption, and the prices of natural gas, coal and electricity will rise to achieve the rebalance between supply and demand.

Chart 13: the total amount of scenery and water in the installed capacity of EU power generation in 2021 is about 52%.

Source: Wind,Bloomberg, China International Capital Corporation Research Department

Figure 14: electricity generation hours of renewable energy are generally lower than those of fossil fuels and nuclear power

Source: Wind,Bloomberg, China International Capital Corporation Research Department

In addition to electricity, ► heating demand this winter may be a bigger challenge: for Europe, the pressure of this winter's peak energy consumption season is not just on the generation side, heating side demand or greater challenges.

From the historical data, we can see that the consumption of natural gas and coal in Europe has strong seasonality. At present, summer still belongs to the off-season of consumption, and the demand for natural gas in winter is often more than twice that in summer. The gap in demand for coal between winter and summer may reach three times.

As can be seen from chart 15-18, the seasonal driving force of gas and coal consumption lies in the heating demand of residents, and the heating demand of natural gas accounts for more than 60% of the total demand in winter. According to the China Gold Home Appliances Group, the current heating structure in Europe is still dominated by boilers, natural gas still occupies the dominant low position, and some coal and heating oil, there are relatively few alternatives.

At the same time, residential heating demand is also more rigid than industry and other fields, which means greater upward flexibility for the prices of natural gas, coal and other varieties.

Figure 15: natural gas demand in winter is often more than twice that in summer

Source: Eurostat, China International Capital Corporation Research Department; Note: the five Western European countries are the United Kingdom, France, Germany, Italy and the Netherlands, the same below.

Figure 16: natural gas consumption is highly seasonal

Source: Eurostat, China International Capital Corporation Research Department

Figure 17: the main driver of the seasonality of natural gas consumption is heating demand

Source: Eurostat, China International Capital Corporation Research Department

Figure 18: industry and electricity consumption are relatively weak seasonally

Source: Eurostat, China International Capital Corporation Research Department

► natural gas supplies still face considerable uncertainty and risk premiums will support coal prices: an European embargo on Russian coal is due to fall on August 10 and an embargo on oil products is gradually in place. Natural gas trade is also facing the risk of "sanctions" and "anti-sanctions". In the short term, Europe's energy system will still rely on "precarious" natural gas, and coal will not be left alone.

Figure 19: European coal imports have been high for the past six months

Source: Refinitiv, China International Capital Corporation Research Department

Figure 20: global coal exports have increased since the outbreak of the conflict between Russia and Ukraine

Source: Refinitiv, China International Capital Corporation Research Department

In terms of European coal supply, European coal imports have been high in the past six months under strong demand and high prices. Shipping data show that before the ban, Europe is still stepping up imports of Russian coal, while Australian coal is also growing rapidly.

Port coal stocks have also climbed rapidly to their highest level since the end of 2019. At the same time, natural gas supply still faces greater risks. We can see that the early maintenance of the Beixi No. 1 pipeline once intensified the market's concern about the outage of natural gas supply, but after the maintenance, the natural gas transport volume of the pipeline between Russia and Europe was still at a low level, and the natural gas price of TTF in the Netherlands rebounded to 60 US dollars / MMBTU.

The high gas price supports the coal price through the gas-coal conversion on the generation side. The current natural gas price is much higher than the gas-coal conversion parity, which means that considering factors such as carbon price and power generation efficiency, the cost of natural gas power generation is still higher than that of coal power generation.

Assuming that the efficiency of coal-fired and gas-fired power stations is 36% and 49% respectively, then a ton of 6000 calories of coal is equivalent to about 495 cubic meters of natural gas. In the first seven months of this year, natural gas consumption in the five Western European countries (Britain, Germany, Italy, the Netherlands and France) fell 12.2 per cent / 24472 million cubic meters compared with the same period last year. We assume that 30 per cent of this is a reduction on the generation side, if this reduction is made up entirely by coal and electricity, it is equivalent to 14.8 million tons of 6000 calories of thermal coal, equivalent to 34 per cent of the total thermal coal imports of the five countries in 2021.

Thus it can be seen that the reduction of natural gas supply will bring greater pressure to coal consumption.

Figure 21: rough calculation of coal instead of gas on the power generation side

Source: Refinitiv, China International Capital Corporation Research Department

Therefore, we believe that the current process of replenishing natural gas in Europe will indirectly affect the pressure on coal supply this winter. As of early August, the filling rate of European natural gas stocks was 71 per cent, meeting the 63 per cent target set by the European Commission and absolute filling about 5 per cent below the level of the same period 2016-2020.

The European heating season generally begins in November and lasts until March of the following year, so off-season inventory repairs need to be completed by the end of October, with a filling rate of 80% (new European Commission target)-90% (historical average).

At present, European LNG imports remained at a high level in July, with part of the reduction caused by the damage to US LNG export capacity made up by Norway's LNG import, gas consumption reduction in the stacking industry and power sector, and supporting inventories continuing to be repaired.

Looking ahead, the risk of Beixi 1 PNG imports or even a total outage of Russian gas supply is still likely to be the biggest uncertainty for European gas inventory repairs and peak gas consumption season this winter, especially for countries such as Germany, which are relatively dependent on Nord River 1.

The energy crisis in Europe may further tighten the global seaborne coal market this winter: in the global seaborne coal market, in terms of trade volume, the Asia-Pacific region, including China, India, Japan and South Korea, remains the main market. Europe is a relatively small buyer.

Europe imported about 56 million tons of thermal coal in 2021, accounting for about 5.8 per cent of global imports. However, we believe that the shortage of energy supply in Europe will have a strong spillover effect on the global market. After the landing of the Russian coal import embargo, Europe will increase its imports of seaborne coal to deal with the energy shortage it may face this winter. At the same time, not only in Europe, but also the global surge in natural gas prices has triggered a gas-coal shift on the generation side of countries that rely on natural gas for power generation, and we expect coal demand in these regions to remain high this winter.

In addition, coal power still occupies a dominant position in India, Southeast Asia and other emerging markets, and its demand for coal will keep pace with economic growth. Therefore, even if seaborne coal prices have reached an all-time high, global seaborne thermal coal demand may still grow against the trend this year. We expect seaborne thermal coal imports from India, East Asia (Japan, South Korea, Taiwan of China) and Europe to increase by 6.9%, 1.7% and 8.6% respectively year-on-year in 2022.

But at the same time, the export of seaborne thermal coal may still be inflexible, under the combined action of weather, capacity bottleneck, domestic industrial policy and other factors, it may be difficult for Australia, Indonesia and other seaborne coal exporters to have a significant increase. We expect thermal coal exports from Australia, Indonesia and Russia to decline by 2.4%, 1% and 6.7% respectively in 2022 compared with the same period last year.

Factors such as torrential rains in the main coal mining areas caused Australia's thermal coal exports to fall by about 4.1% from January to May compared with the same period last year, while Indonesian thermal coal production increased by about 6.4% year-on-year, but exports fell by about 16.3%. This is mainly due to Indonesia's brief ban on coal exports in January this year, which led to a sharp drop in exports that month.

Russian coal exports are also subject to railway capacity bottlenecks, trade settlement and international embargoes and other factors. We may see an accelerated shift in the flow of Russian coal exports from west to east. After the landing of the European ban on Russian coal imports, Russian coal exports to Europe will basically stagnate, and India and other countries' coal imports to Russia may continue to grow rapidly.

We expect that the gap between supply and demand in the global seaborne coal market will further expand this winter, global coal stocks will usher in a certain test in the winter consumption season, and thermal coal prices will also face greater upward pressure. the replenishment phase before the heating season may respond in advance.

Moreover, at present, the contradiction between supply and demand in the global thermal coal market is still concentrated in high calorific value coal, and we expect that high calorific value coal may still maintain a substantial premium. We expect that overseas high calorific value thermal coal (6000kcal), such as Newcastle Thermal Coal and European ARA Coal, will remain high above US $350 / tonne this winter.

Chart 22: global thermal coal supply and demand may tighten further this winter

Source: WoodMac, China International Capital Corporation Research Department

In contrast, the steady supply and stable price of domestic coal continues to advance, effectively ensuring the stable operation of coal prices in the case of prosperous supply and demand. Since the "double limit" in the third quarter of last year, domestic production capacity has been continuously released. according to the State Bureau of Mine Safety Supervision, a total of 490 million tons of coal production has been increased since September last year, and the nuclear production has increased by 180 million tons per year so far this year. We see that the number of inventory days in the eight coastal provinces has dropped rapidly to about 12 days compared with the current peak consumption season, which is only about 2 days higher than the same period last year.

We expect that there may still be a strong demand for replenishment in coastal power plants after the summer peak.

Figure 23: thermal coal stocks in eight coastal provinces are falling all the way.

Source: CCTD, China International Capital Corporation Research Department

Figure 24: relatively abundant thermal coal stocks in 17 inland provinces

Source: CCTD, China International Capital Corporation Research Department

Looking forward, we expect that domestic coal supply will shift from phased to normal, with an average daily output of 12.12 million tons of raw coal in the first half of this year, and there may still be room for increase in the second half of this year. In terms of imports, domestic and foreign coal prices are still substantially upside down, and we expect the high price gap to continue to restrain the growth of imports. Customs data show that coal and lignite imports in July were 23.523 million tons, up 23.9% from the previous month, but still down 22.1% from a year earlier.

From the shipping data, we can also see that there has been a certain increase in coal imports recently compared with the previous period, indicating that there is still a certain demand for replenishment in coastal areas driven by strong demand. From a country-by-country point of view, Russian coal imports have grown rapidly since the beginning of this year, while Indonesian coal imports have also increased month-on-month.

Chart 25: there has been a gap between coal production and imports since the beginning of this year.

Source: national Bureau of Statistics, General Administration of Customs, China International Capital Corporation Research Department

Chart 26: shipping data show that China's coal imports from Russia and Indonesia have increased month-on-month.

Source: Refinitiv, China International Capital Corporation Research Department

Edit / ping