The energy sector rose more than 3 per cent to lead S & P; Tesla, Inc. fell more than 2 per cent to lead blue-chip technology stocks down; Walt Disney Company rose nearly 5 per cent to lead the Dow; Pinduoduo rose 5 per cent and NIO Inc. rose 4 per cent. The pan-European stock index hit a two-month high, with the oil and gas sector up nearly 2 per cent and GlaxoSmithKline PLC down more than 8 per cent.

The yield on 10-year Treasuries is up 20 basis points from Wednesday's low and has eased upside down from the two-year yield. The dollar index erased its daily decline after nearing a six-week low.

Crude oil rose more than 2% and hit a new high in more than a week, natural gas in the United States rose more than 8% to a new high in more than two weeks, natural gas in Europe hit a new five-month high, and electricity prices in Germany hit an all-time high. Gold temporarily leaves its high position for six weeks to stop three consecutive sunny days. Lun Nickel rose more than 5% to a six-week high, while Lun lead hit a two-month high in four days.

Following CPI in July, US PPI growth slowed more than expected in July compared with the same period last year, and recorded negative month-on-month growth for the first time in more than two years. In addition to easing inflationary pressures, the number of US first-time jobless claims rose for two weeks last week, nearing its highest level since November, signalling that labour market supply tensions are also easing. Analysts believe that CPI and PPI inflation data have brought good news that a soft landing is expected, but at present, we should be cautious that the outlook for the US economy is still uncertain and the Federal Reserve may continue to actively raise interest rates to suppress inflation.

The three major US stock indexes rose at least 1 per cent when they were at their new high in early trading on Thursday, while the energy sector led the S & P by nearly 4 per cent at midday, while blue-chip technology stocks fell under the pressure of a rebound in US bond yields. Tesla, Inc. 's sector and the medical sector led the decline, dragging down all three major indexes to close only the Dow to keep the rally. Walt Disney Company, whose quarterly results were stronger than expected and announced a big price increase for streaming platform Disney+, rose nearly 10% in early trading, leading the Dow higher.

Hot Chinese stocks followed the trend of A shares and Hong Kong stocks, which rose sharply and outperformed the market. At one point in early trading, Pinduoduo rose more than 9%, leading the Nasdaq 100 index. XPeng Inc., who closed up more than 9%, rose more than 10% in morning trading. NIO Inc. Motor, whose Hong Kong stock closed up nearly 8%, and Bilibili Inc., who rose nearly 4%, both rose more than 8% in midday trading and still beat the market. Of the two "demon stocks" that fluctuated sharply recently, Zhifu financing fell sharply in double digits, rising sharply two days before listing and falling for three days in a row. Shang Cheng Division rose nearly 7% in early trading and then fell.

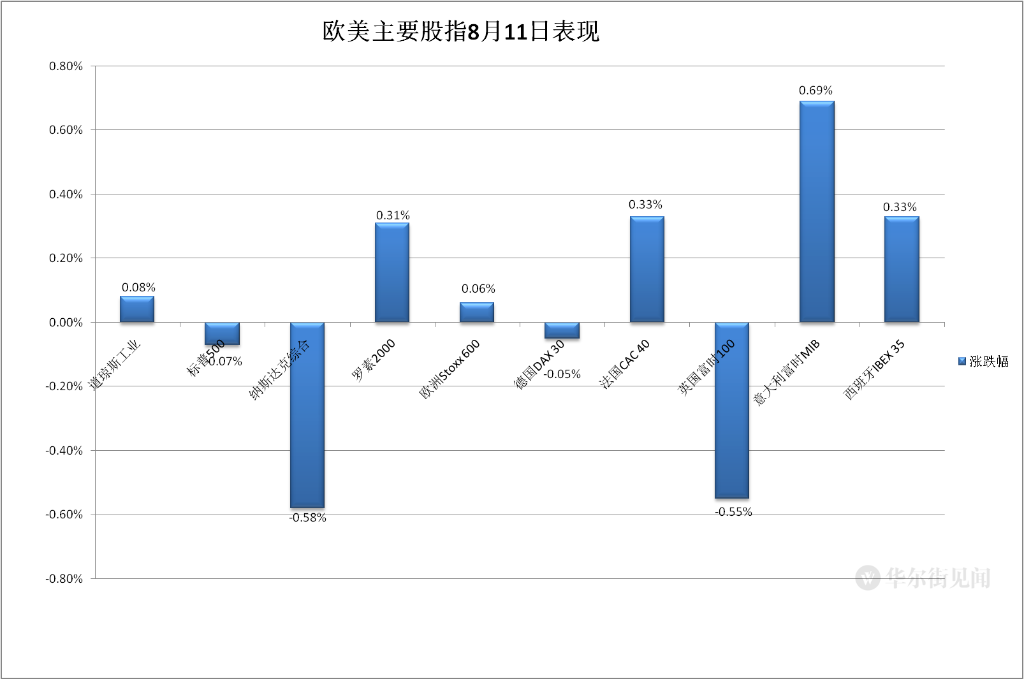

Investors are worried about the prospect of stomach medicine Zantac litigation in the United States, the share price of the pharmaceutical giant led by GlaxoSmithKline PLC fell, coupled with the poor performance of the mining stock Antofagasta, even British stocks performed worst among European countries. However, European stocks, like US stocks, were supported by energy stocks affected by the rise in crude oil, and the pan-European stock index finally closed higher, continuing to refresh its two-month high.

After the announcement of the US PPI, investors' expectations of the Fed's ultra-aggressive interest rate hike in September continued to cool, with US bond yields setting new lows and then gradually rebounding, with the benchmark 10-year Treasury yield rising 20 basis points from its one-week low set on Wednesday. The spread between two-year and 10-year US bonds, an important indicator of recession signals, has narrowed and the upside-down of yields has weakened, ending days of the biggest upside-down in more than two decades.

After the announcement of the PPI, the dollar index accelerated its decline as expectations of violent interest rate hikes by the Federal Reserve receded, approaching its low since late June set on Wednesday, and US stocks gradually wiped out their losses. The offshore renminbi, which has risen for three days against the dollar, Chevron Corp regained its recent high of 6.73 against the dollar after the PPI announcement, but fell off the one-month high set on Wednesday as the dollar rebounded and fell further.

Among commodities, after the International Energy Agency (IEA) raised its forecast for oil demand growth this year due to high summer temperatures in Europe and tight natural gas supply, international crude oil rose faster and the intraday rise expanded to more than 2%. When the risk of gas supply in winter increased, natural gas in Europe continued to refresh its highest level since March, and electricity prices in Germany continued to hit a record high. After Tesla, Inc. signed a $5 billion nickel purchase agreement with Indonesia, Lunni soared for days, closing at $23600 for the first time since the end of June, continuing to lead the rise in industrial metals. Risk aversion waned and gold, which continued to rise this week, fell back. New York gold futures fell from their highest level since late June, but held the $1800 mark.

Energy sector leads European and American stock market up, medical sector leads decline and outperforms the market. Walt Disney Company leads Dow Tesla, Inc. to lead blue-chip technology stocks lower.

The three major u.s. stock indexes continued to rise collectively, with the Dow Jones industrial average up more than 340 points, or about 1%, the s & p 500 up more than 1.1%, and the NASDAQ up more than 1.3%. At the end of morning trading, the Nasdaq fell short-term, the Nasdaq and S & P fell successively in midday trading, and the Dow also gave up most of its gains. In late trading, when the Dow turned short-term, when it refreshed its session low, the Nasdaq fell more than 0.7%, and the S & P fell more than 0.2%.

In the end, the three major indexes only closed higher, up 27.16 points, or 0.08%, at 33336.67, up for two consecutive days and both closed at their highest level since May 4. S & P closed down 0.07% at 4207.27 before falling for four consecutive days on Wednesday. The Nasdaq closed down 0.58% at 12779.91, giving up some of its gains at the end of three consecutive losses on Wednesday, barely entering a bear market after emerging from a bear market on Wednesday, and both s & p fell off its highest level since may 4 set on Wednesday.

Russell 2000, a small-cap stock index dominated by value stocks, closed up 0.31%, up three days in a row and outperformed the market for three days. The technology-heavy Nasdaq 100 index closed down 0.65%, falling back at the end of three consecutive losses on Wednesday and losing the market, but Chinese stocks led by Pinduoduo closed higher.

Commentators said that in early trading, the S & P 500 broke through the Fibonacci correction level of 4220, but in the end, US stock bulls failed to hold S & P above this important support level. There has never been a case of innovation low after rebounding through this support level during a bear market.

The S & P 500 failed to break through the important support level

Six of the S & P 500 sectors closed lower on Thursday, led by the healthcare sector, which fell more than 0.7 per cent, followed by Tesla, Inc. 's consumer discretionary products down nearly 0.7 per cent, real estate by nearly 0.6 per cent and Microsoft Corp's IT by nearly 0.6 per cent. Among the five rising sectors, energy rose more than 3 per cent, finance rose 1 per cent, industry and materials rose nearly 0.5 per cent and 0.3 per cent respectively, and Alphabet Inc-CL C's communications service rose slightly.

Leading technology stocks collectively closed down.Tesla, Inc. led the decline by more than 2.6 per cent, giving up most of Wednesday's gains of nearly 4 per cent. Among FAANMG's six largest technology stocks, Amazon.Com Inc, which rose more than 3 per cent on Wednesday to its highest level since April 28, fell more than 1.4 per cent, while Microsoft Corp and Alphabet Inc-CL C's parent company Alphabet both fell more than 0.7 per cent from their highs since May 4. Netflix Inc, which rose more than 6 per cent on Wednesday to its highest level since April 19, Netflix Inc, fell nearly 0.6 per cent. Facebook Inc's parent company Meta, which rose nearly 6 per cent on Wednesday to its highest level since July 21, fell nearly 0.5 per cent, while Apple Inc fell more than 0.4 per cent to bid farewell to its high since April 13.

Chip stocks go up and downThe Philadelphia semiconductor index closed down more than 0.3 per cent, and the semiconductor industry ETF SOXX fell more than 0.1 per cent. Among the IT stocks of the S & P 500, NVIDIA Corp, AMD and Broadcom Ltd fell about 0.9 per cent, while Seagate Technology rose more than 2 per cent, Intel Corp and Qualcomm Inc rose about 0.6 per cent, and Lam Research Corp and Applied Materials Inc rose about 0.5 per cent.

Energy stocks perform stronglySchlumberger rose by more than 5%, ConocoPhillips and Western Oil by more than 4%, Exxon Mobil Corp and Chevron Corp by more than 2%.

Among the more volatile stocks, investors are increasingly worried about the prospect of litigation related to Zantac, a drug to treat excess stomach acid, which was ordered off the shelves by the US FDA in 2020 because of the possibility of causing cancer. Pharmaceutical stocks all fell, with Pfizer Inc (PFE) closing down 3.3 per cent and GlaxoSmithKline PLC (GSK) US shares, which fell more than 8 per cent in London-listed European stocks. In addition, European shares of Paris-listed SAN closed down 3.3 per cent.

Among the stocks that reported results, Walt Disney Company (DIS) closed up about 4.6%, leading the Dow; Vacasa (VCSA), a holiday home rental management company whose quarterly profit was higher than expected and raised its annual guidance due to demand growth, closed up 33.2%; and glasses retailer Warby Parker (WRBY), which lowered its annual guidance but lost less than expected and had flat sales, closed up 19.5%. Cardinal Health (CAH), a medical services company with lower-than-expected quarterly revenue but higher-than-expected earnings, closed up 5.2%, while fashion brand RL, whose quarterly revenue and profit were both better than expected, closed up 3.9%. Sonos (SONO), a high-end audio brand with lower-than-expected quarterly profits and revenue and lowered its full-year guidance, closed down nearly 25 per cent, while Six Flags (SIX), a theme park operator blamed for a 22 per cent drop in attendance in the second quarter, closed down 18.2 per cent. Dating App Bumble (BMBL), which lowered its annual revenue guidance and had a negative impact of $9.4 million caused by foreign exchange fluctuations, fell 8.6 per cent.

As a whole, hot Chinese stocks continue to rise and outperform the market.ETF KWEB and CQQQ closed up nearly 2.8 per cent and 1.8 per cent, respectively. The Nasdaq Golden Dragon China Index (HXC) closed 2.6 per cent higher. Of the four stocks on the Nasdaq 100th index, Pinduoduo closed up about 5%, JD.com 2.6%, NetEase, Inc 1.9% and Baidu, Inc. 1.1%. The new power of car-building has soared collectively. XPeng Inc., whose Hong Kong stock market closed up more than 9 per cent, NIO Inc. Motor, whose Hong Kong stock market closed up nearly 8 per cent, rose 4 per cent and Li Auto Inc. rose more than 3 per cent. Of the two "demon stocks", MEGL, which closed down about 90 per cent on Tuesday and 0.2 per cent on Wednesday, closed down more than 11 per cent, rising for two consecutive days and closing down for the third day in a row, while HKD, which closed down more than 2 per cent on Wednesday, closed down nearly 0.2 per cent. Among the other stocks, Tencent Music rose more than 6%, bit Digital, Kingsoft Cloud Holdings and Hong Kong stocks closed up nearly 4%, Bilibili Inc. and HUYA Inc. both rose more than 3%, iQIYI, Inc. rose nearly 3%, and BABA and Weibo, where Hong Kong stocks rose more than 4%, rose more than 2%. Tencent powder rose about 2%, while Renesola fell more than 5%.

As for European stocks, the pan-European stock index closed slightly higher for two days in a row. The European Stoxx 600 index hit its highest close since June 8 for the second straight day. Most of the major European stock indexes continued to rise, while British stocks ended three straight gains, while German stocks, which rebounded on Tuesday, fell slightly. 11 of the Stoxx 600 stocks closed higher on Thursday, while the oil and gas sector rose nearly 2%, far ahead of other sectors. Of the eight closing sectors, the medical sector, which fell more than 1%, led the decline, showing the decline of pharmaceutical stocks, while the basic resources of mining stocks fell more than 0.8%. Among individual stocks, Antofagasta, a London-listed mining stock with a 48 per cent drop in profits in the first half of the year, fell 2.2 per cent, followed by a 3.7 per cent drop by mining giant Rio Tinto PLC, with even Lei Ying shares performing worst in all countries.

The 10-year Treasury yield rebounded 20 basis points from Wednesday's low and the 2-year yield fell upside down.

The easing of inflationary pressures in the US has reduced safe-haven demand and investors continue to bet that the ECB may raise interest rates by 50 basis points in September. European government bond prices fell and yields rebounded, easily erasing Wednesday's decline. The yield on UK 10-year benchmark government bonds closed at 2.05 per cent, up 11 basis points on the day, breaking 2.0 per cent on the 4th of this week for the first time. The yield on 10-year German bunds closed at 0.97 per cent, up 8 basis points on the day and approaching 1.0 per cent in intraday trading. It is at a two-week high since July 28.

After the announcement of the US PPI, the yield on the US 10-year benchmark Treasury note broke 2.74 per cent before the session, and then recovered quickly. Us stocks broke 2.80 per cent in early trading and measured 2.90 per cent in midday, refreshing the high set on Friday since July 22nd, up about 12 basis points on the day, up nearly 23 basis points from the one-week low set on Wednesday, and about 2.89 per cent at the end of the day. 11 basis points higher.

The trend of 10-year Treasury yield in the last three days

After the announcement of the PPI, the yield on 2-year US Treasuries, which is more sensitive to the interest rate outlook, broke through 3.14% and fell by more than 7 basis points during the day, before continuing to recover. U.S. stocks flattened all their declines at midday, closing above 3.22% and rising about 1 basis point during the day. Spreads on two-year and 10-year Treasuries, an important early warning indicator of recession, narrowed to less than 40 basis points, reducing the upside-down of yields from 2000-year highs.

The recent three-day trend of the yield of all-maturity US bonds

The offshore RMB fell off its four-week high after wiping out its intraday decline after the dollar index approached a six-week low

The ICE dollar index (DXY), which tracks a basket of the dollar's six major currencies, fell below 105.00 before European trading, and the US PPI fell below 104.70 again after the announcement, nearing the intraday low set on Wednesday since June 29th, with an intraday drop of more than 0.5 per cent, far less than the biggest drop since June 16, which fell more than 1.6 per cent on Wednesday, and then gradually erased the decline.

By Thursday's close, the dollar index was below 105.20, down slightly during the day, while the Bloomberg dollar spot index also fell slightly, both falling for four days in a row.

The offshore RMB (CNH), which has risen for three consecutive days, fell back against the dollar, rising to 6.7215 in early trading and losing 6.73,6.74,6.74,6.74,6.74. after the announcement of the US PPI, US stocks lost 6.74and refreshed their daily lows to 6.7442 at midday, falling off the high since July 13, which broke through 6.72in midday trading on Wednesday. The offshore RMB was trading at 6.7438 yuan against the dollar at 04:59 Beijing time, down 207 points from late trading in New York on Wednesday.

Crude oil hit a new high in more than a week, US natural gas rose more than 8%, European natural gas hit a new five-month high, German electricity price hit an all-time high.

International crude oil futures closed higher for two consecutive days by virtue of intraday gains. When European stocks broke their daily lows at the beginning of the session, US WTI crude oil and Brent crude both fell nearly 0.8 per cent during the day. European stocks continued to rise after early trading, while US stocks rose more than 2 per cent in intraday trading. In the end, WTI September crude oil futures closed up 2.62 per cent at $94.34 per barrel, while Brent crude oil futures closed up 2.26 per cent at $99.60 a barrel, and both closed up more than 2 per cent for the first time since July 29th, setting a two-day high since Tuesday on August 2nd.

Natural gas in Europe continued to rise, but at a slower pace than on Wednesday. ICE UK gas futures, which closed more than 9 per cent higher on Wednesday, closed 3.03 per cent higher at 401.65 pence per kcal, rising for three consecutive days and closing at the highest level since March 8 for the first time since March 8. TTF benchmark Dutch gas futures, which rose nearly 7 per cent on Wednesday, closed 1.34 per cent higher at 208.11 euros per megawatt-hour and continued to rise for two days to a new high since March 8. In addition, the electricity price in Germany will rise 0.97% to 417.00 euros in the coming month. In the coming year, the electricity price in Germany rose 5.81% to 455.00 euros in late trading, setting an all-time high in intraday or late trading for eight consecutive days.

Us gasoline and natural gas futures continue to rise together. NYMEX September gasoline futures closed up less than 0.1% at $3.0715 a gallon, the highest since July 29, while NYMEX September natural gas futures closed up 8.19% at $8.8740 per million British thermal units, the highest since July 26.

Lun Nickel rose more than 5% to reach a new high in six weeks and lead reached a two-month high in four consecutive days. Gold temporarily left its six-week high and stopped three consecutive days.

London base metal futures rose across the board on Thursday. Lenny led the rally for the second day in a row, coming out of its trough since late July on Wednesday, with a rise of more than 5% on Thursday to its highest level since late June. Lun Copper also rose for two days in a row, continuing to break its highest level since the end of June, closing above $8000 for two consecutive days. Lun lead rose for six days in a row, hitting its highest level since early June for four consecutive days this week. Lun Zinc and Lunxi rose for three days in a row. Lunzhihua reached its highest level since mid-early June for two days in a row. Lunxi rose more than 3%, closing above US $25300 for the first time in a month. Lun Aluminum, which stopped rising four times in a row on Wednesday, resumed its rally, reaching its highest level since late June.

New York gold futures closed lower for the first time in four days of the week, while COMEX December gold futures closed 0.36% lower at $1807.20 an ounce, falling to a two-day high since June 29 on Wednesday, but closed above $1800 for the fourth day in a row. New York silver futures gave up all the gains that rebounded on Wednesday, while COMEX September silver futures closed down 1.8% at $20.35 an ounce.

Gold and silver trend in the last two days

Edit / somer