Source: CICC Macro, the original research headline "CICC Macro | Why is the US economic data weak and employment data strong? "

Analysts: Liu Zhengning, Zhang Wenlang, etc.

The agency believes that strong jobs and "sticky" wages could lead to a rapid rebound in aggregate demand and inflation, undermining the Fed's previous tightening efforts. As a result, in the context of a strong labour market, even if we see weaker economic data, the market should not underestimate the strength and sustainability of the Fed's tightening.

Although US GDP growth has been negative for two consecutive quarters, the non-farm data just released for July show that the labor market is still strong. How to understand that economic data is weak and employment data is strong?We think there are three possible reasons:1) Employment data are lagging behind.The downward trend of demand has not been fully reflected. 2) the economic recovery is structurally unevenInterest rate-sensitive sectors have been curbed by the Fed's rate hike, but demand for services has been resilient.3) Labor shortage increases enterprises'"preventive" willingness to hire.. The labor supply in the United States shrank after the epidemic, and companies tend to hire more people and lay off fewer people, resulting in a strong labor market performance.

Strong employment may keep the Fed's monetary policy tight, and the Fed may need a more "hawk" to curb inflation.. The labor force is both a producer and a consumer. Strong employment and high wage growth, which are good for demand, also make it difficult for inflation to fall quickly. In addition, the friction in the US labor market intensified after the epidemic, and the natural unemployment rate (NAIRU) rose, which means that the Fed needs to tighten more than ever before to completely curb inflation. From thisWe believe that the market should not underestimate the strength and sustainability of the Fed's rate hike, nor should it prematurely assume that the Fed will turn loose.

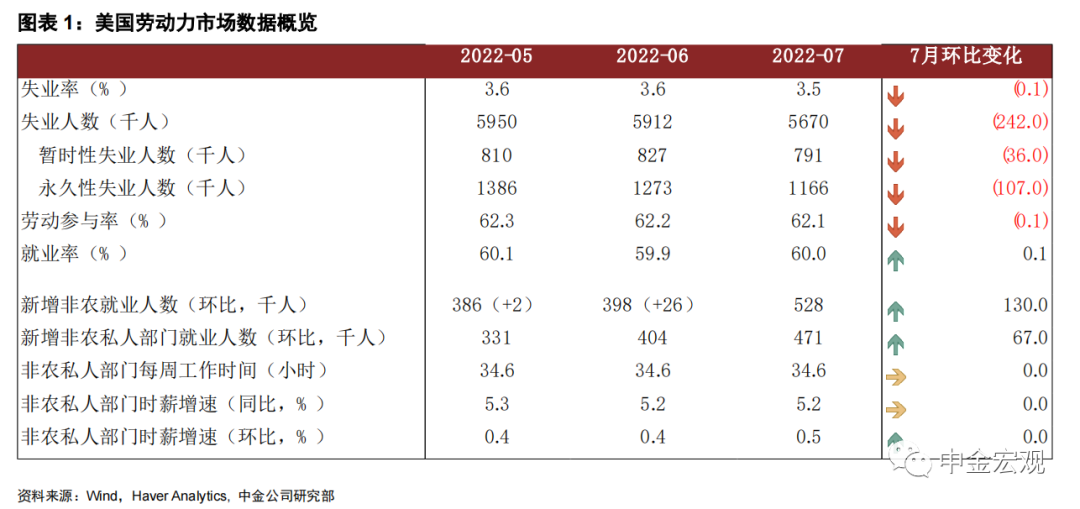

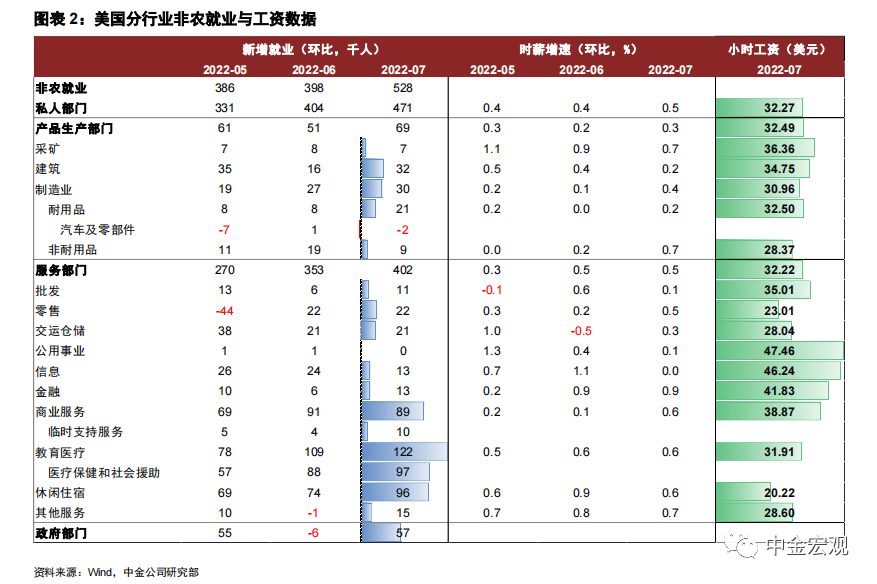

Let's take a look at the non-farm data first: 528000 new non-farm payrolls were created in July, a much higher-than-expected 250000. Overall non-farm payrolls have returned to pre-epidemic levels (February 2020), and the unemployment rate has fallen to an all-time low of 3.5 per cent (chart 1).In terms of sectors, employment growth in the service sector is still very strong, with strong performance in leisure hotels (+ 96000), business services (+ 89000), and education and health care (+ 122000). There is still a gap between these industries and the level of employment before the epidemic, and there is still room for improvement in the future (chart 2). Despite the recent decline in investment in real estate sales and the decline in manufacturing PMI, employment increased in construction (+ 32000) and manufacturing (+ 30000). In addition, although consumer spending on goods also fell in the second quarter, employment in the wholesale industry (+ 11000), retail industry (+ 22000) and transportation and storage industry (+ 21000) was also increasing.

How to understand the poor economic data and strong employment data?

We think there are three possible explanations:

1) Employment data are lagging behind and do not fully reflect the downward trend of demand.History shows that employment indicators tend to lag behind, with companies generally reducing hiring or working hours rather than direct layoffs in the early stages of an economic downturn, so the impact of falling demand is not reflected in employment so quickly.

2) the economic recovery is structurally uneven, and the service sector is still resilient because of its late recovery.The recovery after the epidemic, real estate and durable goods consumption performance is very strong, but the service industry has been unable to recover due to the impact of the epidemic. Since the beginning of the year, as the Federal Reserve has raised interest rates and pushed up interest rates, consumption of real estate and durable goods has shown signs of weakening, but there is still room for improvement in the service sector because of insufficient early recovery, coupled with the fact that the service industry is not so much affected by interest rates. as a result, employment can still maintain strong growth.

3) Labor shortage increases the "preventive" employment willingness of enterprises, and enterprises tend to recruit more people and lay off fewer people.Supply shock is the main feature of the current epidemic, which is mainly reflected in the contraction of labor supply in the United States and the contraction of energy supply in Europe. In the case of labor shortage, in order to avoid not hiring, companies tend to hire more people and lay off fewer people, reflecting the very strong labor market. So far, the labor force participation rate in the United States is still low, with the July figure of 62.1%, down 0.1 percentage points from June, indicating that the labor supply is still difficult to recover in the short term.

The labor force is both a producer and a consumer. Labor shortage pushes up wages, benefits residents' income and increases the sustainability of demand expansion.Although labor shortage is also a supply shock, unlike the general supply shock that suppresses aggregate demand (such as rising oil prices suppressing household consumption), labor shortage does not restrain aggregate demand, but can push up wages and support the expansion of workers' income and aggregate demand. As a result, in the case of labour shortages, aggregate demand will fall more slowly and inflation will become more resilient. On the other hand, the current slowdown in the US economy is not enough to contain inflation.

More importantly, the labor market friction intensified after the epidemic, and the natural unemployment rate rose, which means that the unemployment rate needs to rise sharply in the future to contain inflation.. The natural unemployment rate is also known as the unaccelerated inflation unemployment rate (NAIRU). Theoretically, when the actual unemployment rate is lower than the natural unemployment rate, the actual output of the economy will be higher than the potential output, which will accelerate inflation. In order to control inflation, it is theoretically necessary for the actual unemployment rate to be higher than the natural unemployment rate, that is, at the expense of employment in exchange for price stability.

Research by Blanchard & Summers (2022) shows that the epidemic has led to increased friction in the US labor market, a decline in matching efficiency and a significant increase in natural unemployment rate. One evidence is that the Beveridge curve moves outward as a whole, that is, at a given vacancy rate, the unemployment rate becomes higher, showing that it is harder for job seekers to match job openings (figure 3). According to their calculations, from 2019 to 2022, the US labor market matching efficiency parameter fell from 1 to 0.8, and natural unemployment rose from 3.6% to 4.9%, an increase of about 1.3 percentage points (chart 4).In other words, in theory, inflation may need to rise above 4.9% in real terms.

One view is that the US can reduce inflation without rising unemployment on the grounds that as long as companies are less willing to hire, the gap between labour supply and demand will narrow and wage inflationary pressures will be much lower. However, according to the research of Blanchard & Summers, in theory, in order to achieve a decline in the willingness of enterprises to recruit (reflected in the decline in the vacancy rate) and the unemployment rate does not rise, the matching efficiency of the labor market must be significantly improved, and the Beveridge curve must move inward, which is almost difficult to achieve in a short time.

According to their research, the unemployment rate has usually risen after the vacancy rate has fallen in history.On average, in the 6, 12 and 24 months after the vacancy rate peaked, the unemployment rate rose by 0.3, 1.0 and 2.1 percentage points, respectively (chart 5). Looking forward, we believe that if labor market frictions do not ease, then the decline in the vacancy rate is likely to herald a rise in unemployment.

Finally, we believe that this US economic slowdown may be different from the past, from GDP to negative growth (technical recession), to the "cooling" of the labour market, and then to the fall of inflation, it may take a long process.As mentioned earlier, one difference between this time and the past is that the source of the supply shock is the contraction of labor supply, which will lead to a shortage of labor supply, which will push up workers' wages and support demand.

In addition, the lag in service recovery will also enable employment in the service sector to maintain a certain growth rate after weakening employment in other industries, thus making the overall labor market still look strong. The combination of the two factors may take a long time for the US economy to enter a full-blown recession, or the Fed may need to keep tightening until aggregate demand slows down across the board.

If the Fed "stops and stops" in raising interest rates and relaxes when it sees weaker demand in some sectors, strong jobs and "sticky" wages could lead to a rapid rebound in aggregate demand and inflation, undermining previous tightening efforts.Therefore, in the context of a strong labour market, even if we see weaker economic data, the Fed should maintain the trend of tight monetary policy, and the market should not underestimate the strength and persistence of Fed tightening.

Recent remarks by Fed officials are also consistent with the above judgment, and we do not think we can rule out the possibility that we can continue to make great strides to raise interest rates by 75 basis points in September.Since the interest rate meeting in July, some Fed officials have expressed their views on the prospect of raising interest rates. Among them, Brad, chairman of the St. Louis Fed, a hawkish representative on the FOMC vote in 2022, tends to raise interest rates "ahead of schedule" to ensure the Fed's credibility, and supports raising interest rates to 3.75% by the end of the year. 4%.

In 2023, Evans, chairman of the FOMC and chairman of the Chicago Fed, said it was "reasonable" to raise interest rates by another 50 basis points in September, but another 75 basis points "may not be a problem". Daley, chairman of the San Francisco Fed, said bluntly that no one should regard the recent sharp interest rate hike as a sign that the central bank is gradually withdrawing from raising interest rates. Mestre, chairman of the Cleveland Fed and the FOMC voting committee in 2022, expects the policy rate to exceed 4% by mid-2023, with the current federal funds rate range of 2.25% and 2.5%. According to her position, the Fed's rate hike process may continue until next year.

Edit / Corrine