The education track is still a good track, and the Kmur12 company, the vocational training head company and the "new education infrastructure", which are the first to transform, are more certain.

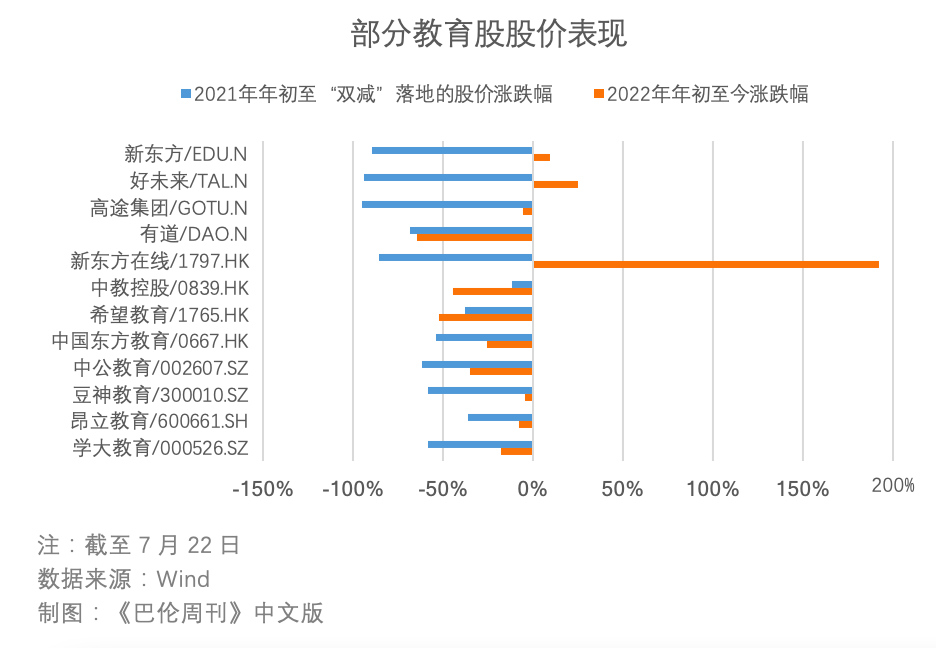

A year ago, on July 24, the "double reduction policy" was launched, and the K12 extracurricular tutoring industry suffered an unprecedented impact, and the impact also spread to other education stocks.

After the first anniversary of the "double reduction", are the education stocks still giving birth to investment opportunities? In mid-June 2022, the surge of New Oriental Education & Technology Group online (1797.HK) made people see the possibility of the transformation of teaching and training companies; going back in time is the increase in the popularity of vocational education and quality education after the "double subtraction"; and looking back, it is the "new education infrastructure" that begins to change the boundaries of the education track.

According to the Chinese version of Barron Weekly, the education track is still a good track, and investors can focus on three types of investment opportunities: (1) Kmur12, which is the first to complete the transformation and excellent profit performance, (2) industry leaders in the field of vocational training, and (3) enterprises that have established advantages in the field of "new infrastructure for education".

Kmuri 12 transformation, quality education becomes the key

Kmur12 discipline training is the sector most affected by the "double reduction policy" in the education industry. Take New Oriental Education & Technology Group online as an example, its semi-annual report stated that "as of November 30, 2021, the company has terminated Kmur9 business and plans to phase out Kmur12 business enrollment by the end of fiscal year 2022 (May 31, 2022). In terms of semi-annual results, Kmur12 education business accounts for 47.16% of New Oriental Education & Technology Group's total online revenue, which means that 270 million yuan in revenue will completely return to zero this year.

TAL Education Group (TAL.N) faces a similar situation; the company's annual report has shown the impact of a "double reduction", with revenues of $4.3909 billion in the 2022 fiscal year to the end of February, down 2.3 per cent from a year earlier. The company stopped providing Kmure 9 discipline training services in China in December 2021, which is expected to have a "significant negative impact" on the company's revenue in fiscal year 2023.

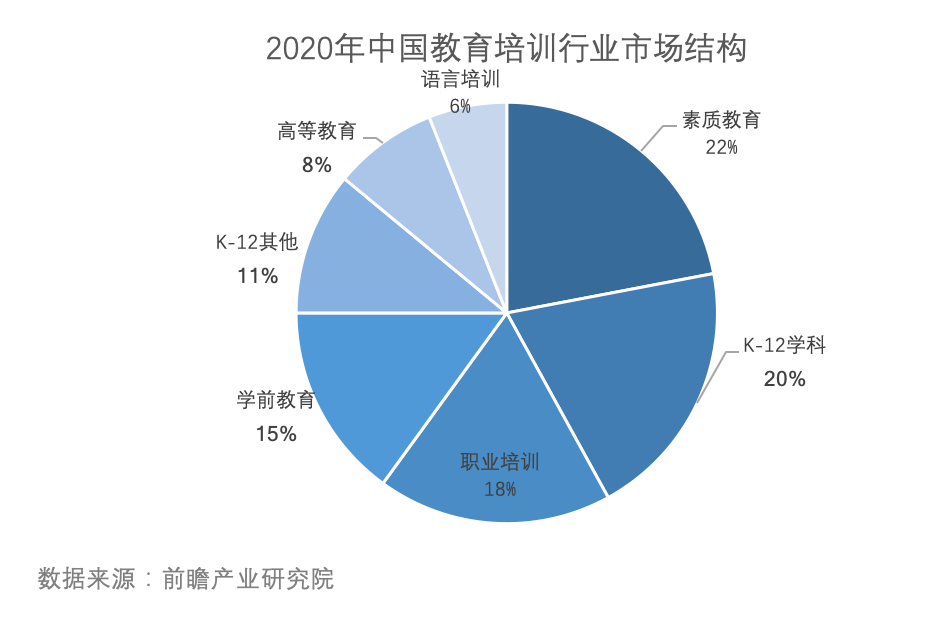

However, although the importance of Kmuri 12 discipline training in the past is self-evident, it is not the largest segment of China's education and training market before the "double reduction". According to the forward-looking Industrial Research Institute, the overall market size of China's education and training industry will reach 2.056 trillion yuan in 2020, with quality education accounting for the largest share (22%), followed by Kmuri 12 subject training (20%). In addition, the proportion of vocational training and pre-school education is not low.

In other words, from a more macro point of view, the overall market dispersion of the education and training industry is actually not low. The Chinese version of Barron Weekly believes that after the "double reduction", there is a greater possibility for the major companies to transform Kmur12 discipline training into quality education. The reasons include:

First of all, quality education is the strategic theme of educational reform and development. In March 2021, the quality Evaluation Guide for compulsory Education issued by the Ministry of Education and other six departments defines the key contents in five aspects: moral development, academic development, physical and mental development, aesthetic literacy, labor and social practice. in fact, it details the specific categories of quality education.

Secondly, as shown in the above picture, the market demand for quality education has always existed, and after the "double reduction", the demand for quality education has room for further growth. The forward-looking Industrial Research Institute predicts that the market size of quality education will expand to 604.6 billion yuan and 715.2 billion yuan in 2022 and 2023.

In addition, head education institutions have begun the layout of quality education business, which will, to a large extent, strengthen the importance of quality education in the whole education industry.

What needs investors' attention is that the diversity of quality education business can be interpreted as "complexity" on another level. To put it simply, quality education contains a wide range of contents, not only art, sports and other different education directions, but also STEAM, travel, research and other sub-division of the track. To a certain extent, the multi-layer connotation of quality education represents the further dispersion of market concentration, so the fierce degree of market competition can be imagined.

Therefore, the Chinese version of Barron Weekly believes that the former Kmur12 industry leader is expected to occupy a first-mover advantage in the process of quality education transformation. On the one hand, the hardware and software that these companies already have give them the basic conditions to complete the transformation more quickly; more importantly, the popularity of these companies and the large number of students accumulated in the past provide a greater possibility for them to revive. For example, TAL Education Group's English brand "Li Bu English" has changed its name to "Li Bu Children's Education" and launched new quality education products covering English drama, eloquence, aesthetic education, calligraphy, intelligence, chess and so on.

It is worth mentioning that, in addition to the transformation to quality education, New Oriental Education & Technology Group, who has attracted the attention of investors, has brought a lot of refreshing attempts to the transformation of educational institutions. In addition to "Oriental selection" to bring goods out of the circle, New Oriental Education & Technology Group's subsidiaries have layouts in 5G, e-sports events, hotels and catering management. After the policy benefits have been vacated and there is plenty of room for value return, these seemingly unrelated to education sparks are likely to rekindle investor enthusiasm.

Behind the "public craze for examination", there are both opportunities and challenges in vocational training.

The phrase "the end of the universe is compiled by Kao Gong" partly reflects the attitudes of young people and job seekers towards the job market and career planning. It also reflects the expansion of China's vocational training track to a certain extent. According to the data from the foregoing Research Institute, the market scale of vocational training in China in 2020 is second only to quality education and KMel 12 discipline training in the whole education industry. According to the Chinese version of Barron Weekly, vocational training will become an important subdivision track for education units.

One of the reasons is that, like quality education, industry policies tend to tilt towards vocational training. As early as May 2019, the State Council clearly defined vocational skills upgrading action as an important livelihood project in the Vocational skills upgrading Action Plan (2019-2021). In December 2021, the Vocational skills training Plan of the 14th five-year Plan made it clear once again that carrying out large-scale vocational skills training is an important measure to enhance the employment and entrepreneurial ability of workers, alleviate the contradictions in structural employment, and promote the expansion of employment. it is an important support for promoting high-quality development.

Another reason for the development of vocational training in recent years is the intensification of competition in the job market, which pushes up the market demand for vocational training. According to China's Ministry of Education, the number of college graduates of the class of 2022 is 10.76 million, an increase of 1.67 million over the same period last year, reaching an all-time high in both scale and increment. Taking the civil service recruitment examination of the central authorities and their directly affiliated agencies as an example, data from the State Administration of Civil Service show that a total of 2.123 million people have passed the qualification examination of employers, with a ratio of about 68:1 to the number of employment plans.

In addition to the "public craze for the examination", job seekers and in-service personnel in other industries and fields have begun to "recharge", "textual research" and "make up for deficiencies" for many reasons, such as self-improvement, the pursuit of high salaries, enhancing market competitiveness, alleviating employment pressure, and so on. it has also intensified the popularity of the vocational training market.

As a result, vocational training has also become one of the tracks for the transformation of Kmuri 12 institutions. Gaotu Techedu Inc. Group (GOTU.N) said in its 2021 annual report that its business focus will shift to professional courses, vocational training and electronics for adults after it stops providing Kmuri 9 and tutoring for high school students at the end of 2021 and February 2022, respectively.

In terms of professional courses, Gaotu Techedu Inc. Group mainly designs courses for in-service adults preparing for professional qualification examinations, including teacher qualification, chartered financial analyst qualification, CPA qualification, CPA qualification, securities qualification examination, etc., as well as postgraduate entrance examination, civil service examination and other training. In terms of vocational training, the company focuses on foreign language education, IT education and interest courses.

According to the 2022 China Vocational Education Industry report released by Dowhale Research, China's vocational education market is expected to exceed one trillion yuan in 2022 and reach 1.2 trillion yuan by 2024, which undoubtedly indicates a segment of the education track that is expected to usher in a dividend period. According to the data of the Seventh National Census, the number of people with university education in China has reached 218.36 million, and the average number of years of education for people aged 15 and over has risen from 9.08 to 9.91.

The Chinese version of Barron Weekly believes that the continuous improvement of the quality of the population will make vocational training enter the fast lane, among which the industry leaders with dominant market share and stable fundamentals have more investment certainty. But while seeing opportunities, investors can't ignore some potential risks--

First, due to different training objectives and requirements, vocational training continues the characteristics of low concentration in the education and training industry, and even the competition pattern is more differentiated. This represents that it is relatively difficult for a leading company to run out of a large volume in a certain field of training. From the point of view of the A-share education sector, apart from 002607.SZ, there is actually not much room for investors to choose from.

Second, the transformation of traditional education giants to vocational training is a long way. Take Gaotu Techedu Inc. Group as an example, from 2019 to 2021, its Kmur9 and high school subject training contributed 80.7%, 87.5% and 91.4% of revenue respectively. As a result, the training qualifications, teachers, product design and curriculum operation involved in the company's transformation to vocational training will not be a simple "change in old clothes and new clothes", but more like a complete change. In that case, business feasibility, cash flow level, performance return cycle and other concrete factors will consider the formation of this kind of investment target.

Third, even if the track is expanding, investors cannot ignore the performance impact of changes in the company's fundamentals. The half-year performance forecast for 2022 issued by Zhonggong Education on July 14 shows that the postponement of the examination and the prevention and control of the epidemic situation have a great adverse impact on the company's performance. It is estimated that the net profit attributed to shareholders of listed companies in the first half of 2022 is-720 million yuan to-920 million yuan, with a basic loss per share of 0.12 yuan to 0.15 yuan per share.

Compared with the losses caused by the epidemic, some market voices have criticized the products with high refund rates for public education. Secondary and public education adopts the form of "guaranteed classes", that is, after students pay high tuition fees, if they fail to pass the exam, the company will refund some or even all of the fees. According to the company's annual report, the company's rebate rate for the whole of 2021 has increased significantly compared with 2020, resulting in large fluctuations in the current performance. Zhonggong Education did not disclose the specific amount of refund, but the net cash flow generated by its business activities in 2021 decreased by 8.98 billion yuan compared with the previous year, a sharp drop of 183.93% compared with the same period last year. "the rapid growth of student refund" is one of the important reasons. So even if Zhonggong Education is one of the education stocks that were mistakenly killed last year, its share price is still lacklustre, down 34.86% so far in 2022.

New infrastructure for education, investment theme gradually clear

A policy that landed almost at the same time as the "double reduction" is the "guidance on promoting the Construction of a New Type of Educational Infrastructure and Building a High-quality Education support system", which clearly points out that by 2025, a new type of educational infrastructure system with optimized structure, intensive efficiency, safety and reliability will be basically formed. The Chinese edition of Barron Weekly wrote in a report last year that "new infrastructure for education" will become the key word for investment in the education track.

In fact, many listed companies have been included in the list of national industry-education integration enterprises issued by the National Development and Reform Commission and the Ministry of Education in July 2021: there are not only Chinese prefixes such as Aluminum Corporation Of China Ltd (601600.SH, 2600.HK, ACH.N), China Energy Construction (601868.SH), but also financial institutions such as Industrial and Commercial Bank of China (601398.SH, 1398.HK), China Construction Bank Corporation (601939.SH, 0939.HK), etc. There are also CSPC Pharmaceutical (1093.HK), Yutong bus (600066.SH), Luo Niushan (000735.SZ) and other different industries. From another point of view, the diversity of the extension of "new education infrastructure" makes the concept more complicated, making it more difficult for investors to choose individual stocks.

However, after a year of development, the investment theme of "New Infrastructure for Education" is increasingly converging to informationization. The China Business Industrial Research Institute predicts that China's education information market will reach 527.7 billion yuan in 2022. The Chinese version of Barron Weekly selected nine listed companies with business involvement in the field of information software and hardware from the list of national industry-education integration enterprises. It is obvious that in this year when the education industry was suffering from turmoil, their performance outperformed other education stocks.

The Chinese version of Barron Weekly believes that when betting on "new educational infrastructure" and educational informatization, there is still a need to be clear about specific stocks:

(1) even though the concept of "new infrastructure for education" has been confirmed at the policy side, not every company has explicitly reflected the concept at the business level. For example, the business of Lenovo Group Limited (0992.HK) is divided into "smart devices", "infrastructure solutions" and "solution services". Its investment in education business is hidden in "smart devices" and "programme services" respectively, and there is no detailed description of the income from education business. Lenovo Group Limited's annual revenue was $71.618 billion as of March 31, 2022, with "smart devices" and "solution services" accounting for 83 per cent and 7 per cent of the total revenue, respectively, according to the 202111.22 annual report.

Of the nine new education infrastructure stocks mentioned above, only iFLYTEK (002230.SZ) disclosed the education-related business in the financial report. In 2021, the company's revenue in the education sector rose 48.85 per cent year-on-year to 6.232 billion yuan, accounting for 34.04 per cent of total revenue, according to the annual report.

(2) before some stocks became "new education infrastructure" concept stocks, they had been marked with other labels by the market; more generally, due to the small volume of education-related business, there is great uncertainty as to whether the so-called concept tuyere can really drive stock prices up. The most typical example is Tencent (0700.HK), which, in broader market perception, is the leader of the Internet sector, rather than a technology company that exports its underlying capabilities in smart education.

To sum up, the Chinese version of Barron Weekly believes that in the future when the concept of investment in "new education infrastructure" is becoming increasingly clear, investors still need to judge value from business layout and performance fundamentals. In view of the fact that many of the targets of the "new education infrastructure" are more deeply rooted in the technical aspects such as big data, cloud computing and digitization, investors also need to see the impact of industry development and plate rotation on related stocks.

In his research report in July, Shen Wanhongyuan continued to be optimistic about the education industry, pointing out that "employment pressure has boosted the demand for academic qualifications, and the market for adult education has continued to improve", and maintained New Oriental Education & Technology Group's (EDU.N, 9901.HK) "buy" rating, suggesting paying attention to the layout of the leading institution on the corresponding track.

Huatai believes that the effect of the transformation of KM12 education to vocational education, quality education and educational informationization remains to be seen; but in terms of educational intelligence hardware, the organization has observed that some relatively leading players in subdivided tracks are gradually expanding their product categories to build a panoramic and personalized learning ecosystem. Huatai gave China Education Holdings (0839.HK), New higher Education Group (2001.HK), youdao (DAO.US) "buy" rating.

The content of this article is for reference only, and investment suggestions do not represent the tendency of Barron Weekly; the market is risky and investment should be cautious.

This article is from the official account of Wechat, Barron Weekly (ID:barronschina). Author: Lin Yidan, Editor: Wu Haishan, 36 Krypton released by authorization.