Overall, as external fluctuations and reduced policy support may affect the upward action ability of the market, CICC judged that the market may continue to consolidate in the short term.

CICC said in a research report that, on the whole, as external fluctuations and reduced policy support may affect the upward action ability of the market, CICC judged that the short-term market consolidation may continue. However, if the deviation trend of economic growth and policy cycle between China and the United States continues, CICC believes that the medium-term upward trend of the Hong Kong stock market will remain unchanged.

In terms of investment advice, in view of the current macro environment, CICC believes that sectors that provide certainty of cash flow will still be a good choice, such as certainty brought by dividend payment or certainty brought by predictable operating cash flow.

As a result, CICC recommends high dividend targets, such as banks, some utilities and the energy sector. In addition, CICC also recommends focusing on high-quality growth sectors where valuations are discounted and the regulatory environment is gradually improving, such as cars, medical devices, some Internet and consumer sectors.

The main points are as follows:

Last week, there was another significant correction in the overseas Chinese stock market. Although the record-setting inflation data in the United States in June also triggered some fluctuations in overseas markets,CICC believes that last week's correction in the overseas Chinese stock market may have more to do with internal factors.

Domestically, concerns about a possible slowdown in growth stabilization policies and resurfacing concerns about structural problems have suppressed short-term market risk appetite.In a sense, CICC believes that after economic growth shows signs of stabilizing, the policy strength may indeed slow down, especially in comparison with the larger disturbance stage of the epidemic from April to May. However, the economic data in the second quarter, especially the recent challenges facing the real estate market, show that the process of economic recovery is not completely solid, and more stable growth policies are still needed to support it.

Overseas, with the opening of the second quarterly report of US stocks and the further rise in inflation, the Fed is likely to raise interest rates again at the end of July.The US stock market may face some disturbance.The path of raising interest rates, coupled with the possibility that future inflation may remain high and weak earnings growth, may cause the external environment to remain one of the main sources of volatility in the Hong Kong stock market in July or even in the third quarter.

Looking forward, as investors gradually shift their focus to the actual effect of existing stable growth policies, and there is still uncertainty at home and abroad.CICC expects the short-term market to continue to consolidate and enter a relatively calm period before the situation becomes clear.

However, in an environment where economic growth and policy cycles deviate between China and the United States, domestic policy positions remain loose, market valuations remain attractive and southward capital inflows continue to prevent the overall upward trend of the Hong Kong stock market from being completely reversed in the medium term.

In this context, CICC believes that the search for certainty and high-quality targets, such as high-dividend stocks and high-quality growth stocks, may be a reasonable choice to help provide downside protection.

Market prospect

Similar to A-shares, there was another significant correction in the overseas Chinese stock market last week. Although the record-breaking inflation data in the United States in June also triggered certain fluctuations in overseas markets, CICC believes that last week's correction in the overseas Chinese stock market may have more to do with internal factors. For example, the relatively lower-than-expected economic data for the second quarter shows that China's economy is still some way from completing the repair, and still faces challenges from the imbalance between consumption and real estate. At the same time, the recent rebound of the epidemic in some cities has also increased market concerns about future growth prospects. More importantly, recent local real estate problems have raised investors' concerns about the health of the real estate market, resulting in the poor performance of the real estate sector.

Domestically, concerns about a possible slowdown in growth stabilization policies and resurfacing concerns about structural problems have suppressed short-term market risk appetite. While economic activity has clearly recovered from its April low and contributed to a significant rebound in the market over the past two months, investors have speculated that policy strength may gradually slow or even decline in the third quarter.

The recent higher-than-expected increases in China's CPI and pork prices, coupled with the people's Bank of China's persistently low reverse repurchase efforts, have also added to the market's concerns. In a sense, CICC believes that after economic growth shows signs of stabilizing, the policy strength may indeed slow down, especially in comparison with the larger disturbance stage of the epidemic from April to May.

However, the economic data in the second quarter, especially the recent challenges facing the real estate market, show that the process of economic recovery is not completely solid, and more stable growth policies are still needed to support it.

1) China's second-quarter data show that the economy is repairing, but the imbalance still exists. Specifically, China's GDP grew 0.4% in the second quarter from the same period last year, the slowest pace since the first quarter of 2020, mainly due to the significant negative impact of the rebound in the nationwide epidemic on the domestic economy, especially the weak recovery in the service sector. GDP in the second quarter included the negative impact of the April epidemic, but judging from the June data, the short-term impact on the production side has passed.

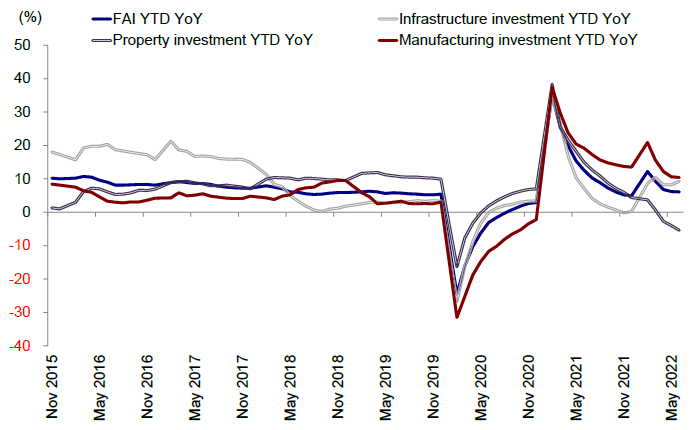

Specifically, exports rose 17.9 per cent in June from a year earlier, up from 16.9 per cent in May and the highest since January. Industrial production climbed to 3.9% year-on-year growth in June from 0.7% in May. The total amount of social zero was growing by 3.1% in June from a year earlier, a marked improvement compared with the 6.7% drop in May, but household service consumption is still weak. Fixed asset investment grew 6.1 per cent from January to June this year (vs. It grew 6.2 per cent in the first five months from a year earlier), mainly due to the strong performance of manufacturing and infrastructure investment in the first half of the year.

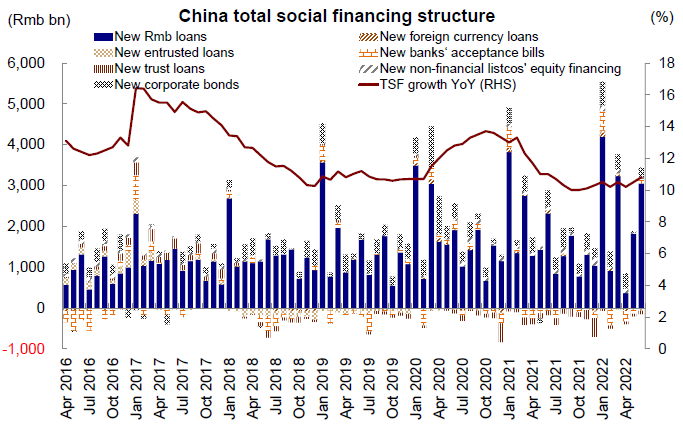

By contrast, real estate investment remains sluggish. Investment in real estate development rose again from-7.8% to-9.4% compared with the same period last year, reflecting the cautious use of land, slow start and weak investment in the context of deleveraging by real estate enterprises. In addition, after the data of social integration and M2 in May were significantly better than expected, the new social finance climbed further to 5.17 trillion yuan in June, driven by the effective implementation of a series of stable growth policies, an increase of 1.47 trillion yuan over the same period last year, but the structure may be more related to policy-supported infrastructure projects.

So overall, the June data showed a strong improvement and repair, but the overall recovery remains uneven and unstable.

2) the recent emergence of some risks in the real estate market has led to a rise in market concerns, which may require a rapid policy response. Given the current macro environmentCICC advised investors to keep a close eye on future policy signals, especially the mid-year Politburo meeting in July.

Overseas, the US stock market may face some disturbance as the second quarterly report of US stocks kicks off and the Fed is likely to raise interest rates again at the end of July after further inflation. Us inflation reached 9.1 per cent in June, the highest level in nearly 41 years. The likelihood that the Fed will raise interest rates by 100bp at its upcoming meeting has risen sharply following the release of higher-than-expected CPI data. Although this expectation is not certain given that fears of a recession are rising, another big interest rate hike in July is at least a high probability event for 75bp. This factor, coupled with the fact that future inflation is likely to remain high and weak earnings growth, may cause the external environment to remain one of the main sources of volatility in the Hong Kong stock market in July or even in the third quarter, thus causing disturbance to the Hong Kong stock market.

Overall, looking forward, as investors gradually shift their focus to the actual effects of existing stable growth policies and there are still uncertainties at home and abroad, CICC expects the short-term market to continue to consolidate and enter a relatively calm period before the situation becomes clearer. However, in an environment where economic growth and policy cycles deviate between China and the United States, domestic policy positions remain loose, market valuations remain attractive, and continued southward capital inflows also makeIn the medium term, the overall upward trend of the Hong Kong stock market will not be completely reversed.

In this context, CICC believes that the search for certainty and high-quality targets, such as high-dividend stocks and high-quality growth stocks, may be a reasonable choice to help provide downside protection. In the long run, more sustained upside will depend on whether current optimism translates into improved corporate earnings and growth. CICC advises investors to pay close attention to stable growth policy signals and earnings prospects to judge the short-term pace and upward momentum of the market.

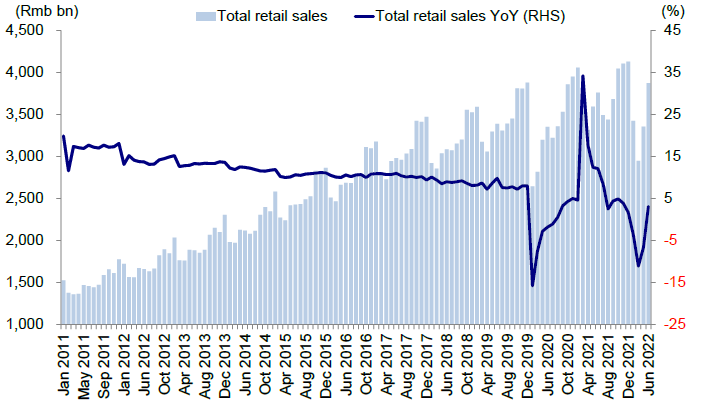

Chart 2: total social zero increased by 3.1% in June compared with the same period last year, showing a significant improvement compared with May-6.7%.

Chart 3: 5.17 trillion yuan of new social finance was added in June, an increase of 1.47 trillion yuan over the same period last year

Specifically, the main logic that underpins CICC's view and the factors that need to be paid attention to last week include:

1) Macro: the economic recovery continues, but the uncertainty remains.In the second quarter of 2022, China's GDP grew 0.4 per cent year-on-year, lower than expected and significantly slower than the 4.8 per cent growth in the first quarter. The service industry is a major drag. Apart from the fact that consumption of residential services is still weak, property-related services are also weak. Specifically, in the second quarter, the added value of the primary and secondary industries increased by 4.4% and 0.9% respectively compared with the same period last year, while the added value of the tertiary industry decreased by 0.4%.

June data show that the economic recovery continues, but consumption of household services is still weak.As industrial production continues to improve, the short-term shock on the production side has passed. Industrial production climbed to 3.9 per cent year-on-year in June from 0.7 per cent in May, with growth in everything from mining to electricity. On the demand side, total social zero was growing by 3.1% in June from a year earlier, a marked improvement compared with May-6.7%, indicating a strong rebound in the consumer industry driven by resumption of work and policy support.

Specifically, driven by a series of stimulus policies such as tax cuts and subsidies for new energy vehicles to the countryside, the recovery momentum of the automobile industry is the most obvious, leading the improvement trend of zero data in the whole society.

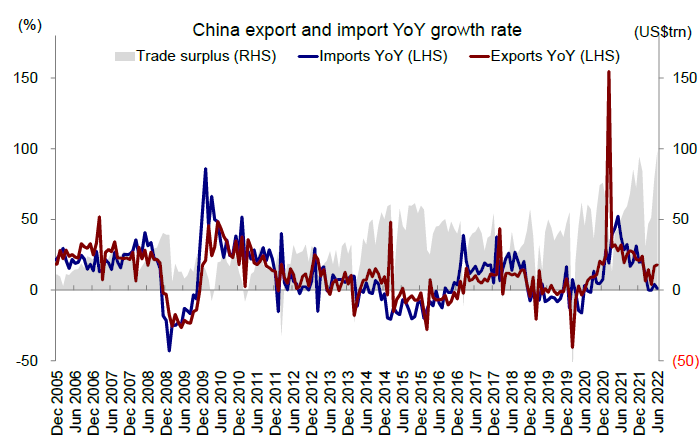

However, it is worth noting that the overall consumer expenditure on residents' services is still weak, such as-20.9% of the expenditure on education, culture and entertainment in the second quarter compared with the same period last year. At the same time, thanks to the improvement in the epidemic, China's exports rose 17.9 per cent in June from a year earlier, accelerating from 16.9 per cent in May. Import growth slowed to 1.0 per cent year-on-year in June from 4.1 per cent in May as commodity prices fell.

Manufacturing and infrastructure investment contributed to the growth of fixed asset investment, while the real estate sector remained weak.Fixed asset investment rose 6.1 per cent from January to June compared with the same period last year (vs rose 6.2 per cent in the first five months of this year), mainly due to strong growth in manufacturing and infrastructure investment in the first half of the year, rising 10.4 per cent and 7.1 per cent respectively.

By contrast, real estate investment fell 5.4 per cent from a year earlier, enlarged from a 4.0 per cent year-on-year decline from January to May. Monthly real estate investment climbed to 9.4 per cent year-on-year in June from 7.8 per cent in May, indicating limited supply and low demand.

Chart 4: fixed asset investment increased by 6.1% from January to June this year

Chart 5: China's exports rose 17.9% in June from a year earlier, accelerating from 16.9% in May.

2) currency: the better-than-expected financial data in June indicate that the policy of stabilizing growth has been implemented steadily, but it is important that credit needs to be further expanded in the future.After the financial data in May was significantly better than expected, the new social financing in June was 5.17 trillion yuan, an increase of 1.47 trillion yuan over the same period last year, which was higher than the highest expectation in the Wind survey. The strong growth in new social finance is mainly driven by government bonds, RMB loans and off-balance sheet bills.

Specifically, new medium-and long-term corporate loans improved significantly in June; along with the improvement in property sales, the year-on-year decline in new medium-and long-term household loans also narrowed. At the same time, M2 growth climbed to 11.4% year-on-year in June, surpassing the highest point in 2020.

3) earnings: the growth rate of earnings may slow significantly in the first half of 2022 and improve significantly in the second half of 2022.The report of overseas Chinese stocks is approaching in 2022 and will usher in the peak period of performance announcement in August. Based on China International Capital Corporation industry analysts' earnings forecasts for individual stocks, CICC's overall 1H22 earnings are expected to grow 5 per cent year-on-year in renminbi terms, down from 20 per cent in 2021.

CICC believes that the reason behind this is that a number of challenges, such as a rebound in the domestic epidemic, global supply shocks and sharp rises in commodity prices, have dragged down downstream demand and investment and led to a continued squeeze on profit margins in downstream industries.

Specific to all industry levels, CICC expects a significant decline in profits in the defensive sector, especially in the utility sector, which is more sensitive to upstream energy prices, while the energy, non-ferrous metals and transportation sectors are expected to boost cyclical industry earnings by 15 per cent in the first half compared with the same period a year earlier.

On the other hand, downstream industries (such as textiles, clothing and electronics) and real estate are likely to lag behind other industries in the first half of the year.

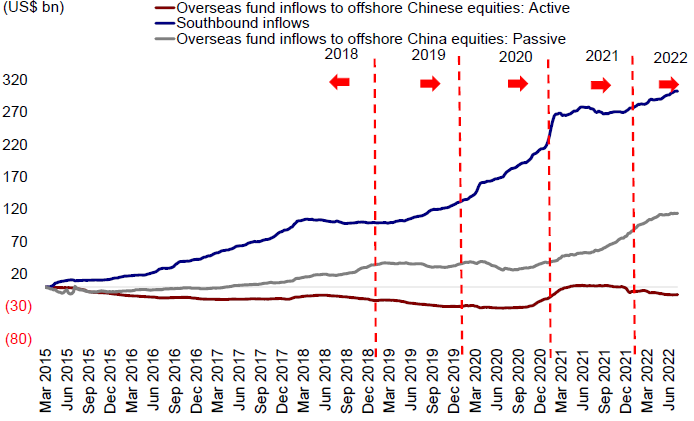

4) liquidity: southbound funds changed from net outflows in the previous week to net inflows, while overseas funds also showed inflow momentum.Chinese investors' enthusiasm for investing in the Hong Kong stock market through the Hong Kong Stock Connect recovered last week, with an average daily inflow of HK $488 million, down from HK $800m the previous week.

The total inflow of overseas ETF funds into the overseas Chinese stock market was $369 million, while the outflow of overseas active funds totaled $249 million last week. Overall, a total of $618 million of overseas capital flowed out of the overseas Chinese stock market last week, according to data from EPFR.

Chart 6: southbound funds changed from net outflows in the previous week to net inflows, while overseas funds also showed inflows into Chinese stocks.

Focus on events

1) China's economic growth and policy changes; 2) geopolitical situation; 3) epidemic changes; 4) Sino-US relations.

Edit / Viola