Author: Liang Zhonghua

Recently, market expectations for VAT reform have been rising. In response to the discussion in the market, this paper estimates two types of hypothetical tax reduction scenarios:

From the perspective of the whole historical trend, China's value-added tax reform has entered a new stage since 2017, simplifying and adjusting the multi-file tax rates after "business reform and increase". The government work report at the beginning of the year has already pointed out the direction of VAT reform of "three and two". In a recent interview, the Minister of Finance once again mentioned the importance of VAT reform.

We estimate two kinds of simulation scenarios, one is that the tax rate will be reduced by 1%, and the other is that the tax rate will be reduced in parallel, and the 10% tax rate will be reduced from 6% to 16% to 15% and 6%. The tax rate will remain unchanged. It is estimated through the relationship between input-output table, financial report data of listed companies, tax rate matching of all kinds of products and so on.

The general tax rate reduction plan is relatively mild, and the intensity of tax reduction is relatively strong. The tax rate will be reduced by one point, the whole market is expected to reduce taxes by 645.6 billion, and all listed companies are expected to reduce taxes by 157.5 billion yuan. Under the parallel tax reduction plan, the whole market is expected to reduce taxes by 1.2498 trillion, and all listed companies are expected to reduce taxes by 265.2 billion yuan.

If the tax rate is generally reduced by one tax point, the burden on the financial industry will be reduced more, and the tax burden on some manufacturing industries will be reduced relatively less. From a market-wide point of view, the service industry, especially the financial industry, has benefited more, while the manufacturing industry has benefited relatively less. among them, the textile, clothing, shoes, hats, leather, down and its products industry has been damaged in the process of tax reduction. From the perspective of listed companies, the actual tax reduction effect of real estate and financial industry is more obvious, while the actual tax reduction effect of steel, non-ferrous and other manufacturing industries is relatively small. After the tax reduction, it will be more beneficial to the profits of the commercial, retail, communications and extractive industries.

Under the parallel tax reduction plan, the benefits of the industry are greatly divided, and many industries may be damaged.In the market as a whole, the tax burden of the real estate, construction, agriculture, forestry, animal husbandry and fishing, transportation, warehousing and gas production and supply industries decreased significantly; the actual tax burden of nearly half of the industries increased instead, and the actual tax burden of accommodation and catering, food and tobacco, textiles and other industries increased more. From the perspective of listed companies, the tax burden of real estate, architectural decoration, transportation, public utilities, agriculture, forestry, animal husbandry and fishing has dropped significantly, while the tax burden of food and beverage, leisure services, banks and non-bank finance has increased in this plan. After the combined tax reduction, the profits of the industries such as architectural decoration, real estate, communications, transportation and commercial trade have increased greatly, but the profits of about 1. 4% of the industries have been damaged in the process of tax reduction. among them, the profits of leisure services and food and beverage industries have dropped more.

Under the parallel tax reduction scheme, enterprises with different attributes have obvious differences in the effect of tax burden reduction and profit thickening.The benefit of the central enterprises is obviously higher than that of other categories of enterprises, while the benefit of the public enterprises is not obvious, which is mainly due to the differences in the industry distribution of different types of enterprises, and the central enterprises account for a higher proportion in the industries where the tax burden decreases obviously, so the effect of tax reduction is more obvious, and the profits are thicker.

What reforms have been experienced in domestic value-added tax?

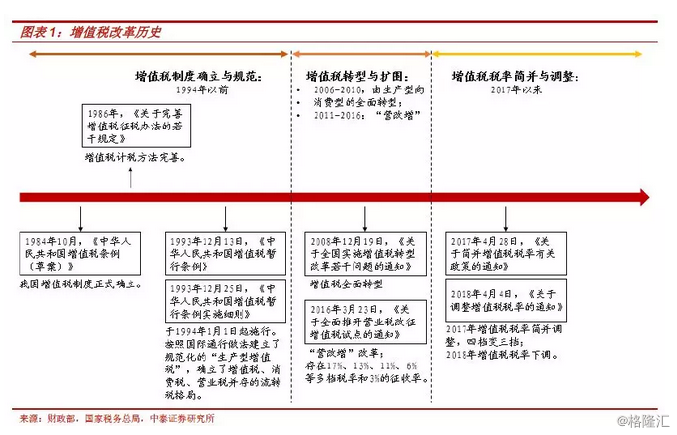

From the perspective of the whole historical trend, the reform of China's value-added tax system is roughly divided into three stages. The first stage is the establishment and standardization of the value-added tax system from 1984 to 1994. The interim regulations of the people's Republic of China on value-added tax and the detailed rules for the implementation of the interim regulations of the people's Republic of China on value-added tax have established the circulation tax pattern of the coexistence of value-added tax, consumption tax and business tax in China.

The second stage is the transformation and expansion of VAT from 2006 to 2016, in which VAT comprehensively transformed from production to consumption from 2006 to 2010, expanding the scope of income deduction and solving the problem of double taxation. The "business reform" reform began after 2011 and was carried out nationwide in 2016, breaking the circulation tax pattern of the coexistence of the three major taxes since 1994.

The third stage is the consolidation and adjustment of VAT rates since 2017. After the completion of the "business reform and increase", there are multiple tax rates of 17%, 13%, 11%, 6% and 3% in domestic value-added tax, and the tax collection and administration is more complicated. Two tax rate adjustments have been implemented since 2017, including the 2017 notice on policies related to the simplified VAT rate, which adjusted the tax rates from four to three (17 per cent, 11 per cent and 6 per cent). In the first half of this year, the tax rate adjustment document "notice on adjusting VAT rates" was issued again, reducing the tax rates of 17 per cent and 11 per cent by one tax point to 16 per cent and 10 per cent.

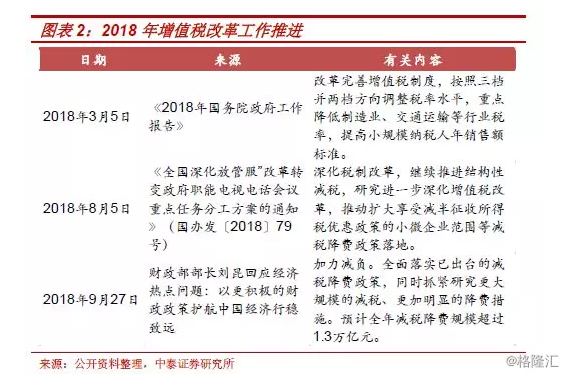

Recently, the market has paid more and more attention to the adjustment of value-added tax rate. In retrospect, the government work report at the beginning of this year already laid out the arrangement of this year's value-added tax reform plan, "adjusting the tax rate level in accordance with the third and second stalls." Notice on August 5, "National deepening Management and Service" Reform and Transformation of Government functions teleconference on the division of key tasks "once again made work arrangements for" studying the further deepening of value-added tax reform ". In an interview with Xinhua on September 27, Finance Minister Liu Kun mentioned "stepping up efforts to study larger-scale tax cuts and more obvious fee cuts." With the acceleration of the work arrangements of the relevant departments, the expectation of VAT tax rate adjustment in the market is gradually heating up.

There is no doubt that the three-file and two-file tax reduction plan will greatly reduce the tax burden of the main body of the market, but it still needs to be adjusted according to the pressure of fiscal revenue and expenditure in the process of VAT reform, so how will the VAT reform be carried out in the future?

We have made two kinds of scenarios: the first is a mild and gradual tax rate reform, and it is expected that the parallel tax reduction will be carried out step by step, first moderately reducing the tax rate, and then considering the merger. For the time being, this paper will use the general tax rate reduction of 1% to calculate the effect of the first step of moderate tax reduction. The second plan is a moderate parallel tax reduction. At present, the market is generally expected to abolish the 10% tax rate stall and merge it into 6%, with a moderate reduction of 16% tax rate. In this paper, in the process of calculation, it is assumed that the existing 10% tax rate will be merged into 6% file, and the 16% tax rate will be reduced to 15% 6% tax rate unchanged.

Second, how to calculate the value-added tax of different industries?

First of all, we briefly introduce the calculation method of this article, VAT = output tax-input tax = output tax base * output tax rate-input tax base * input tax rate, so in order to measure the VAT paid by different industries, we need to guide the corresponding tax rate and tax base of each industry.

1. Calculation of the tax rates of output tax and input tax

In the process of calculating the output tax rate in various industries, we have adopted some approximate treatment methods. Firstly, we match the input-output table industry with the CSRC industry, and compare it with the value-added tax rate of each tax item. If the tax items of multiple tax rates are involved in the industry, the average tax rate will be further calculated by using the revenue share of listed companies as the weight; if the revenue share of different tax items is difficult to split, we will use the mean or a certain fixed weight for approximate treatment, thus calculating the average tax rate of the corresponding output tax in the industry, as shown in the table below.

For the corresponding input tax rate of each industry, we combine the above output tax rate with the input-output table in 2015 to calculate. First of all, μ I is defined as the value-added tax rate of industry I products (that is, output tax rate), Xi is the amount of industry I products invested in the production process of a certain industry, and Yi is the final output amount of industry I.

that,

2. Calculation of the tax base of output tax and input tax

In the process of measuring the output tax base and input tax base, one scheme is to use the input-output table directly, then it is easy to get the output and input tax base of different industries, among them, output tax base (input-output table) = industry total output-inventory increase-export abroad; input tax base (input-output table) = intermediate total input. Another scheme is to use the data of listed companies to summarize by industry, so, output tax base (listed company) = business income, input tax base (listed company) = business income * direct consumption coefficient, in which the direct consumption coefficient of industry I is expressed as

It is worth noting that the operating income data of listed companies already include import sales data, while the total output in the input-output table does not include import data, so the VAT calculated by using the input-output table needs to be adjusted to:

VAT payable = output tax base (input-output table) * output tax rate-input tax base (input-output table) * input tax rate + import VAT

Third, if the tax rate is reduced by 1%, what will be the impact of the industry?

The impact of VAT rate reduction on the industry is more complex, tax rate changes will affect product prices, and industries with different bargaining power will benefit from significant differences. Generally speaking, companies with strong bargaining power can still maintain the high price of their products after the tax rate is reduced, so as to share more tax reduction profits.

However, if the change of bargaining power is taken into account, more measurement assumptions will be needed, resulting in a large deviation from the final calculation results. And in the long run, as long as there is sufficient competition, the high price of products after tax reduction will not be maintained forever, and the price will still return to the new equilibrium. Later, we will only consider the static calculation, that is, we will not consider the tax reduction effect and profit change caused by the price change.

1. Using the calculation results of input-output table.

According to the second part of the VAT payable, we define the actual tax burden = VAT payable / (output tax base + import amount).

According to the distribution of input and output of various industries in the input-output table in 2015, if the VAT rate of all industries is reduced by one tax point, the actual tax burden of each industry will fall by less than 1%. Among them, the service industry, especially the financial industry, benefits more, while the manufacturing industry benefits relatively less. Specifically, the actual tax burden in education, oil and gas extraction, real estate, finance and other industries has dropped significantly, while in the manufacturing industry, the textile, clothing, shoes, hats, leather, down and its products industry has been damaged in the process of tax reduction (the negative value in the figure indicates an increase in the actual tax burden), and the tax burden in manufacturing industries such as electrical machinery and equipment, textiles, wood processing products and furniture is also relatively less than that in other industries.

Industries with a large proportion of added value benefit more from the process of value-added tax reduction. Intuitively, VAT is a production link tax, which levies on the part of added value, so each reduction of a tax point will lead to a greater reduction in the actual tax burden of the industry with a larger proportion of added value. Our calculation results also support the above judgment. The following figure shows the comparison between the proportion of added value of each industry and the actual tax burden reduction of each industry after the reduction of one tax point, and there is basically a positive correlation between the two, that is, the industries with more added value, the greater the decrease in the actual tax burden. Therefore, it can be understood that the above sub-industry calculation results show that the financial industry accounts for a relatively high proportion of added value and benefits greatly in the process of tax reduction, while some manufacturing industries account for a relatively high proportion of intermediate investment, so the benefit of tax reduction is relatively small.

![image.png]()

2. the calculation results using the data of listed companies.

The advantage of input-output table data is that it can better match output tax and input tax, but the corresponding data year is 2015, the current output structure may have changed, so we further use the data of listed companies to make supplementary calculations. Similarly, we define here the actual tax burden = VAT payable / business income.

Based on the 2017 annual report data of listed companies, the results are similar to those of the above input-output table, the actual tax burden change of each industry is less than the policy reduction tax rate, in which the service industry benefits more and the manufacturing industry benefits relatively less. As shown in the following figure, if all industries reduce one tax point, the actual tax burden of each industry will be reduced by less than 1%. The calculation results of Shenwan industry classification and CSRC industry classification show that the actual tax reduction effect of real estate and financial industry is more obvious, while the actual tax reduction effect of steel, non-ferrous and other manufacturing industries is relatively small.

![image.png]()

Based on profit thickening = VAT reduction / net profit, we further measure the profit changes of various industries.

From the measured results, apart from synthesis, the industries with obvious increase in profits are concentrated in commercial trade (wholesale and retail). The effect of profit thickening is much higher than that of communications (information transmission, software and information technology services) and extractive industries (mining), which rank second and third.

Compared with the effect of tax reduction, the ranking of industries with thickened profits is not consistent, and the effect of tax reduction in service industries is more obvious, but the effect of profit thickening is not obvious, such as real estate, non-bank finance and banks, which rank among the top three industries with tax reduction effect. the effect of profit thickening ranked 10th, 12th and 27th respectively in the application-in-case industry.

![image.png]()

The profit thickening effect of the service industry is not obvious, which may be due to its high profit margin and large base. We compare the relationship between profit thickening and the change of tax burden and industry profit margin. Profit thickening is indeed affected by the actual tax burden, and the correlation between industry profit margin and it is also very significant. The higher the profit margin is, the weaker the profit thickening effect is.

![image.png]()

Fourth, if the value-added tax is merged, who will benefit and who will suffer?

This section will calculate the VAT parallel tax reduction plan, assuming that the 10% tax rate will be merged into 6%, and the 16% tax rate will be reduced by one tax point to 15%.

1. Using the calculation results of input-output table.

Based on the 2015 input-output table data, the industry with the most obvious effect of tax reduction in the parallel tax reduction plan is still the real estate industry, followed by construction, agriculture, forestry, animal husbandry and fishing, transportation and warehousing and gas production and supply industries. However, in the parallel tax reduction plan, the actual tax burden of nearly half of the industries will increase, and the tax burden of the accommodation and catering, food and tobacco, and textile industries will increase significantly. The increase in the actual tax burden in the process of tax reduction is mainly due to the fact that parallel tax reduction may greatly reduce the input tax in some industries, while the reduction in output tax is not obvious, so that the deductible tax is reduced and the actual tax burden is significantly increased. Take accommodation and catering as an example, the combined tax reduction plan did not reduce the output tax rate, still maintaining 6%, but the input tax rate was reduced, resulting in an increase in the real tax burden of the industry.

![image.png]()

![image.png]()

2. the calculation results using the data of listed companies.

Based on the calculation of the annual report data of listed companies in 2017, the parallel tax reduction plan significantly reduces the tax burden of the real estate industry. the next industries with obvious effects of tax reduction are building decoration (construction), transportation (transportation, warehousing and postal services), public utilities (electricity, heat, gas and water production and supply), agriculture, forestry, animal husbandry and fishing (agriculture, forestry, animal husbandry, fishery). This is basically consistent with the measured results of the input-output table above. On the contrary, food and beverage, leisure services, banking and non-bank finance and other industries in this plan is to increase the tax burden.

![image.png]()

The profit thickening effect of architectural decoration (construction industry) is obviously ahead of other industries, followed by real estate, communications, transportation, commercial trade and other industries. In the application level industry classification, the profits of about 1A4 industries are damaged in the process of tax reduction, among which the profits of leisure services and food and beverage industries have dropped more.

Compared with the general tax rate reduction plan, the impact of the parallel tax reduction plan on industry profits is more obvious, but there is also a significant increase in the number of industries with negative effects. As can be seen from the chart below, under the parallel tax reduction plan, there is a very significant positive correlation between the increase in industry profits and the actual tax burden reduction, and a negative correlation with profit margins. Under the parallel tax reduction scheme, the range of tax reduction is larger, and the industry differences are also large, so the parallel tax reduction scheme can more obviously affect the change of industry profits.

![image.png]()

Fifth, who can benefit more from the wave of tax cuts?

The general tax rate reduction plan is relatively mild, and the intensity of tax reduction is relatively strong. According to estimates, the tax rate will be reduced by one tax point, the whole market is expected to reduce taxes by 645.6 billion, and all listed companies are expected to reduce taxes by 157.5 billion yuan. Under the parallel tax reduction plan, the whole market is expected to reduce taxes by 1.2498 trillion, and all listed companies are expected to reduce taxes by 265.2 billion yuan.

There are differences in industry benefits under the value-added tax reduction, and the industry benefit differentiation is even greater in the parallel tax reduction plan.According to the data of listed companies, the tax burden of real estate, banking, non-bank finance and other industries has dropped significantly, while the tax burden of some manufacturing industries, such as iron and steel and non-ferrous metals, has decreased slightly; after the tax reduction, the profits of commercial trade, communications and other industries have increased significantly, while the profits of food and beverage, banking and other industries have increased relatively small. After the combined tax reduction, the tax burden of real estate, architectural decoration and other industries has dropped more, and their profits have increased significantly, while the actual tax burden of food and beverage, leisure services and other industries has increased significantly, and their profits have suffered more.

The benefits of the parallel tax reduction scheme are quite different for companies with different attributes. The tax rate is generally reduced by one tax point, and the tax burden of all kinds of enterprises decreases more evenly, in which the actual tax burden of public enterprises decreases the most, while that of foreign-funded enterprises decreases least; while under the parallel tax reduction plan, the tax burden of central enterprises leads the market, and the tax burden of public enterprises decreases the least. From the point of view of the thickening of profits, the tax rate is generally reduced by one tax point, and there is little difference in the profits of all kinds of companies (other enterprises are not considered here, the sample size is small). Under the parallel tax reduction plan, the profits of central enterprises and local state-owned enterprises have increased relatively much. The increase in the profits of public enterprises is not obvious.

The fact that the benefits of different categories of companies in the parallel tax reduction plan are so different is mainly due to the differences in the distribution of various companies. We select the listed companies in the five categories of industries with the most obvious tax burden reduction in the parallel tax reduction plan for comparison, and the proportion of central enterprises in these five industries is basically very high. Compared with the revenue share of all kinds of companies in the industry, the revenue share of central enterprises exceeds the average in the four major industries of architectural decoration, transportation, public utilities and communications. The central enterprises account for a relatively high proportion in the industries with obvious tax burden reduction, so the effect of tax reduction is more obvious.

Risk reminder event: policy change