Source: Wall Street

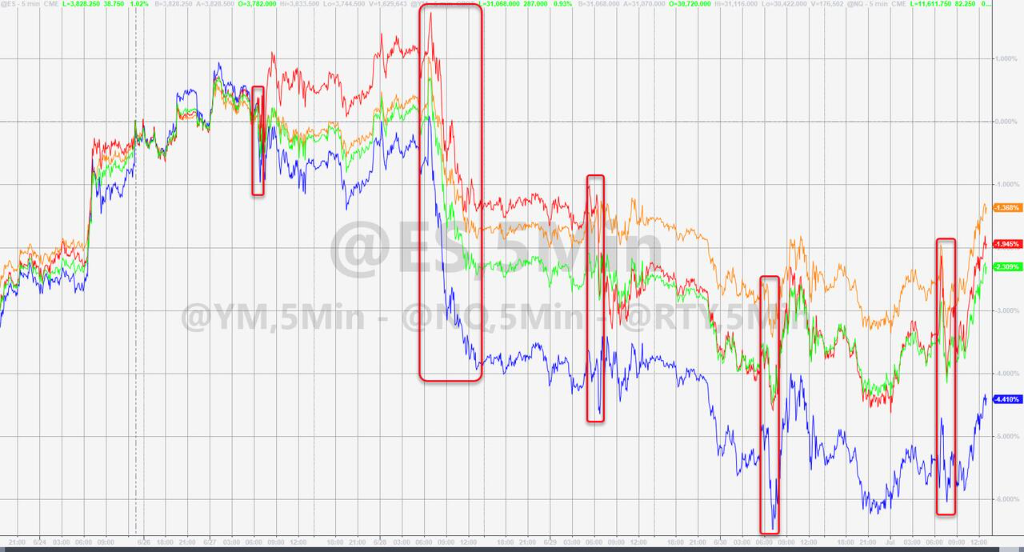

The S & P ended four consecutive declines, with the utilities sector leading the way, with the chip stock index down nearly 4 per cent. Some of the index outperformed the market, with Pinduoduo up nearly 5 per cent and station B up more than 4 per cent.

The pan-European stock index fell slightly to an one-week low, with Uniper up 10 per cent to support the utility sector up more than 3 per cent, while the technology sector fell nearly 2 per cent and fell nearly 5 per cent throughout the week.

The dollar index continued to hit its highest level since the Federal Reserve raised interest rates in June, approaching its highest level in more than 19 years, while the rouble fell 6% to a 10-day low. The yield on 10-year Treasuries hit an one-month low, falling more than 20 basis points at one point, while the yield on two-year German bonds fell 30 basis points this week, the biggest drop in history.

Us oil rose more than 3 per cent, ending a two-week decline, while European natural gas rose more than 10 per cent a week. Gold hit a new five-month low in five months, and silver hit a two-year low in three days, falling nearly 7% in a week. Lun copper hit a 17-month low on Wednesday, while zinc fell more than 4% to a seven-month low and fell more than 9% throughout the week.

After consumer spending fell for the first time this year on Thursday, the US ISM manufacturing index released on Friday fell more than expected in June to a two-year low, adding to fears that an aggressive Fed rate hike could trigger a recession. BofA strategists believe that US stock traders should embrace the "recession shock"; Goldman Sachs Group strategists believe that the risk of a future sell-off in US stocks is still high because pricing only reflects investors' expectations of a mild recession.

After the release of the ISM data, the low opening of the three major US stock indexes refreshed their daily lows, with the Nasdaq down nearly 1 per cent, the Dow down nearly 300 points, and the S & P 500 down about 0.9 per cent. After Micron Technology Inc issued revenue guidance for the fourth quarter that fell far below expectations and warned of a weak demand environment, some technology stocks, especially chips, led the decline in early trading. Lam Research Corp and Micron Technology Inc led the Nasdaq 100th index lower in early trading. At one point, the Philadelphia semiconductor index fell nearly 5 per cent. At midday, various sectors rebounded, with defensive sector utilities taking the lead in promoting the three major stock indexes to rise. S & P, which suffered its biggest first-half decline in 1970 on Thursday, finally reversed its four-day losing streak, but has not been able to break out of the bear market, and other stock indexes have not changed their cumulative losses throughout the week.

Risk aversion intensified after the ISM data, with the dollar index rising more than 0.9 per cent for the first time in two weeks, almost erasing all losses since the Fed raised interest rates by 75 basis points on June 15 and approaching the highest level since late 2002 set on June 15. After Russian gas giant Gazprom decided not to pay a dividend for the first time since 1998, the ruble, which recorded its highest monthly gain against the dollar in June, fell sharply to a 10-day low, falling for the first time in the last five weeks.

Year-on-year CPI growth in the eurozone hit an all-time high in June, with money market traders speculating that inflation could start to slow, predicting for the first time since the beginning of June that the ECB would raise interest rates by less than 75 basis points by the end of September, no longer confident of a 50 basis point hike. Market expectations of aggressive interest rate hikes by the central bank faded further after the release of US ISM data. The price of European and American government bonds accelerated and the drop in intraday yields widened sharply. The yield on the benchmark 10-year Treasury note fell below 2.80 per cent for the first time since late May, with an intraday drop of more than 20 basis points. At one point, the yield on 10-year German bunds fell more than 20 basis points from its intraday high. The yield on the more interest-sensitive 2-year German bond even recorded the biggest weekly drop in history.

Among commodities, international crude oil futures, which have been falling for days, rose intraday, and US stocks rose more than 3% in intraday trading. This week, the momentum of continuous weekly decline was reversed. On Thursday, the OPEC+ meeting agreed to increase production by 648000 barrels per day in August as expected, but media surveys show that despite the Biden administration's urge to increase production, OPEC oil production fell for the second month in a row in June. Due to fears of a recession, most of London's base metals, which fell by at least 20% in the second quarter, continued to fall. Len Zinc, which led the decline for days, fell to a seven-month low, down more than 9% in a week, and Ren Copper repeatedly refreshed its lowest level since February last year. Under the pressure of a stronger dollar, New York gold futures fell below the $1800 mark in intraday trading. Although they narrowed most of the losses in the day at the close, they continued to refresh their lows since early February, and silver futures hit a new low since July 2020.

The S & P ended four consecutive declines in the utility sector leading a rise in the chip stock index. Mining stocks continued to lead the decline in European technology stocks against the market.

The three major US stock indexes collectively opened lower, rising in the short term in early trading, and all refreshed their daily lows after the ISM data were released. The Dow Jones Industrial average fell nearly 290 points, or more than 0.9%, the S & P 500 fell nearly 0.9%, and the NASDAQ Composite Index fell nearly 1%. In midday trading, the Dow, the S & P and the Nasdaq rose one after another. When the session was high in late trading, the Dow rose more than 360 points, or nearly 1.2%, while the S & P and the Nasdaq rose nearly 1.2% and more than 0.9%, respectively.

In the end, the three major indexes collectively closed higher. The S & P 500, which led the rally, closed up 1.06% at 3825.33, wiping out all closing losses that hit a record low since Wednesday on Thursday and remain in a bear market range for four consecutive days. The Dow closed up 321.83 points, or 1.05%, at 31097.26, erasing all losses that closed at an one-week low on Thursday. The Nasdaq, which closed Thursday at its lowest level since June 17, closed up 0.9% at 11127.84, a four-day losing streak for the S & P.

Russell 2000, a small-cap stock index dominated by value stocks, closed up 1.16%, outperforming the market and falling for three days in a row. The Nasdaq 100 index, which is dominated by technology stocks, closed up 0.71%. Although it rebounded, it outperformed the market, with chip stocks leading the decline among component stocks.

As in June and the second quarter, major U. S. stock indexes have fallen this week, giving up some of last week's big gains. The Nasdaq and Nasdaq fell 4.13% and 4.3% respectively last week, and the S & P, which rose more than 6% last week, fell 2.21%, the 11th week in the last 13 weeks. the Dow, which rose more than 5% last week, fell 1.28% in the 12th week of the last 14 weeks, while Russell 2000, which rose 6% last week, fell 2.15% and fell in the ninth week in the last 11 weeks.

Dow, S & P, Nasdaq, Russell 2000 since Friday, June 24

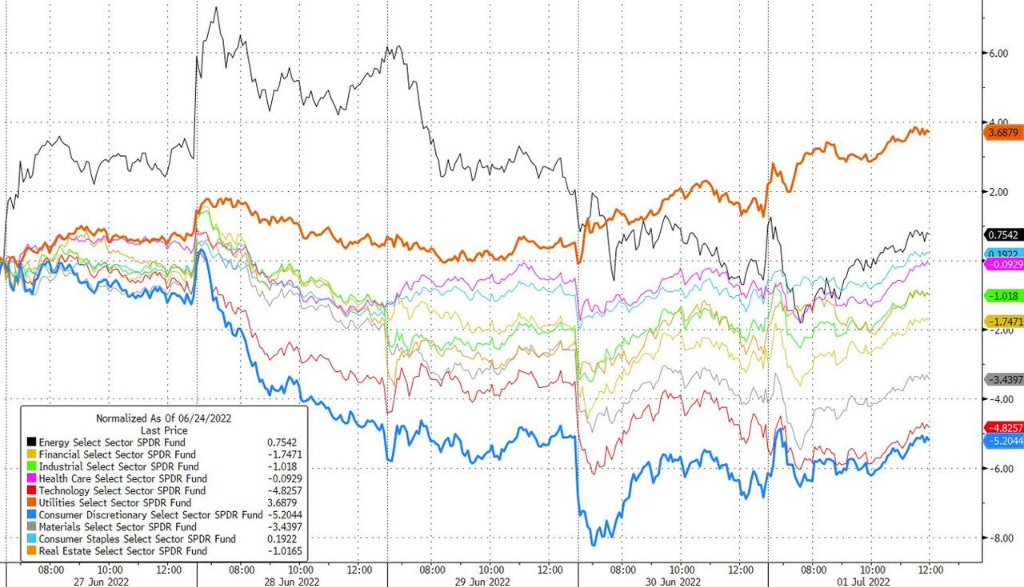

The major sectors of the S & P 500 collectively closed higher, with public utilities up nearly 2.5 per cent for the second day in a row. Amazon.Com Inc's non-essential consumer goods rose nearly 2 per cent, real estate, finance, health care, energy and essential consumer goods all rose more than 1 per cent, while IT, the sector of chip stocks that rose 0.25 per cent, rose the smallest. Only four sectors have accumulated this week, with public utilities rising more than 4%, energy up more than 1%, health care and essential consumer goods up nearly 0.4% and 0.3% respectively. IT, communications services and consumer discretionary goods all fell more than 4 per cent, showing the decline of technology stocks, while the materials sector affected by the metal slump fell more than 3 per cent.

ETF trend of various sectors of US stocks in recent 5 days

Most leading technology stocks rebounded, with Tesla, Inc. closing up more than 1.2 per cent. Among the six major technology stocks in FAANMG, Amazon.Com Inc closed up nearly 3.2% and walked out of the trough since June 16. Netflix Inc, who hit a new low since June 21 on Thursday, closed up 2.9%, Apple Inc rose more than 1.6%, breaking away from the low since June 22, Microsoft Corp rose nearly 1.1%, while Facebook Inc's parent company Meta closed down nearly 0.8% to its lowest level since June 23 and last Thursday. The media said that the division would scale back the planned recruitment of engineers and prepare for a possible decline in performance. The Alphabet of Alphabet Inc-CL C's parent company fell 0.2%, hitting a new low since June 17. These technology stocks have all fallen this week, led by Alphabet down more than 7.8%, Tesla, Inc. down 7.5%, Magi Meta and Amazon.Com Inc down nearly 6%, Netflix Inc down 5.7%, Microsoft Corp down 3%, and Apple Inc nearly 2%.

Chip stocks overall continued to fall and outperformed the market, with the Philadelphia semiconductor index and semiconductor industry ETF SOXX closing down 3.8 per cent and 3.5 per cent, respectively. Among the Nasdaq 100 stocks, Lam Research Corp and Ke Lei closed down more than 7%, Micron Technology Inc fell nearly 3%, Applied Materials Inc and ASML US stocks fell more than 5%, Qualcomm Inc and Microcore Technology fell more than 3%, and Intel Corp fell nearly 3%.

Among the volatile stocks, Kohl's (KSS) closed down 19.7% after confirming that it had stopped selling negotiations to Franchise Group, believing that the retail environment had deteriorated significantly since the start of the bidding process, and downgrading its quarterly guidance. FedEx Corp (FDX), whose rating and target price was downgraded by Berenberg due to increased inflationary pressure, closed down 1.2%. South Korea's Amazon.Com Inc Coupang (CPNG), which was upgraded from neutral to overweight by Credit Suisse, closed up nearly 18%.

Most of the hot US stocks rebounded, some outperformed the market, and ETF KWEB and CQQQ closed up nearly 1.3 per cent and 0.6 per cent, respectively. The Nasdaq Golden Dragon China Index (HXC) closed up nearly 1.3 per cent. Of the four stocks on the Nasdaq 100th index, Pinduoduo closed up about 4.9 per cent, JD.com 2.7 per cent, Baidu, Inc. nearly 1.9 per cent and NetEase, Inc more than 0.1 per cent. The new power of car-building fell, XPeng Inc. fell by more than 4%, NIO Inc. Motor and Li Auto Inc. fell by more than 1%. Among the other stocks, Bilibili, Tencent Music, iQIYI, Weibo Corp and KANZHUN LIMITED rose more than 4%, Zhihu Inc. nearly 4%, the first e-cigarette stock RLX Technology Inc. rose more than 2%, BABA rose about 2%, Trip.com rose more than 1%, while TAL Education Group and Full Truck Alliance Co. Ltd. fell more than 1%. New Oriental Education & Technology fell more than 0.7%, Tencent fell more than 0.2%.

In terms of European stocks, the pan-European stock index Euro Stoxx 600 closed slightly lower for two consecutive days since last Thursday, while most major European stock indexes rebounded, only slightly falling British stocks fell for three days in a row. Seven sectors of the Stoxx 600 closed down on Friday, and the underlying resources of mining stocks, which led the decline on Thursday and June, fell nearly 2.5%, continuing to lead the decline, with technology down nearly 2%. After turning to the German government for help because of Russia's limited gas supply, Uniper, a German energy giant and utility that fell more than 14 per cent on Thursday, closed up 10.3 per cent, supporting a rise of more than 3 per cent in the utilities sector. European chip stocks fell as much as their US counterparts, with Dutch-listed lithography giant ASML down 5.4 per cent and Germany's Infineon down nearly 3.5 per cent.

The Stoxx 600 fell more than 1% this week, giving up about half of last week's increase. Stock indexes in all countries are falling. Throughout the week, only telecommunications rose nearly 0.6%, public utilities rose nearly 0.4%, health care and food rose nearly 0.3%, and insurance rose 0.2%. Real estate, which fell by more than 5%, led the decline, and technology, which rose by more than 5% last week, fell nearly 5%. Basic resources, which fell by nearly 5% last week, led the decline by 4.5%.

In addition, Russia's benchmark stock index, the MOEX, which fell more than 7 per cent on Thursday and fell for the third day in a row, closed up 0.08 per cent and fell more than 7.7 per cent this week, ending two weeks of gains. Gazprom, which announced no dividend on Thursday, tumbled more than 30% on the day and closed down another 7% on Friday.

The 10-year Treasury yield hit an one-month low in intraday trading, falling more than 20 basis points at one point and the biggest weekly drop in 2-year German bond yields in history.

European government bond prices rose for three days in a row, and yields fell by at least 10 basis points in a row. By late European trading, the yield on UK 10-year benchmark government bonds fell 14.3 basis points to 2.086%. The intraday low of 2.011% was the lowest since May 31, down more than 27 basis points from the intraday high. The yield on 10-year German bunds was 1.232%, down 10.4 basis points on the day. U.S. stocks broke 1.17% to 1.164% in early trading, the lowest since June 1 and down more than 24 basis points from intraday highs. The yield on interest-sensitive 2-year German bonds was 0.516%, down 13.3 basis points on the day.

The yield on 10-year gilts fell 21.6 basis points this week, while the yield on 10-year German bonds fell 21.0 basis points, both falling for two consecutive weeks and by at least 20 basis points, while the yield on two-year German bonds fell 29.7 basis points this week, the biggest weekly drop in history.

The trend of bond yields of euro zone countries since March 2020

The yield on the benchmark US 10-year Treasury note stood above 3.02% in early trading in the Asian market, and then continued to fall. The Asian market lost 3.00% in intraday trading, and US stocks fell below 2.90% before trading. After the release of ISM data in early trading, US stocks once broke 2.80% to 2.7873%, breaking 2.80% for the first time since May 31, giving up all the increases since the announcement of CPI on June 10, with an intraday drop of more than 22 basis points. At the end of trading in New York, it was 2.8803%, down 13.26 basis points on the day, and down about 25 basis points this week for two consecutive weeks.

The trend of 10-year Treasury yields since April

The dollar index continues to hit a new high since the Fed raised interest rates, approaching a more than 19-year high, the rouble fell 6% to a 10-day low.

After Thursday's intraday decline ended two consecutive gains, the ICE dollar index (DXY), which tracks the exchange rate of a basket of six major currencies of the dollar, maintained its upward trend throughout the day on Friday. European stocks accelerated to rise again by 105.00 in intraday trading. After the release of ISM data in the United States, they once broke through 105.60 to reach a new high since June 15. It was close to the intraday high of 105.80 since December 2002, and rose nearly 0.91% on the day. It was the biggest intraday gain since June 17.

By Friday's close, the dollar index was above 105.10, up 0.4% on the day and nearly 1% this week. The Bloomberg dollar spot index rose more than 0.3%, its highest since June 14, and rose nearly 0.9% this week. All easily erased all the losses that bid farewell to three weeks of gains last week.

Bloomberg Dollar spot Index since June 10

The offshore RMB (CNH), which said goodbye to three consecutive days of decline against the dollar on Thursday, fell back to 6.7271 against the dollar before European stocks traded. It fell below the 6.72 mark for the first time since June 22, falling 334 points from the intraday high of early trading in Asia, and then gradually narrowing the decline. U.S. stocks recovered 6.70 in midday trading. At 04:59 Beijing time on July 2, the offshore RMB was at 6.6974 yuan against the dollar, down 33 points from late Thursday in New York. It is down 158 points this week, ending two weeks of gains.

The Russian rouble, which rebounded on Thursday, closed at 54.5 against the dollar, down 5.93% on the day, falling below 55.80 in intraday trading and nearly 8.5% on the day, the lowest in the last 10 trading days since June 21, far away from the May 2015 high set on Wednesday near 50.00. After rising more than 16% in June to record its biggest monthly gain, the rouble fell 2.06% this week, falling for the first time in five weeks and falling in the second week of the last 11 weeks.

Bitcoin (BTC) rose in early trading in Asia, once approaching $21000 to refresh its recent three-day high, far from the June 19 low set by falling below $18600 on Thursday, up more than $2000, or nearly 12%, from the intraday low, and then giving up most of its gains. Asian stocks fell below $20, 000 in intraday trading, European stocks approached the $19000 mark, and US stocks closed around $19500. It has risen by more than 3% in the last 24 hours and has fallen by nearly 9% in the last seven days.

Us oil got rid of its one-week trough and rose more than 3% in intraday trading. European natural gas rose more than 10% in a week after two weeks of decline.

International crude oil futures, which have fallen for two days in a row, rose in midday trading on Friday. When European stocks were at a pre-session low, US WTI crude fell to $104.56, down more than 1.1 per cent on the day, while Brent crude approached $108and fell more than 0.9 per cent. European stocks rose after early trading. When US stocks were at their intraday high, US oil rose to $109.34, up nearly 3.4 per cent on the day, and cloth oil rose above $112and rose more than 3.1 per cent on the day.

In the end, WTI August crude oil futures closed 2.52 per cent higher at $108.43 a barrel, shaking off Thursday's low since Thursday, while Brent September crude oil futures closed 2.38 per cent higher at $111.63 a barrel, erasing most of Thursday's 3 per cent decline.

Us oil rose 0.8% this week, ending a two-week decline, while last week's zero rise and fall of 2.3% did not return to the decline of the week before last week, nor did it repeat the mistakes of June. Us oil fell 7.8% in June, while cloth oil fell 6.5%. It rose in the last six months, but rose in the second quarter and the first half of the year.

The trend of US WTI crude Oil Futures since June 21

Natural gas in Europe varies from rise to fall. ICE UK natural gas futures closed down 2.96% at 240.94 pence per kcal, ending three days of gains, rising 41.9% this week, erasing last week's nearly 16% decline. TTF benchmark Dutch natural gas futures closed up 2.26% at 147.784 euros per megawatt, rising for three consecutive days and hitting their highest level since March 8, up about 14% this week and for three weeks in a row.

Us gasoline and natural gas futures rebounded after falling for two days in a row. NYMEX August gasoline futures closed up 4.3% at $3.6878 per gallon, still down 2.5% this week for two weeks, while NYMEX August natural gas futures closed up 5.64% at $5.7300 per million British thermal units after falling more than 16% on Thursday and 8.8% this week for three consecutive weeks.

The trend of American Oil and European and American Natural Gas in the past year

Lun copper hit a 17-month low on Wednesday, falling more than 4% to a seven-month low of more than 9% in a week.

London base metal futures mostly fell on Friday. Len Zinc led the decline for the second day in a row, falling more than 4% on Friday after falling 6% on Thursday, closing below $3100 for the first time since October 7 last year, and Len Copper and Lunni both fell for two days in a row. Lun copper fell more than 2% in one day, closing below $8100 for the first time since February 8 last year, and hitting a new low on the third day of the week since February last year. Lenny closed below $22000 for the first time since January 11 this year. Lun Aluminum fell for four consecutive days, hitting its lowest level since July last year for two consecutive days. While Lunxi and Lunxi ended three days of consecutive losses, Lunxi emerged from Thursday's November 2020 trough, and Lunxi got rid of the danger of falling to Friday's lowest level since March last year.

Most of the base metals have fallen this week, led by a drop of more than 9% in zinc and nearly 4% in copper. Lenny fell more than 2% for five weeks in a row. Lomalco fell about 0.5% for six weeks. Lunxi, which fell by more than 21% last week, rose more than 8% in a week, up thousands of dollars from the 15-month low set on Friday, while Lunxi lead rose 1%, ending three weeks of decline.

Gold hit a five-month low and silver hit a two-year low in three days, down nearly 7% in a week.

New York gold futures fell below $1800 in Asian trading on Friday. U.S. stocks fell to $1783.4 before trading, the lowest since January 23, and fell more than 1.3% during the day. U.S. stocks continued to rise after opening, and U.S. stocks rose after rising to $1800 at the end of morning trading. finally, COMEX August gold futures closed down 0.3% at $1801.5 / oz, closing down for five consecutive days. And for two consecutive days, the main contract closed at a new low since February and March.

New York silver futures fell for four consecutive days, while COMEX September silver futures closed down 3.4% at $19.667 an ounce, the third consecutive low since July 2020. Gold futures are down 1.6% this week, and silver futures, which are down 6.9%, have fallen for three weeks in a row.

Trend of New York Gold Futures since June 21

Edit / new