China's major internet companies are stepping up “core manufacturing.”

At the recent Alibaba Cloud summit, Alibaba Cloud Intelligence President Zhang Jianfeng announced CIPU, a dedicated processor designed for new cloud data centers, and stated that in the future, CIPU will replace CPUs as the processing core of the cloud era.

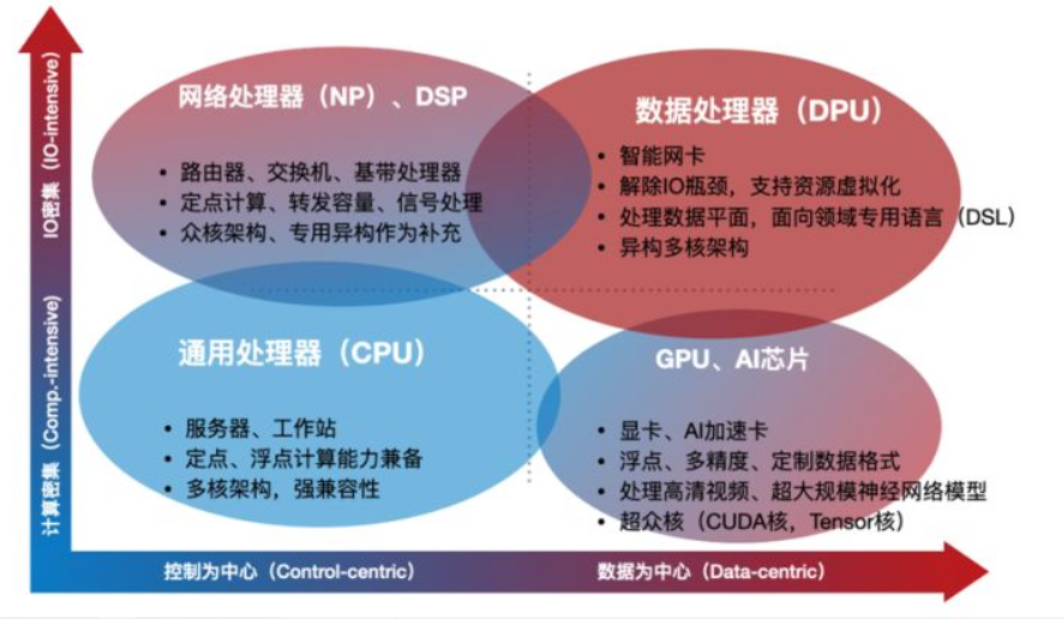

It was also revealed that Tencent recently invested hundreds of millions of yuan in the DPU startup Yunbao Intelligence in a new round of financing. This is also the third time that Tencent has invested in this DPU company that has been established less than two years ago. DPU is considered the “third main chip” for data centers after CPUs and GPUs, and is a hot investment area in the chip industry in recent years.

Meanwhile, in November of last year, Tencent officially revealed its actions in self-developed chips for the first time, launching the “Zixiao” chip for AI computing, the “Changhai” chip for video processing, and the “Genling” chip for high-performance networks. All three chips are dedicated chips.

When it comes to naming the chip, the employees of the big factory have fully demonstrated their solid experience in reading fantasy novels on the Internet.

The success of the chip did not happen overnight. 2018 was a key moment — Baidu announced the launch of Baidu Kunlun 1, a full-function AI chip in the cloud. In September of the same year, Ali announced that its DAMO Academy and Zhongtianwei had formed a chip company, named “Pingtouge Semiconductor.”

In recent years, due to tight global supply chains, the semiconductor industry has come into the spotlight, and is often criticized for focusing only on business model innovation, and internet giants that lack hard technology have “rolled up their sleeves” and taken the initiative to enter the field of chips, an absolute “hard technology” field; what kind of relationship does the chip BAT is making have with well-known Intel, Qualcomm, and AMD?

01 A lot of “core things”

To a large extent, the wind of the core building movement came from the US.

Amazon launched the network chip Nitro1 in 2013, and now it has three complete lines: a cloud network chip represented by Nitro, a server chip represented by Graviton, and a dedicated AI machine learning chip.

Google, on the other hand, first introduced a TPU chip, or “tensor processor,” at the I/O developers' conference in June 2015. It was created specifically to optimize its TensorFlow framework, and has now reached the fourth generation of products.

By sorting through the chips released by these Chinese and American internet giants, it is easy to see that the chips created by the major manufacturers are mainly dedicated chips, and are relatively focused on AI chips and cloud server chips, which are not CPUs and GPUs that many people are familiar with.

The so-called special chip is actually easy to understand. It is a chip specially designed to solve a relatively specific problem. In contrast, it is a general chip represented by a CPU. The latter can do many things, but it sacrifices efficiency in certain scenarios.

Because in various scenarios such as artificial intelligence computing and data center processing, the amount of computation is required and the calculation is relatively “regular,” it is worth specifically designing hardware resources for them to achieve the purpose of reducing power consumption and improving computational efficiency.

Expanding a little further, the different forms of FPGAs and ASICs are also extended to AI-specific chips. The former retains a certain degree of flexibility that can be modified, while the latter is thoroughly customized for specific scenarios.

For example, the optical 800 chip introduced by Ali in 2019 is a chip dedicated to AI inference. Its inference performance is more than 100% more cost-effective compared to traditional GPUs.

For example, Baidu also abandoned the GPU route and built on FPGAs from the beginning. FPGAs are characterized by being programmable, so users using Kunlun chips can customize, modify, and secondary develop according to their own application scenarios. Because AI application scenarios are scattered and complex, FPGAs are programmable chips, suitable for deployment in cloud computing platforms that provide virtualized services.

The primary purpose of the core manufacturers is to meet the needs related to their cloud computing and AI business. For example, Amazon's own Nitro never sells to the outside world; it is completely self-developed and used.

So why don't big manufacturers cooperate with chip design companies like Qualcomm and AMD, but instead choose to develop their own chips or make chips through mergers, acquisitions, and investments in startups?

When it comes to core making decisions to climb to the top of the human technology tree, the big manufacturers are all very rational, and the reason they don't cooperate with chip design companies is also very simple: it's not economical, it's not safe.

With the continuous development of intelligent technology and the gradual enrichment of application scenarios, the characteristics of chips are that they are becoming more and more specialized, and there is an increasing need for customized adaptations to specific scenarios. According to Late Post, DPU is still in a very early stage, and the industry is still “crossing the river by touch” in terms of technical routes and product forms.

According to comprehensive data, the R&D cost of a dedicated chip is at least hundreds of millions of yuan, including various aspects such as personnel expenses, EDA authorization, IP authorization, streaming expenses, product trial production, etc., but for “big business” companies, money is not the most important factor to consider; time costs and the accumulation of commercial barriers are even more important — compared to being controlled by Qualcomm and Nvidia, it is obviously more cost-effective to do it yourself on a dedicated chip.

In reality, this is even more true for Chinese companies that take more dimensions into geopolitical gaming. Of course, nothing is absolute. Google also cooperated with Broadcom in the process of developing TPU, but it's just that when it comes to core manufacturers, they place more importance on autonomy and control, and can be deeply customized for their own business scenarios.

02 The “trend” of core building

You may have discovered that the companies most active in core building in China and the US use cloud computing as one of their main application scenarios, and even Microsoft, which has not been highlighted by us, reports that it has been developing its own ARM architecture processors for the past two years. There is already a rift in the Wintel Alliance. Huawei, which is also vigorously developing cloud computing, also has products such as the “Kunpeng 920,” a server chip based on the ARM architecture.

According to Micronetwork, Elvis Hsu, general manager of CINNO Research's semiconductor division, said, “Self-developed customized AI chips make cloud servers perform significantly higher than servers that use general-purpose chips such as CPUs and GPUs, so independently developing ASIC or FPGA chips is the best solution, such as Ali's Ali-NPU neural network chip.”

This is not only to meet the performance requirements of the scenario, but also to directly reduce costs. If self-developed Arm server chips are used, the price is only a fraction, or even one-tenth, of x86 chips. This will give vendors a competitive advantage in an increasingly competitive environment in the cloud service market. The reason Amazon AWS is able to become a “price butcher” is also largely due to self-developed chips that effectively reduce service costs, yet can be cheaper on the premise that instance performance is not inferior to competitors. Especially in this day and age, when state-owned cloud computing collectively enters the market and seizes orders, how to hold on to the barriers is testing Tencent Cloud and Alibaba Cloud.

On the technical level, as mentioned before, the big manufacturers are not “rebuilding the wheel,” but are trying to expand their territory in the field of high-end specialty chips such as AI chips and server chips. This will also drive the advancement of domestic chip design capabilities. For example, the Yitian 710 chip released by Ali last year uses a 5nm process and ARMv9 architecture, and Baidu Kunlun Core 2 also uses a more advanced 7nm process.

However, at the level of the commercial ecosystem, strong and strong manufacturers are not inferior to the original players in the chip industry in terms of talent recruitment or other resource integration capabilities, and since they are used for strategic businesses such as AI and cloud computing, there is no need to worry about the appearance of a terrible situation where they hit a wave of money like the consumer business, then retreat after a bad situation, eventually leaving behind a scourge of the ground.

The chip industry relies heavily on division of labor and cooperation. The entry of big manufacturers as new players is also mainly in the chip design process. Therefore, big manufacturers organize their own research, which will bring benefits to chip manufacturers, chip equipment, and chip design companies that cooperate with them, and the rich application scenarios owned by Internet companies can also facilitate the completion of a closed commercial loop of chips put into production faster.

For example, Baidu's “Hongmei” chip for smart homes and other fields, Tencent's “Changhai” special chip for video processing, and Ali's RFID chip “Fallen” all reflect the scenario advantages of Chinese Internet companies.

In fact, scenarios that force hardware have always been the rule of industrial development, especially for the game industry and consumer electronics. The rise of chips requires a trend: just as Intel and AMD started with the wave of the PC industry; NVIDIA started with the pressure of gaming demand and took advantage of large-scale parallel computing needs and the AI wave; ARM took off at the same time as the smart phone industry. The “trend” of the core building movement of China's Internet giants is the wave of cloud computing and industrial digitalization.

In addition to Tencent and Ali, major Internet companies such as Byte and Meituan are also actively laying out chip tracks through investment and building their own teams. For example, in 2021, ByteDance participated in companies such as Heem Computing, Cloud Connect, and Ruistech, and invested in GPU chip design company Moore Thread through its wholly-owned subsidiary Quantum Dynamic. It also posted many positions related to chip development on recruitment platforms, targeting server chips and AI chips; Meituan also invested intensively in many semiconductor startups such as AiXI, Rongxin, and Hesai Technology in 2021 through affiliated companies.

Baidu, on the other hand, has an independent portal for the chip business. Baidu Kunlun completed independent financing a year ago. At the time, the valuation was around 13 billion dollars. Compared to this, JD Cloud's core development progress is relatively unclear. JD Cloud released the unified storage platform “Yunhai” in April, saying it is based on a self-developed “King Kong” chip, but other than the name it made in the press release, no further information has been disclosed yet. However, business information shows that in 2021, Liu Qiangdong invested in Schim Computing through Jiangsu Jingdong Bangneng Investment Management Co., Ltd., with a shareholding ratio of 2.87%.

As the chip industry becomes popular, some chip headhunters told Zhou Tian Finance that now the talent level is already in short supply, and many manufacturers will go to colleges and universities to target talents ahead of time. Even during this difficult employment season, “college students who have just graduated get their master's salary starting at 50-800,000.” I'm afraid the entry of big manufacturers will only accelerate talent pay, or dig into the technical backbone of the original middle and downstream manufacturers. After all, big manufacturers are more resistant to losses during the investment stage of new businesses.

On the other hand, at present, production capacity for advanced manufacturing processes is still mainly concentrated in the hands of manufacturers such as TSMC and Samsung. The chip industry's stuck neck problem is concentrated in the manufacturing process, and there is still no relief. It remains to be seen how much production capacity the high-profile chips released by major Internet companies can grab and how quickly mass production can be achieved. At this stage, it's more like “do one point, say three points,” focusing on releasing signals.

Overall, however, it is inevitable that there will be a short-term build-up in market competition. What's more, in a capital-intensive and intellectual-intensive cutting-edge industry like semiconductors, you might as well leave more time for big manufacturers to observe the core issues.

Summarize

Frankly speaking, today, it is increasingly unnecessary to use “Internet companies” to define the scope of an enterprise's business. Whether it's big manufacturers or new car builders, they all use products and services as carriers to meet user needs, and technology research and development as a means to achieve goals.

Just as the US industry does not refer to Meta, Google, and Amazon as Internet companies, but uniformly classifies them into the Tech Company category, when it comes to core manufacturing, we feel that major Chinese manufacturers are still keen on the latest industry trends and are patient to invest.

Domestic chips have now reached a critical window period: this window has the following characteristics: the market can accommodate giant players; on the eve of an explosion, large-scale applications have not yet arrived; scenarios are scattered, complex, and require customization; individual chips are far from enough and must be supported by supporting solutions.

From the perspective of the chip industry, the first-mover advantage and Matthew effect of this industry are very obvious. The market concentration in various professional segments is very high, and existing giants are also very good at “breaking down ladders” and “making stumbling blocks,” relying on technology monopolies to earn excess profits. For Chinese technology companies, only by paying close attention to the valuable window period of the chip industry and using special chips such as AI and servers as an entry point can they increase more bottom cards in a complex economic situation.

This article is from the WeChat account “Techfinsight” (ID: techfinsight), author: Zhou Tian Finance