Source: Wall Street

Author: Wang Mei

HSBC expects Herm è s, Gucci and LVMH to have profit margins of 37.5 per cent, 36.8 per cent and 28.0 per cent respectively in the first half of 2022.

Even with the shadow of the COVID-19 epidemic and the conflict between Russia and Ukraine, global luxury groups are still raving in cash.

On April 12, the LVMH Group released its first-quarter results of this year, which showed that revenue in the first quarter of 2022 was 18 billion euros, an increase of 29% over the same period last year. Two days later, Herm è s released its first-quarter results also showed that revenue in the first quarter was 2.77 billion euros, an increase of 33% over the same period last year. The two luxury giants have an average daily income of 1.382 billion yuan and 213 million yuan, respectively, and both say sales in almost all their departments have achieved double-digit growth.

And a report released by HSBC on Monday predictedAlthough investors seem to expect the luxury industry cycle to enter its final orgy, luxury sales in the second quarter of 2022 will surprise everyone.

The performance of Europe and Japan will be the brightest.

The bank said that from a subregional point of view, in the second quarter, in view of the reopening of the European region and the rebound in cross-regional travelEurope should have the most impressive year-on-year sales growth.Luxury store buying teams in Milan, Paris and London have also recently been supported by Middle Eastern consumers and US tourists who have benefited from a strong dollar.

Japan is not inferior.Because buying activity in Japan seems to have increased significantly since the sixth wave of the COVID-19 epidemic peaked in mid-February.in AmericaBased on the high base effect in the first quarter, HSBC expects US luxury sales to slow month-on-month in the second quarter of 2022, which may be slower in May and June than in April, but on a three-year basisThere will be no real deceleration.

Affected by the epidemic in the past two years, the global luxury consumer market has been in the doldrums, but the Chinese market has bucked the trend, and restrictions on overseas travel have led to the return of luxury consumption. Personal luxury goods sales in China rose 36 per cent year-on-year to 471 billion yuan in 2021, more than double the 234 billion yuan sales in 2019 before the outbreak, according to data released by Bain Consulting.

In the first quarter of this year, due to the epidemic and other reasons,After two consecutive years of rapid growth, the growth of domestic luxury consumption has slowed down.HSBC predicts that revenue from most luxury brands in the Chinese market will fall 25% in the second quarter from a year earlier.

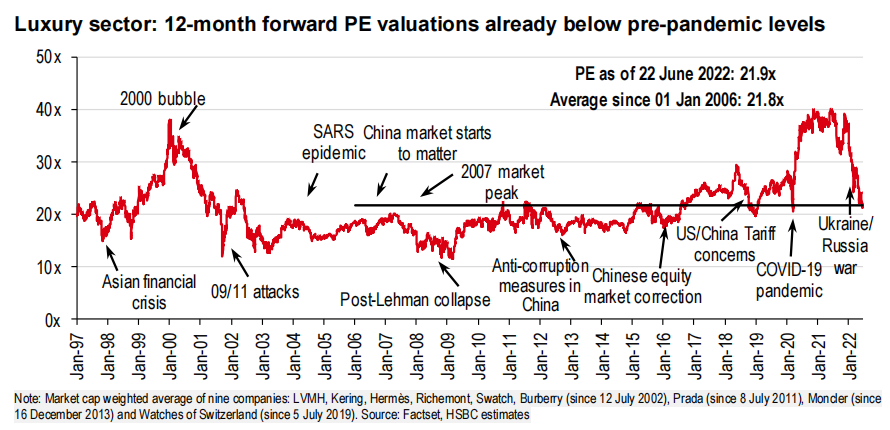

Meanwhile,The HSBC valuation model shows that PE valuations in the luxury industry in the coming year have fallen below pre-epidemic levels, indicating that investors are sceptical about the luxury market in the second half of 2022.

But HSBC believes that, in general,While growth in Europe and Japan is indeed unsustainable (because it is not mainly driven by recruitment), it still says it has a constructive view of the outlook for the Chinese market, as well as for the US market.

Industry profit growth benefits from high-end product lines, higher prices and high operating leverage in Europe

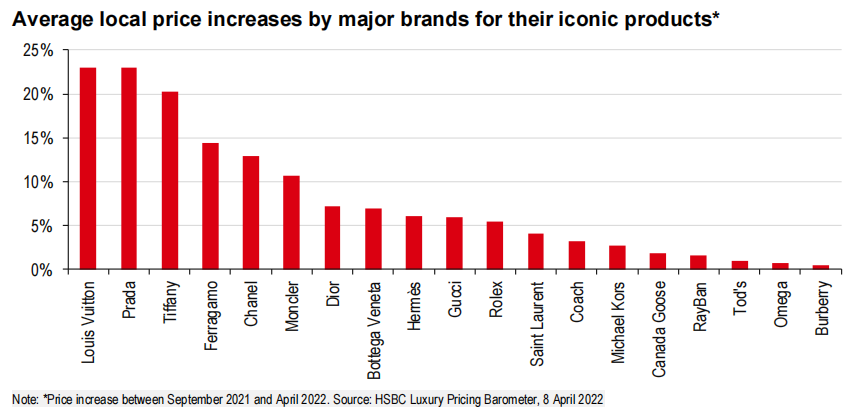

HSBC said that most major brands raised prices sharply in the first quarter of 2022, which should support profit growth in the second quarter (and beyond).

Behind the surge in revenue of luxury goods groups in the first quarter of this year, there is also a "gratifying rise" in commodity prices.At the beginning of the year, major luxury brands ushered in the first wave of price increases.On February 16th, Louis Vuitton, a unit of the LVMH Group, announced that prices of all products, including leather goods, accessories and perfumes, would rise that week in response to rising manufacturing costs and rising global inflation.

According to consumer observation, the price increase of LV is much higher than that of previous years, generally between 10% and 20%. The more popular the package, the higher the price increase. After the news came out at that time, "LV generally increased by 10%" went viral instantly, and many netizens commented that"it's better to buy a fund than to buy a bag."the speed of saving can't keep up with the rate of price increase."。

Meanwhile, Axel Dumas, executive chairman of Herm è s, expects the average global price of Herm è s products to rise by 3.5 per cent this year. It is reported that at the beginning of this year, the price of accessories such as Herm è s scarves increased by 10%. In addition, Chanel, Dior, Balenciaga, Celine and other brands also completed a new round of price increases at the beginning of this year.

However, the price increase does not scare the "rich" at all. After hearing about the price increase, many people want to rush to buy it before the price rise, resulting in LV out of stock. Some people turn luxury goods into financial products with investment attributes and sell them at a premium."the more you go up, the more you buy, the more you buy, the more you buy."。

Analysts believe thatAfter the price increase, the logic behind the increase in sales of luxury goods giants is:First, the rise in the price of luxury goods will only raise the value of the "rich" who want to show their status, status and financial resources. at the same time, the scarcity of luxury goods, especially the limited edition, has a strong anti-inflation attribute, prompting a wave of the middle class to join as a wealth management product; second, luxury giants have monopoly pricing power.

HSBC believes that, coupled with high operating leverage in Europe,These factors will drive the sales of most brands to grow from "median" to "low double digits" in the second quarter of 2022, which should be enough to keep the industry's profit margins flat or even higher than last year.。

In addition, HSBC believes thatWith the help of foreign exchange (weak euro), industry profit margins should be further supported in 2023.In the case of the LVMH group, other things being equal, a 5 per cent depreciation of the euro against all other currencies would cause the group's EBIT to rise by an average of 8 per cent. Since most companies hedge on a 12-month forward basis, the current weakness of the euro should help boost profit margins in the first half of 2023.

Performance Forecast of 9 luxury groups

In its report, HSBC provides an outlook for the performance of nine luxury giants in the first half of this year.

Watches of Switzerland (Swiss Watch)

The group announced sales for the 2022 fiscal year to April on May 18 and provided full-year performance guidance, and its adjusted EBIT (earnings before interest and tax) could fall to between £128 million and £132 million. The group has also issued preliminary guidance for fiscal year 2023, with revenues of between £1.45 billion and £1.5 billion.

HSBC believes that the guidelines will not change much in the short term, but the guidelines do not take into account the benefits of acquisitions, the bank will take into account the £118 million of sales generated by the acquired assets, and the group's EBIT will reach £1.57-169 million in fiscal year 2022.

Due to the current grim macro environment, especially in the United States, where the stock market has plummeted and inflation fears have intensified, investors are worried that sales of high-end watches at auction are beginning to slow, but as the bank's first luxury goods group, there is still some evidence that the supply and demand of Rolex is different from that of other watches.(so is omega) and expects the short-term trend in the US market to remain strong.

Burberry (Burberry)

HSBC expects the group's reported retail sales to be flat in the first quarter of the 2023 fiscal year to June 2022, with the Chinese market down 40 per cent from a year earlier (including a rebound in June) and 20 per cent year-on-year growth elsewhere.

Richemont (Richemont)

HSBC expects the European market to be an absolute bright spot for Richemont, and its retail and jewellery brands will outperform the group's average. Advertising at the end of the last fiscal year should support growth, while the launch of the latest high-end jewellery series by big brand Cartier in Madrid is likely to put a high-profile end to this quarter's sales.

Although Richemont has more market share in China than many of its peers, HSBC believesThe strength of its jewellery brand and the growth of other markets will make the group one of the lucky few to achieve high single-digit sales growth at a fixed exchange rate.

LVMH (LVMH)

HSBC believes that LVMH is the leader and representative of the luxury goods industry and should report strong 1H22 results given its continued growth in market share and strong operating leverage.

The company's 1Q22 sales rose 23 per cent at a fixed exchange rate, while sales in its fashion leather division, its main source of profit, rose 30 per cent. Although the macro environment is full of challengesHSBC expects the group to still achieve nearly 10 per cent sales growth in the second quarter of 2022.

Unlike Kering, where Gucci's market share has declined and needs to be reinvested, and Richemont, which has reinvested in selling advertising, HSBC believes there are few factors that will prevent LVMH from maintaining profit margins in every division, except for the cognac brand Hennessy, where 1H22 sales are likely to fall despite restocking at 2Q22, as well as perfumes and cosmetics divisions with slightly abnormal profit margins in the same period last year.

Considering that LVMH's brand portfolio has been very positive (the fashion leather business has performed well and the selective distribution strategy has recovered from the grim situation)The bank expects its earnings before interest and tax (EBIT) ratio to rise 1.4 per cent to 28.0 per cent in the first half of 2022.

Kering (Kering Cloud Group)

HSBC expects Kering's 2Q22 sales to grow 8.2 per cent month-on-month at a fixed exchange rate (7.3 per cent affected by the exchange rate), with Gucci growing 0.4 per cent and Bottega Veneta 7.5 per cent and Saint Laurent 22 per cent and other brands 21 per cent.

For 1H22 results, HSBC expects the company's EBIT to be 2.68 billion euros, a year-on-year increase of 19% and a year-on-year increase of 27.4%, a year-on-year contraction of 0.4%.Due to the impact of the epidemic and increased marketing investment in the second quarter, Gucci profit margins will fall 1 percentage point year-on-year to 36.8% (still impressive enough).

Moncler (League Corey)

Like other luxury giants, HSBC expects little year-on-year deceleration of Moncler in the US, while growth in Europe is driven by consumers from the Middle East, the US and still strong local demand. In the Asia-Pacific region except China, sales in most markets should grow at double-digit rates.

Its brand Stone Island (Stone Island) should continue its strong growth trajectory. HSBC expects sales of 69 million euros in the second quarter of 2022, an organic growth rate of 20%, and the group's overall organic growth performance of 14%. In terms of profit marginThe bank expects 1H22's EBIT margin to be 17.5%.It is not much different from the 18% of 1H19, which is consistent with management's statement that the profit margin of EBIT in 2022 is close to 2019.

HSBC said in the report that most of Moncler's earnings were biased in the second half, accounting for 80 per cent of the group's reported earnings before interest and tax, so it was less affected in the Chinese market in the second quarter than other luxury goods companies. Given the macro environment of high inflation, investors are worried about the sustainability of demand in Europe and the United States, butHSBC said Moncler had proved over the years that it was a high-quality company supported by strong management execution and that there were still many growth opportunities in the medium term.

Prada (PRADA S.p.A.)

HSBC expects 2Q22 sales to grow 12 per cent at a fixed exchange rate (exchange rate impact is 5 per cent), retail growth of 13 per cent and wholesale flat. By brand, sales of Prada are expected to grow by 12 per cent. Sales of Magi Miumiu (more from Chinese mainland) will grow by 10 per cent, and sales of other brands will grow by 10 per cent.EBIT is expected to reach 300 million euros in the first half of 2022, an increase of 81% over the same period last year, and the profit margin before interest and tax will reach 17.0%., slightly below the level of 17.4% in the second half of 2021.

Herm è s (Herm è s)

HSBC expects the group's 2Q22 organic sales to grow by 9%, and by product, leather goods (46% of group sales in 2021) should return to slightly lower than the 10.5% organic sales growth rate expected in fiscal 2022; expected due to an increase in operating costs (inventory construction, recruitment, marketing expenses, capital expenditure) and the negative impact of foreign exchange hedgingEBIT profit margin in the first half of 2022 was 37.5%, 3.2 percentage points lower than the peak of 40.7% in the first half of 2021.. Management expects foreign exchange hedging to have a negative impact on profit margins by 1.5 percentage points in 2022.

HSBC believes that Herm è s is a company worth holding in such a challenging macro environment if investors are really sceptical about the future of the luxury industry. Because in a tough macro environment, Herm è s is one of the most resilient, if not the most resilient, companies in the industry. In fact,Herm è s tends to perform well in difficult times, thanks to its leather goods division (demand outstrips supply), but also performs well in good times, thanks to the steady performance of all other sectors.

Swatch (Swatch)

While the closure of the Russian market could reduce the group's sales by 150 million Swiss francs in 2022 and a slowdown in the Asia-Pacific market by 200m francs, HSBC believes growth could eventually be flat in June from a year earlier, because distributors sold out before they could reorder in the summer.

HSBC expects the group's 1H22 organic sales to grow by 5%, excluding 0.5% positive foreign exchange impact.1H22's profit margin before interest and tax is expected to grow 13.4 per cent year-on-year, up 1.5 percentage points from the same period last year, thanks in particular to omega's contribution and improved operating expenditure leverage.

Edit / roy