The S & P rose more than 3%, the Dow rose more than 800 points, reversing three weeks of decline; Meta rose more than 7%, the plate rose nearly 4%, Tesla, Inc. rose 13% in a week, the sector rose more than 8% throughout the week, the energy sector fell alone throughout the week; XPeng Inc. rose 7%, BABA rose nearly 5%.

Pan-European stocks posted their biggest gain in six weeks, ending a three-week losing streak, with the technology sector up nearly 4% and the entire week up more than 5%, while the mining sector fell nearly 5% in a week. The yield on 10-year u.s. Treasuries rose back to 3.1%, up more than 10 basis points from Thursday's low and still rising for three weeks. The dollar index ended three weeks of gains.

Us Oil rose more than 3% to shake off a six-week low and still fell for two weeks. European natural gas fell from a three-month high and still rose more than 9% throughout the week. Gold ended four straight falls out of more than a week's lows, but fell for two weeks in a row. Shanghai and tin, which fell more than 9% during the day, fell more than 5% in night trading, while Lunxi fell more than 9% to a 15-month low. New York Copper temporarily dropped its 16-month low and fell nearly 7% throughout the week.

Instead of falling as expected, the number of new home sales in the United States surged 10.7% month-on-month in May, the first monthly increase this year. The final value of consumer confidence at the University of Michigan in June was slightly lower than expected, but the survey showed that an important factor affecting the Fed's decision to raise interest rates this month-consumers' five-year long-term inflation expectations unexpectedly fell, saying goodbye to the 14-year high recorded in May.

Economic data have further cooled market expectations of a Fed rate hike. U. S. stocks accelerated upward after a rebound on Thursday, reversing a three-week decline in a week with only four trading days. The media pointed out that market pricing shows that investors are beginning to rule out the possibility of raising interest rates after December this year, is expected to reach the peak of raising interest rates by the end of this year, and is still considering the possibility of cutting interest rates next year. Asset rebalancing by institutional investors also contributed to this week's rebound in US stocks.

After the announcement of the US CPI, the expectation of the Federal Reserve to cut interest rates plummeted. After the consumer confidence survey of the University of Michigan was released, the expectation of cutting interest rates increased, and the expectation of raising interest rates continued to fall.

After the announcement of the US CPI, the expectation of the Federal Reserve to cut interest rates plummeted. After the consumer confidence survey of the University of Michigan was released, the expectation of cutting interest rates increased, and the expectation of raising interest rates continued to fall.

The three major US stock indexes opened higher on Friday when the Fed revealed that all the big banks had passed their annual stress tests, believing that banks had a strong pool of capital to withstand recession, bank stocks rose strongly, and materials and Meta, the sector that leads blue-chip technology stocks, rose nearly 4 per cent. Thanks to Friday's gains, other sectors rose throughout the week, except for the energy affected by the decline in US oil. Hot Chinese stocks continued to rise, outperforming the market on the third day of the week, and XPeng Inc., who rose nearly 8 per cent on Thursday, rose more than 7 per cent in intraday trading. European stocks rebounded across the board, with the technology sector leading the rise on Friday and leading the week. However, the energy sector fell against the market, reflecting the impact of the sharp fall in industrial metals on mining stocks.

The rally in US stocks came as risk aversion waned, the price of US Treasuries, which had soared for days, fell, yields rebounded, and the dollar returned to decline on Thursday, after three days of losses. After the release of the Michigan consumer survey data, the benchmark 10-year Treasury yield held steady above 3.10%, up more than 10 basis points from Thursday's nearly two-week low, with weekly yields still falling, ending a three-week rally. The dollar index fell further, falling below a fresh daily low of 104.00, its first weekly decline in a month.

Commodities that fell on Thursday accelerated their rebound after consumer inflation expectations in Michigan were announced. International crude oil futures are at a new high. Us WT crude oil rose more than 4% in a day, shaking off the six-week trough set on Thursday. Brent crude oil rose more than 3% at one point, and American oil still fell slightly throughout the week. Cloth oil recovered its losses in the previous days and was flat throughout the week. Gold futures rose in intraday trading, returning to $1830, ending a four-day losing streak and continued to fall throughout the week, but the decline was significantly more moderate than last week.

Most of the industrial metals that closed earlier than crude oil and gold failed to shake off the downward trend. Most of the domestic non-ferrous metals fell more moderately in night trading, while Shanghai tin still closed down more than 5%. London base metals continued to fall across the board. Lunxi, which closed down more than 7% in recent days, closed down more than 9% on Friday, and most London metals, such as Lunni, which fell nearly 9%, continued to hit at least a year's low. In addition to fears of a recession, Lunxi tumbled more than 20 per cent this week and was hit by a rebound in exchange inventories and the departure of capital profits. Although New York copper barely stopped the decline and stayed away from the trough of more than a year, it still suffered its biggest decline in a year, just like Lun Copper.

Meta leads the blue-chip technology stock Tesla, Inc. 's sector leads the rise throughout the week, the S & P energy sector fell alone throughout the week, almost outperformed the market on the 3rd of this week.

The three major u.s. stock indexes collectively opened higher, with the Dow Jones industrial average up nearly 840 points, or more than 2.7%, while the s & p 500 and NASDAQ composite index rose nearly 3.1% and 3.4%, respectively. In the end, the three major indexes closed higher for two days in a row, all hitting new closing highs since June 9. It closed at a new high since June 9.

The Nasdaq, which led gains for several days, closed up 3.34%, the biggest increase since May 13, to 11607.62 points. The s & p 500 closed up 3.06 per cent at 3911.74, up more than 3 per cent for the first time since may 18, 2020. The Dow closed up 823.32 points, or 2.68%, its biggest point gain since may 4, and refreshed Tuesday's biggest percentage gain since may 4, to 31500.68.

The Russell 2000, a small-cap index of value stocks, closed up 3.16%; the tech-heavy Nasdaq 2000 index closed up 3.49%, the biggest gain since May 13, up two days in a row.

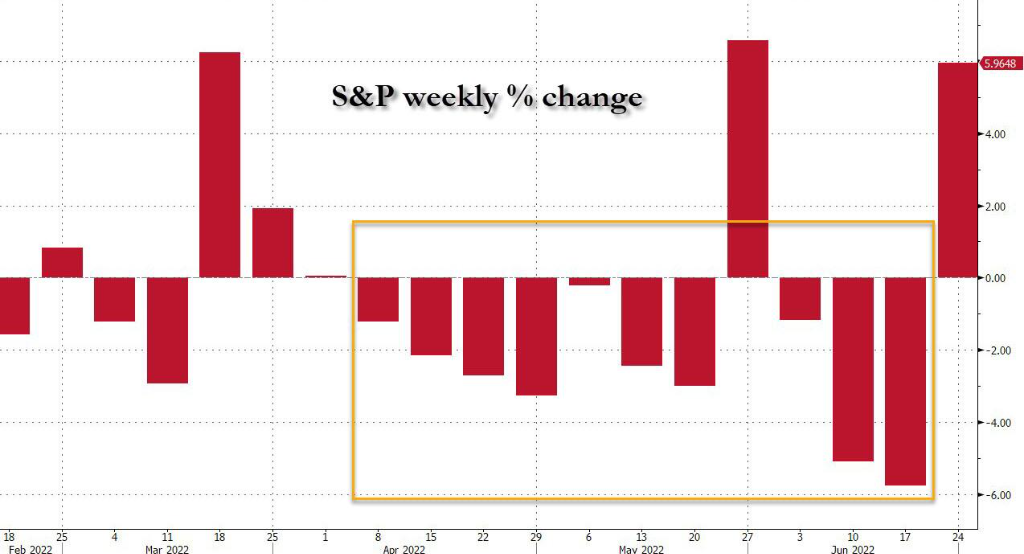

Major U. S. stock indexes rose sharply this week, sweeping away last week's decline and ending three weeks of losses. The Nasdaq, which fell nearly 4.8 per cent last week, rose 7.49 per cent this week; the S & P, which fell 5.8 per cent last week, rose 6.45 per cent, the second-biggest weekly gain this year; and the Dow, which fell 4.8 per cent last week, rose 5.39 per cent and rose in the second week of the last 13 weeks. The Nasdaq 100, which fell 4.8% last week, rose 7.45%, while the Nasdaq and S & P both rose in the second week of the last 12 weeks. Russell 2000, which fell 7.5 per cent last week, rose 6.01 per cent and rose in the second week of the last ten weeks.

The cumulative weekly performance of the S & P 500 in the past four months

The cumulative weekly performance of the S & P 500 in the past four months

All sectors of the S & P 500 rose, materials and Meta's communications services rose nearly 4 per cent, finance rose 3.8 per cent, Tesla, Inc. 's consumer discretionary rose 3.7 per cent, industry and Apple Inc's IT also rose more than 3 per cent, and the smallest energy rose more than 1.5 per cent. Only energy, which is down nearly 1.6%, has fallen this week, with consumer discretionary goods up more than 8%, real estate up 7.7%, IT and utilities up more than 7%, communications services up 7%, and materials at the bottom up 2.7%.

Leading technology stocks rose across the board, with Tesla, Inc. closing up 4.5% to reach a new high since June 2. Among the FAANMG's six largest technology stocks, Facebook Inc's parent company Meta closed up 7.2% to its highest level since June 10, Alphabet Inc-CL C's parent company Alphabet closed up 5.1%, Netflix Inc closed up 5% to the highest level since June 9, Amazon.Com Inc rose nearly 3.6%, Microsoft Corp rose 3.4%, all reached the highest level since June 8. Apple Inc closed up 2.45% to the highest level since June 9. Tesla, Inc. is up more than 13% this week, Alphabet is up about 10%, Amazon.Com Inc is up 9.6%, Netflix Inc is up 8.7%, Microsoft Corp is up more than 8%, and Apple Inc is up 7.7%.

Bank stocks performed well on Friday. Among the top five Bank of America Corporation, two Dow stocks, Goldman Sachs Group and JPMorgan Chase & Co, closed up 5.8% and nearly 3% respectively, Morgan Stanley rose more than 5%, Citigroup rose more than 3%, and Bank of America Corporation rose 0.7%. In addition, Wells Fargo & Co closed up 7.5 per cent, and Capital One rose 5.6 per cent.

Among the more volatile stocks, FDX, which had lower-than-expected earnings in the last quarter but had better-than-expected earnings guidance for the full year, closed up 7.2 per cent, while CCL closed 12.5 per cent higher after it announced that second-quarter orders were nearly double that of the first quarter, calling it the best order performance since the COVID-19 outbreak. Other cruise stocks also rose, with Royal Caribbean Cruise (RCL) up 15.8% and Norwegian Cruise (NCLH) up 15.4%.

Hot Chinese stocks outperformed the market on the third day of the week and the fourth of the last five trading days, with ETF KWEB and CQQQ closing up 3.7 per cent and 3.3 per cent respectively, up 7 per cent and 5.1 per cent this week. The Nasdaq Golden Dragon China Index (HXC) closed up 4% and is up 11% this week. Among the four constituent stocks in the Nasdaq 100 index, Baidu, Inc. rose nearly 3.6%, JD.com 3.4%, Pinduoduo 2.7% and NetEase, Inc 3%. Among other stocks, Kingsoft Cloud closed up more than 10%, XPeng Inc. 7%, BABA nearly 5%, NIO Inc Automobile, New Oriental Education & Technology, Trip.com, Zhihu Inc. up more than 4%, Li Auto nearly 4%, Tencent Music, DouYu International Holdings Limited, iQIYI, Dada up more than 3%, Tencent Fendan, TAL Education, Weibo rose more than 2%, e-cigarette first RLX Technology, Full Truck Alliance rose more than 1%, while Bilibili Inc. fell more than 0.1%.

In terms of European stocks, the pan-European stock index, which has been down for two days in a row, rebounded strongly. The European Stoxx 600 index not only broke from a 16-month low set on Thursday, but also posted its biggest gain since May 11 and closed at a new high since Wednesday. Stock indexes of major European countries rebounded across the board. All sectors closed higher on Friday, led by technology and media that rose more than 3.7%, while the medical and food sectors also rose more than 3%, with cars down nearly 4% leading the decline by more than 0.4% on Thursday.

This week the Stoxx 600 index rose for the first time in four weeks. Stock indexes of most countries also ended the trend of falling for three weeks in a row, only German stocks fell slightly, falling for four weeks. Only three sectors fell throughout the week, with basic resources of mining stocks falling nearly 5%, cars down 1.7%, and oil and gas down more than 0.1%. The technology sector rose nearly 5.4%, while personal and household goods also rose more than 5% throughout the week.

The 10-year Treasury yield rebounded more than 10 basis points from Thursday's low and ended three weeks of intraday rise in German bond yields, which fell more than 20 basis points throughout the week.

European bond prices were mixed, and German bond yields rebounded in intraday trading after days of sharp falls. By late European trading, the yield on UK 10-year benchmark government bonds closed at 2.302%, down 1.4 basis points on the day. The intraday measure was 2.27%, refreshing Thursday's lowest level since June 9. The yield on 10-year German bunds rose 1.5 basis points to 1.442% during the day, while European stocks fell to 1.355% in early trading, the lowest since June 9, and fell more than 7 basis points during the day. European stocks rose above 1.50% when they rose to a new session high.

UK bond yields fell 19.6 basis points this week, halting a five-week rise, while German bond yields fell 21.8 basis points, falling for the first time in five weeks.

The yield on the US 10-year benchmark Treasury note refreshed its daily low of 3.04% at the beginning of European trading, fell nearly 5 basis points during the day, and then continued to recover. European stocks rose more than 3 basis points in the day after rising 3.10% in intraday trading. U.S. stocks broke through 3.10% again in early trading and gave up all their gains and declines. after the Michigan survey was announced, it quickly returned to the upward trend, stood at 3.10%, and at one point approached 3.14% to refresh its daily high. It has rebounded more than 10 basis points from Thursday's nearly 3.00% last Friday, the low since the US CPI was announced in May, to about 3.13% at the close of trading, up 4 basis points on the day.

As a result of sharp declines on Wednesday and Thursday, 10-year Treasury yields fell about 10 basis points this week, ending three weeks of gains, despite Friday's rally.

The trend of Treasury yield since the announcement of CPI in the United States

The trend of Treasury yield since the announcement of CPI in the United States

The dollar index broke through 104 at one point and ended a three-week rally.

The ICE dollar index (DXY), which tracks a basket of the dollar's six major currencies, fell for most of Friday. The Asian market briefly broke through the 104.50 refresh session high in early trading and rose slightly by 0.08 per cent during the day. After the release of the Michigan Consumer Survey, it fell below 104.00 and fell nearly 0.5 per cent on the day.

By Friday's close, the dollar index was above 104.00, down more than 0.3% on the day and more than 0.5% this week, while the Bloomberg spot index fell about 0.3% and more than 0.6% this week, saying goodbye to three weeks of gains.

The offshore RMB (CNH) against the dollar fell below a fresh session low in early trading in Asia, and then continued to rise. U.S. stocks recovered 6.68 in early trading and finally rose for two consecutive days. At 04:59 Beijing time on the 25th, the offshore RMB was at 6.6816 yuan against the dollar, up 179 points from late Thursday in New York.

The yen fell in intraday trading, rebounded on Thursday and moved closer to a 24-year low. The USDJPY was steady above 135.00 in midday trading and was above 135.20 after closing, up nearly 0.3% on the day, still far from its highest level since October 1998, which broke through 136.70 on Wednesday.

The Russian rouble rebounded against the dollar after a five-day rally on Thursday, reaching a fresh session high of 53.10, close to its highest level since June 2015, which broke through 53.00 on Wednesday, and hit a seven-year high for two consecutive days as of Wednesday. It has risen more than 5% this week, up for four weeks.

The cryptocurrency rose for two days in a row. BTC rose above $21400 in intraday highs in Europe, up nearly $800, or 4%, from its intraday low in early trading in Asia. Us stocks closed above $21000, up nearly 3% in the last 24 hours, up more than 2% in the last seven days, and continue to stay away from the November 2020 low set by falling below $17700 on Saturday.

Us oil rose more than 3%, pulled out of a six-week low, fell for two consecutive weeks, European natural gas fell off a three-month high, and still rose more than 9% throughout the week.

International crude oil futures, which have fallen for two days in a row, accelerated their rebound in US stocks. After the release of the Michigan consumer survey, US WTI crude rose to $108.58, up more than 4.1 per cent on the day, while Brent crude approached $114,3.6 per cent on the day.

In the end, WTI August crude oil futures closed 3.353.21% higher at $107.62 a barrel, shrugging off Thursday's closing low since May 10, while Brent August crude oil futures closed up $3.07%, or 2.79%, at $113.12 a barrel, closing at a two-day low since May 18 on Thursday.

Us oil fell 0.3% this week, falling for two weeks in a row. Oil cloth closed flat on Friday, with zero gains and losses, not continuing the sharp decline last week. Last week, US oil and cloth oil fell by more than 9% and 7% respectively, the biggest weekly decline since April 1, ending seven consecutive weeks of gains.

Since the beginning of this year, US oil has experienced cumulative ups and downs in one week.

Since the beginning of this year, US oil has experienced cumulative ups and downs in one week.

Natural gas fell back in Europe. ICE UK natural gas futures, which rebounded on Thursday, closed down 9.15% at 169.74 pence / kcal, refreshing the low since June 13, which fell more than 10% on Wednesday. It is down 15.89% this week, giving up some of the nearly 40% gains last week. TTF benchmark Dutch natural gas futures, which rose for four consecutive days, closed down 3.63 per cent at 128.505 euros per megawatt hour, falling from Thursday's highest level since March 11, up 9.14 per cent this week and up for two weeks, but less than last week's more than 40 per cent rise.

Us gasoline and natural gas futures have been mixed. NYMEX July gasoline futures closed up 3.2% at $3.8848 a gallon, leveling out the decline that ended Thursday, rising 2.4% this week and ending a two-week losing streak. NYMEX July natural gas futures closed down 0.3% at $6.22 per million British thermal units, the lowest for two consecutive days since April 6, down more than 10% this week and falling for two weeks after falling more than 20% last week, the biggest decline in half a year.

Shanghai tin fell more than 5% in night trading, Lunxi fell more than 9%, hit a 15-month low, New York copper temporarily left the 16-month trough, gold ended four consecutive losses, but fell for two weeks.

Domestic non-ferrous metals continued to fall. Shanghai tin night trading, which closed down 9.49% during the day, Shanghai nickel night trading, which was down 8.91% during the day, closed down 4.34%. Shanghai zinc night trading, which fell 5.07% during the day, closed down 5.12%. Shanghai copper night trading, which fell 4.15% during the day, closed down 1.62%. Shanghai aluminum night trading, which was down 2.28% during the day, closed down 0.70%, and Shanghai lead night trading, which was down 1.39% during the day, closed down 0.20%.

London base metal futures continued to close lower across the board on Friday. Lunxi led the decline for three days in a row, falling more than $2000 a day. After falling more than 7% for two consecutive days, it fell nearly 8.9% on Friday, closing below $25000 for the first time since March last year, and Lun Copper, Lun Ni, Lun Aluminum and Lun Zinc all fell for three days in a row. Lun copper hit a second consecutive low since February last year, closing below $8400 for the first time in 16 months, but fell just over 0.3 per cent, far less than the biggest daily decline of more than 4 per cent on Thursday. Lunni fell nearly 7 per cent in one day and closed at $22400 for the first time since the end of January; Lun Aluminum hit a three-day low since July last year; Len Zinc hit a half-year low. Lun lead fell for four consecutive days to close below $1920, its lowest level since November 2020.

Base metals continued to fall across the board this week, with Lunxi, which has been down for two weeks, leading the decline, falling more than 21% this week, almost twice as much as last week. Lenny fell nearly 13%, falling for four weeks. Lead fell more than 7%, copper fell more than 6%, and zinc fell nearly 5%, all of which fell for three consecutive weeks. At the bottom of the decline, Lomalco fell about 1.7% for five consecutive weeks.

New York copper barely stopped its two-day decline. Comex copper for July delivery closed up 0.04% at $3.7405 / lb, still close to Thursday's closing low since February last year, falling 6.8% this week. Helen copper suffered its biggest weekly decline in a week since June 18, falling for three weeks.

New York gold futures fell below $1820 before the US stock market, down nearly 0.7% on the day. After the release of the Michigan Consumer Survey, New York gold futures rose back to $1830, wiping out all day losses and rising. In the end, COMEX August gold futures closed up 50 per cent at $1830.30 an ounce, breaking Thursday's closing low since Tuesday, ending a four-day losing streak, but it is still down 0.6 per cent this week for two weeks after falling 1.8 per cent on Tuesday, far less than the biggest drop in a month of nearly 2 per cent last week.

Edit / emily