The three major indexes all fell in intraday trading. After the Powell hearing, they all rose and closed at a two-week high, while the energy sector fell nearly 4 per cent against the market. China probably outperformed the market on the second day of this week, with Li Auto Inc. up nearly 7 per cent and BABA Pinduoduo up more than 6 per cent. The pan-European stock index hit a 16-month low a week later, with the auto sector down nearly 4% and Deutsche Bank down 12%.

The yield on 10-year US Treasuries was close to 3.0 per cent, a two-week low, and German yields fell more than 20 basis points a day for the first time in more than three months. The yen pulled out of its 24-year low and the dollar index reversed three consecutive declines and failed to recover.

Lunxi fell more than 7% in a row, a 14-month low, and Lunxi copper fell more than 4%, the biggest drop in a year and a 16-month low. Gold hit a new low in more than a week in a row. Us Oil hit a new six-week low. Natural gas in Europe rose nearly 5%, hitting a three-month high in three days.

Poor economic data: last week, initial jobless claims fell below expectations for three consecutive weeks, while initial PMI in manufacturing and services fell more than expected in June, hitting two-year and five-month lows, respectively. After explicitly acknowledging in his testimony on Wednesday that higher interest rates could lead to a recession, Federal Reserve Chairman Powell testified in Congress the next day that he did not think a recession was inevitable, but acknowledged that raising interest rates risked an increase in unemployment. and reiterated the most hawkish argument in the semi-annual monetary policy report that the Fed is "unconditionally" committed to fighting inflation.

Investors continued to weigh the risk of recession, with all three high U.S. stocks falling, while the energy sector, which is sensitive to economic prospects, continued to lead the decline, while most sectors rose, led by the defensive sector, utilities and healthcare sectors. After the Powell hearing, the three major indexes held gains until the close. Technology stocks that are sensitive to rising US bond yields have mostly rebounded. Some popular Chinese stocks rebounded strongly, with Pinduoduo taking the lead in NASDAQ 100 stocks. The National standing Committee will clearly increase support for car consumption, which is expected to increase by 200 billion yuan this year. XPeng Inc. rose more than 8% during the day. Li Auto Inc., which was confirmed by Ningde Times that its models will carry its latest Kirin battery, rose nearly 9% in intraday trading.

Expectations of an aggressive Fed rate hike have cooled, and the overnight interest rate swap market expects the Fed to end its rate hike cycle as early as this year and may even cut interest rates by 50 basis points next year. Treasury prices accelerated after the PMI announcement, with benchmark 10-year Treasury yields falling more than 10 basis points for the second day in a row, at one point approaching 3.00%, falling to a nearly two-week low, giving up all the gains since the higher-than-expected CPI spike in May was announced two weeks ago.

After the announcement of the PMI, the dollar index accelerated its decline and fell in the short term. Although the rise finally reversed the trend of three days of decline, it failed to recover 105.00 close to the high set last week since the end of 2002. The yen, a safe-haven asset, rebounded in intraday trading, putting aside its 1998 lows. The dollar fell more than 1% against the yen at one point in intraday trading.

Norway's central bank raised interest rates by 50 basis points more than expected, the biggest increase in two decades. The euro zone's composite PMI fell more than expected in June to a 16-month low, with economic locomotives slowing sharply in France and Germany. European bond yields plummeted, with benchmark 10-year German bunds falling more than 20 basis points a day for the first time since early March. European stocks fell further on heightened concerns about economic growth, with the German stock index, which announced the second alert of the natural gas emergency plan, the biggest decline among European countries, led by the economy-sensitive auto sector, and banks dragged down by European bond yields.

Among commodities, fears of a recession topped, industrial metals continued to fall, Lunxi fell by more than 7% in one day, and copper fell by more than 4% for the first time in a year, joining hands with most other London base metals to hit a more than a-year low. Precious metals also fell, with gold rising during the dollar's intraday pullback and finally continuing to close down, rising to an one-month low set on Tuesday. Crude oil futures also continued to fall on fears of recession, with US oil hitting a six-week low. While Germany has entered a secondary state of alert for natural gas, warning that the cut-off of natural gas supply will trigger a "Lehman-style crisis", consumers may face a sharp rise in gas prices, and European natural gas will outperform among commodities. Dutch natural gas futures, the continental European benchmark, closed at a three-month high.

After the Powell hearing, the three major US stock indexes all rose and the energy sector led the decline against the market. On the second day of the week, they outperformed the broader market, automobile and banking stocks, and led European stocks lower.

The three major US stock indexes collectively opened higher, with mixed performance in intraday trading. The Dow Jones industrial average rose more than 230 points, or nearly 0.8%, when it was high in early trading, and fell at the end of the morning. During the Powell hearing, it fell nearly 190 points, or more than 0.6%, during the midday session. The s & p 500 index rose nearly 1% when it was at its high in early trading and fell more than 0.4% at its low after midday. The Nasdaq composite index fell early and short-term, rose more than 1.5% at the new session high at the end of early trading, and gave up almost all its gains at midday.

After the Powell hearing, the Dow and S & P completely pulled out of the decline. In late trading, the three major indexes rose, and the Dow rose again to more than 200 points. The S & P and Nasdaq rose to new highs, rising more than 1.1% and nearly 1.9% respectively during the day.

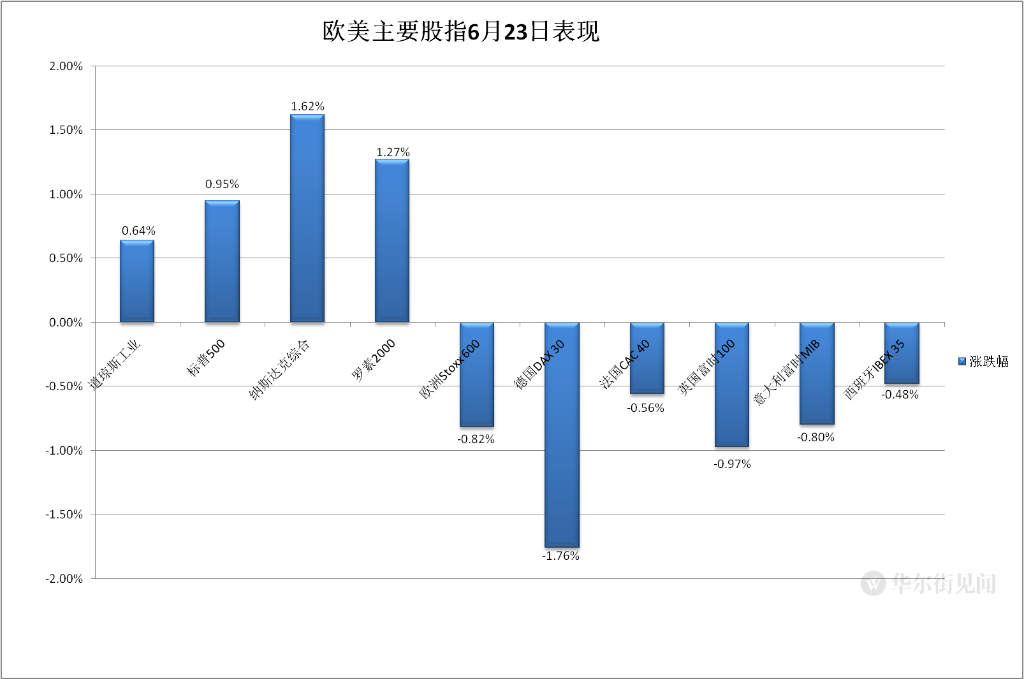

In the end, the three major stock indexes closed higher, all erasing the closing losses that fell on Wednesday, all reaching their highest close since June 10. The Nasdaq, which led gains, closed up 1.62% at 11232.19; the s & p, which closed down 0.13% on Wednesday, closed up 0.95% at 3795.73, still down more than 20% from its closing high on Jan. 3, and has yet to break out of the bear market; and the Dow, which closed down 0.15% on Wednesday and the Nasdaq, closed up 194.23 points, or 0.64%, at 30677.36.

The Russell 2000 index of small-cap stocks, which is dominated by value stocks, closed up 1.27%, while the technology-heavy Nasdaq 2000 index closed up 1.47%, wiping out all the losses that ended Wednesday. Pinduoduo, a Chinese stock, has an eye-catching performance among the NASDAQ 100 constituent stocks.

Dow, S & P, Nasdaq and Russell 2000 Thursday trend

Only four of the major S & P 500 sectors closed lower on Thursday, led by energy, which fell nearly 3.8%, materials fell 1.4%, and industrial and financial fell about 0.5%. Public utilities and health care rose by more than 2%, real estate and essential consumer goods rose by about 2%, and communications services, which had the smallest increase, rose nearly 1.1%.

Most leading technology stocks rose. Tesla, Inc., who rose more than 9 per cent on Tuesday, fell for two days in a row and closed down 0.4 per cent on both days. Among the six major technology stocks in the former FAANMG and now GANMMA, Amazon.Com Inc closed up 3.2%, Microsoft Corp rose nearly 2.7%, and Apple Inc rose nearly 2.2%, all reaching two-week highs. Facebook Inc's parent company Meta rose nearly 1.9%, and Netflix Inc, which rose nearly 4.7% on Wednesday, closed up nearly 1.6%, the highest since Friday, June 10. Alphabet Inc-CL C's parent company Alphabet rose nearly 0.7% to a two-week high.

Chip stocks ended lower overall against the market, with the Philadelphia semiconductor index and semiconductor industry ETF SOXX both down nearly 0.7 per cent. Among the IT stocks of S & P 500s, AMD and Qualcomm Inc fell more than 1 per cent, Yingweida fell 0.8 per cent, Applied Materials Inc fell 0.7 per cent, Lam Research Corp fell nearly 0.4 per cent, Seagate Technology fell 0.2 per cent, Intel Corp and Broadcom Ltd rose less than 0.1 per cent.

Among the stocks that reported results, Rite Aid (RAD), a drugstore chain with higher-than-expected quarterly revenues and lower-than-expected losses, closed up nearly 20 per cent; KB Home (KBH), which had better-than-expected quarterly revenues and profits and reiterated its guidance for the current fiscal year, closed up 8.7 per cent; and Factset Research Systems (FDS), a financial data company with better-than-expected quarterly revenue and earnings and expected to grow at the top end of the previous guidance, closed up 8 per cent.

Among the volatile stocks, WeWork (WE), a shared office space company, closed up 15.8% after Credit Suisse first covered its overweight rating and a target price of $11, more than double Wednesday's closing price. Snowflake Inc (SNOW), a cloud data service, closed up 12.4% after JPMorgan Chase & Co upgraded its rating from neutral to overweight and reiterated its target price 30% higher than Wednesday's close. Funko (FNKO) closed up 12.7 per cent after JPMorgan Chase & Co upgraded its rating to overweight from neutral for treating the toy industry as a safe haven; gun maker Smith & Wesson Brands (SWBI) closed up 9.6 per cent after the US Supreme Court ruled that New York state gun restrictions were invalid; and cloud software maker Veeva Systems (VEEV) closed 6.5 per cent higher after it was first covered by Goldman Sachs Group for its buy rating for its leading position in CRM solutions. REV, which rose for three days and gained more than 400 per cent over three days after filing for bankruptcy last week, closed down nearly 11.6 per cent, while UAL closed down 2.5 per cent after cutting daily flights from Newark airport in New Jersey by 12 per cent to reduce flight delays.

Hot Chinese stocks outperformed the market on the second day of the week and the third day of the last four trading days, with ETF KWEB and CQQQ closing up about 2.5 per cent and 1.8 per cent respectively. The Nasdaq Golden Dragon China index (HXC) closed up nearly 3.1 per cent. Of the four stocks on the Nasdaq 100th index, Pinduoduo closed up 6.4 per cent, Baidu, Inc. 2.4 per cent, JD.com nearly 0.8 per cent, and NetEase, Inc fell nearly 0.9 per cent. Among other stocks, XPeng closed up nearly 8% to its highest level since early March. Li Auto, which had risen more than 8.7% in intraday trading, closed up 6.6%, the highest level since November 27, 2020. Dingdong rose more than 7%, BABA and Dada rose more than 6%. The first e-cigarette stock, RLX Technology Inc., rose more than 4%, iQIYI, Inc. and Vipshop Holdings Limited rose more than 3%, and NIO Inc. Automobile, TAL Education Group, HUYA Inc. and Xunlei rose over 2%. Tencent Fan Dan, Full Truck Alliance Co. Ltd., Kingsoft Cloud Holdings, Zhihu Inc. and Weibo Corp rose more than 1%, while New Oriental Education & Technology Group, who just finished three consecutive declines on Wednesday, closed down nearly 9%, DouYu International Holdings Limited fell more than 4%, Gaotu Techedu Inc. Education fell 0.5%, and NetEase youdao fell nearly 0.4%.

In terms of European stocks, the pan-European stock index fell for two days in a row, and the European Stoxx 600 index broke its closing low since February 1 last Thursday. Stock indexes of major European countries continued to fall across the board. Among the 600 sectors, only personal and household goods that rose more than 1 per cent, public utilities and health care that fell nearly 0.6 per cent rose on Thursday, cars that fell more than 3.6 per cent led the decline, banks also fell more than 3 per cent, and basic resources for mining stocks fell 2.5 per cent. Oil and gas and real estate fell nearly 2%. Among individual stocks, the two major German banks, Deutsche Bank and Commerzbank, both closed down about 12%, leading the decline in the banking sector, with the German stock index leading the decline among countries.

The 10-year Treasury yield is close to 3.0% in intraday trading, hitting a two-week low. German bond yields fell more than 20 basis points a day for the first time in more than three months.

The price of European government bonds that rebounded on Wednesday expanded, with yields falling more than on Wednesday, when they fell more than 10 basis points a day. On Thursday, the yield on UK benchmark 10-year government bonds closed at 2.31 per cent, down 18 basis points on the day. Us stocks broke through 2.30 per cent in early trading, the lowest since June 9, while German bunds closed at 1.42 per cent, down 21 basis points on the day. For the first time since March 1, they fell more than 20 basis points a day, while US stocks broke 1.40 per cent in early trading, the lowest since June 10.

The trend of bond yields of European countries since May last year

The yield on US 10-year benchmark Treasuries continued to decline sharply on Thursday. European stocks initially measured 3.17% to refresh their daily highs, rising more than 1 basis point within the day, but quickly returned to the downward trend. After the announcement of PMI, the decline accelerated, and US stocks once approached 3.00% in early trading, hitting a new low since last Friday on June 10, giving up all the gains since the higher-than-expected CPI was announced on June 10, falling nearly 16 basis points in the day. After Wednesday, the intraday decline again exceeded 10 basis points, and the decline narrowed after the Powell hearing, to about 3.08% at the close of trading in the United States, and down about 8 basis points on the day.

The trend of 10-year Treasury yields since the announcement of US CPI on June 10th

The yen rose in intraday trading to shake off its 24-year trough and the dollar index reversed three consecutive declines and failed to recover.

The exchange rate of the yen, which has hit a new low in nearly 24 years, rose during the day. The USDJPY was above 136.00 in early trading in Asia, close to the high since October 1998 set by breaking through 136.70 on Wednesday, and soon fell 136.00. European stocks fell further in intraday trading. After the US stock market turned lower, US stocks fell below 134.30 at the beginning of the day and fell more than 1 per cent on the day. By the end of the day, US stocks closed just below 135.00, down nearly 1 per cent on the day.

The ICE dollar index (DXY), which tracks the exchange rate of a basket of six major currencies, approached 104.00 during the session and fell more than 0.1% during the day. European stocks rose after the early session, and European stocks rose close to 104.80 when they were high in early trading and rose more than 0.5% during the day. The number of first-time jobless claims in the United States continued to decline after the announcement of unemployment benefits last week. The decline accelerated after the announcement of PMI in June, and American stocks fell at one point in early trading. It quickly rose, but failed to rise above 105.00 throughout the day, failing to approach the intraday high of 105.80 last Wednesday, which was the highest since December 2002.

By Thursday's close, the dollar index was above 104.30, up more than 0.1% on the day, while the Bloomberg spot index rose slightly, ending three days of losses.

Performance of Bloomberg Dollar spot Index in the last five trading days

The offshore renminbi (CNH), which has been down for two days in a row, rose in intraday trading, narrowly falling below the 6.72mark when European stocks refreshed their session lows in early trading, and then continued to rally. Us stocks recovered 6.70. at 04:59 Beijing time on the 23rd, the offshore RMB was at 6.6995 yuan against the dollar, up 132 points from late Wednesday in New York, off an one-week low set by falling below 6.73 on Wednesday.

Lunxi copper fell by more than 7% in a row, a 14-month low, the biggest drop in a year, and a 16-month low in gold hit a new low in more than a week.

London base metal futures closed down for the second straight day on Thursday. Lunxi continued to lead the decline, although the decline was slightly lower than on Wednesday, but it has fallen more than $2000, or more than 7%, for two consecutive days, closing below $27000 for the first time since April last year, and Lun Copper, Lun Aluminum, Lun Zinc and Lunni all fell for two days in a row. Lun copper fell more than 4 per cent, the biggest drop in a year, closing near the $8400 mark for the first time since February last year, after hitting a 16-month low on Wednesday. Len aluminum continued to refresh its low since July last year. Len zinc hit a new low in more than a month on the third day of the week. Lenny hit a four-month low. Lun lead fell for a third straight day, closing below $1950 on Thursday for the first time since March last year, after hitting a 14-month low on Wednesday.

New York copper for delivery fell for two days in a row, while Comex July copper, which fell more than 2 per cent on Wednesday, closed 5.2 per cent lower at $3.739 a pound, hitting its lowest close since February last year after falling below $4 for the first time in 16 months on Wednesday.

Copper futures in New York fell to a low in more than a year.

Metal futures in the inner market also closed lower at night. Leading the decline, Shanghai Tin closed down 6.19%, Shanghai Copper closed down 4.02%, Shanghai Nickel closed down 2.69%, Shanghai Zinc closed down 2.56%, Shanghai lead closed down 0.63%, and Shanghai Aluminum closed down 0.57%.

New York gold futures fell to $1825.3 when European stocks refreshed their daily lows in early trading, down more than 0.7% on the day. Us unemployment data and PMI accelerated after the release of US unemployment data and PMI. After the initial rally, US stocks rose nearly US $1849 in early trading and rose nearly 0.6% during the day. They fell at the end of early trading and finally rebounded and closed down for four consecutive trading days. COMEX gold futures for august closed 0.5% lower at $1829.80 an ounce, the lowest since Tuesday, June 14, and the lowest since may 13, when it fell below $1814 on June 14.

The trend of New York Futures over the past year

Us Oil hit a new six-week low European natural gas rose nearly 5% in three days to a three-month high.

International crude oil futures fell for two days in a row, but not as low as Wednesday. Us WTI crude, which fell more than 7 per cent on Wednesday, fell more than 3.6 per cent during the session low, close to its intraday low of $102 on Wednesday, and Brent crude, which fell nearly 7 per cent, fell about 6 per cent to close to $105on Wednesday.

In the end, WTI August crude oil futures, which closed down more than 3 per cent on Wednesday, closed 1.81 per cent lower at $104.27 a barrel, the lowest since May 12 on Wednesday and the lowest since May 10 on Wednesday. Brent August crude oil futures, which closed down more than 2.5 per cent on Wednesday, closed 1.51 per cent lower at $110.05 a barrel, the second consecutive day of low since May 18.

Natural gas is on the rise in Europe. ICE UK natural gas futures closed up 1.75 per cent at 186.84 pence per kcal, breaking the low since Monday on June 13, which fell more than 10 per cent on Wednesday. TTF benchmark Dutch natural gas futures closed up 4.86% at 133.347 euros per megawatt hour, the second consecutive high since March 11, and on Tuesday broke the closing high set last Wednesday and Thursday since March 31 for the fourth straight day.

U. S. gasoline and natural gas futures fell. NYMEX July gasoline futures, which rose for two days in a row, closed down 1.8% at $3.7656 per gallon, while NYMEX July natural gas futures, which ended five consecutive declines on Wednesday, closed down 9% at $6.239 per million British thermal units, the lowest since April 6.

Us Oil and European and American Natural Gas Futures since the explosion at the Freeport liquefied Natural Gas (LNG) plant in Texas two weeks ago

Edit / somer