Seven consecutive years of profitability, the scarce investment target of the SaaS industryTian Runyun (temporary Code) (810125.HK) $。

SaaS has always been regarded as a "slow bull" track by capital. The deep stickiness of users and the commercial nature of network effects make this sector extremely easy to give birth to long cattle. From 2009 to 2019, there were 98 software companies listed on the US capital market, 80% of which were SaaS software companies, which is four times the number of listed consumer technology companies in the same period. In the past 2021 alone, 27 SaaS software companies were listed in the US capital market. In China, SaaS's excellent business model has also successfully attracted wide attention from A-share and Hong Kong stock investors.

At the same time, the trend of "cloud migration" is expanding in China, and various industries are speeding up the digital transformation. According to the iResearch Consulting report, China's enterprise-level SaaS market is about 53.8 billion yuan in 2020 and is expected to expand at a compound growth rate of 34 percent in the next three years, with the market size exceeding 100 billion yuan. According to Zhitong Financial APP, the SaaS industry in the spotlight will usher in a new face of the capital market-Tian Runyun. According to market news, the new member has been listed through the Hong Kong Stock Exchange and will be listed soon.

Seven consecutive years of profitability, a scarce investment target for the SaaS industry

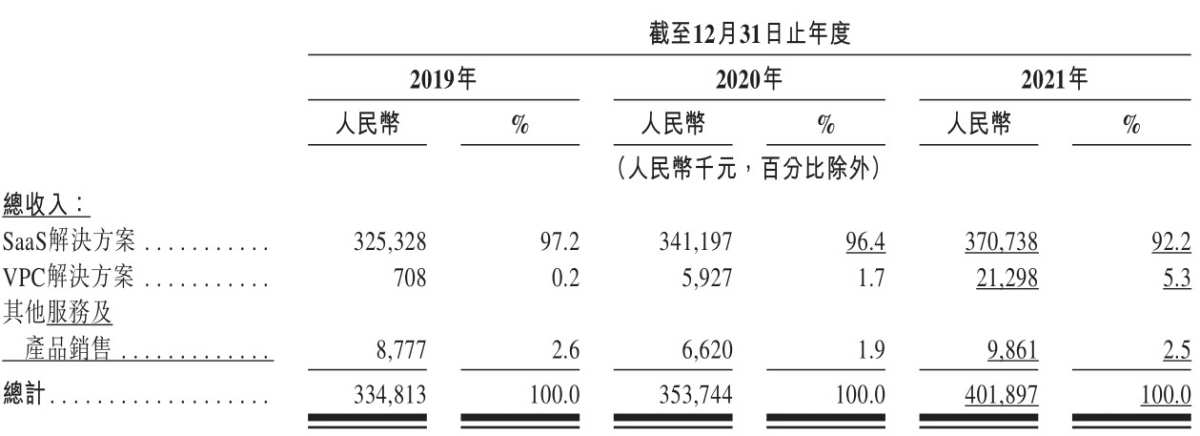

For the emerging SaaS industry, most companies are constantly exploring and verifying their business models in the midst of losses, and profitability is a difficult problem for most enterprises. Especially in the macro environment full of uncertainty, most excellent enterprises no longer advance by leaps and bounds, but turn their business focus to reduce costs and increase efficiency, and the investment logic of the SaaS track has also changed. Specifically, capital has become more rational because it has become disgusted with the barbaric growth model of increasing scale through burning money in the past. Tian Runyun is definitely a special case of domestic SaaS companies. Since its establishment in 2006, the company has gradually become a leader in the industry by relying on years of strong endogenous growth and excellent profitability. According to the prospectus, from 2018 to 2020, Tian Runyun's operating income was 335 million yuan (in RMB), 353 million yuan and 402 million yuan respectively, rising steadily year by year. By the end of December 2021, Tian Runyun had made a profit for seven consecutive years.

As a leader in SaaS industry segment, Tian Runyun mainly provides full-cycle customer contact solutions based on public cloud, which are divided into SaaS and VPC solutions, of which SaaS solutions account for more than 92% of the annual revenue.

According to Zhitong Financial APP, Tian Runyun's solution is based on cloud's native safe and reliable platform to provide platform services for customer contact scenarios in the three core operation processes of enterprise customers: camp, sales and service, so as to create a good customer contact experience. In 2021, the company has promoted more than 3 billion interactions between enterprises and their customers through various channels, making every effort to improve the production efficiency of enterprises.

Second, with the moat and scale advantages established by technology, Tian Runyun gains a wide range of high-quality and loyal customers, including leading enterprises in technology, insurance, automobile, tourism, real estate, medical and other industries. The number of customers served by the company has also increased from more than 2200 in 2019 to more than 3100 in 2021, with a compound annual growth rate of nearly 20 per cent. Among them, 57 are major customers, with an annual purchase amount of more than 1 million yuan. In particular, the company has occupied an outstanding market position in the technology and insurance industries. Among the top 20 companies in China's technology and insurance industries by revenue, Tian Runyun provides services for 13 and 8 companies respectively.

In short, Tianrun Cloud has become the first choice for market leaders in various industries with superior SaaS solutions, which also lays the foundation for it to improve market penetration.

Two logics of continuous improvement of profitability

Tian Runyun can achieve seven consecutive years of profitability, and profitability is expected to continue to improve, inseparable from two major logic: highly flexible solutions and high-quality head customer base.

First of all, behind the highly flexible solutions are more than 500 programming interfaces (API) and software development tools (SDK) provided by the company. Tian Runyun's main SaaS solutions are delivered directly to major customers through API and SDK, so that major customers can flexibly and easily integrate the company's products and technical capabilities into their own systems and empower their local systems, which is very similar to the business model of advanced software companies in Europe and the United States. Under this delivery model, the company no longer needs to invest a lot of R & D resources for interface-level development, but focuses on the evolution of API and SDK, making the company's solutions suitable for a wider range of scenarios, effectively reducing customized development time, thus continuously improving R & D efficiency and leading domestic counterparts in terms of business model.

Secondly, according to the observation of Zhitong Financial APP, Tianrun Cloud adopts a growth strategy based on key customers, which can quickly expand the scope of customers' industries, while the widely distributed customer base enables Tianrun Yun's solutions to apply to various industries and rapidly expand their business among new customers in the same industry, so that in large-scale digital changes, with significant first-mover advantages, seize growth opportunities. According to the prospectus, Tian Runyun's revenue from big clients accounted for 74.5% of its total revenue in 2021. By maintaining a long-term cooperative relationship with a wide range of and high-quality customer groups, the retention rate of the company's SaaS key customers has exceeded 105% for many years in a row, reflecting the high recognition of Tian Runyun SaaS solution by the head enterprise customers. More importantly, in the context of today's uncertain macro environment, the business of major customers is more robust and the growth certainty is higher.

At present, this logic has been verified by the company's head customer base. According to the prospectus, the total income of top customers (the top 20 in the industry) from the top three customer industries, such as technology, increased from 123 million yuan in 2019 to 195 million yuan in 2021, with a compound annual growth rate of 26.0%. Key customer revenue contribution continues to rise, reflecting the strong competitiveness of Tian Runyun SaaS solution.

In short, flexible and effective solutions and a high-quality customer base drive significant network effects. the more large enterprises the company serves, the deeper the company's understanding of customer needs, and the needs of these leading enterprises continue to drive the evolution of the company's products. product iterations precipitate the best industry practices. The more API and industry practices the company accumulates in the process of project implementation, the more business and customers the company obtains, which increases the certainty of sustained high growth of performance.

SaaS track has high growth, focus on endogenous growth, high certainty of performance.

Tian Runyun is basically good, and can not do without the blessing of the track dividend. Judging from the industry track, the industry of cloud-based customer contact solutions in China has developed rapidly in recent years.

The market size of cloud-based customer contact solutions in China (by revenue) has increased from 3.2 billion yuan in 2016 to 10.6 billion yuan in 2021, and is expected to reach 30.7 billion yuan in 2026, according to the report. Among them, revenue generated by public cloud customer contact solutions has exploded, from 700 million yuan in 2016 to 4 billion yuan in 2021.

As a large part of the revenue from China's cloud-based customer contact solution providers comes from companies in the technology, retail and insurance sectors, which have a large potential market, the public cloud track as a whole has significant dividends. For example, revenue generated by the technology sector increased from Rmb400m in 2017 to Rmb1.6 billion in 2021, with a compound annual growth rate of 32.0 per cent. At the same time, it is expected to reach 6.1 billion yuan in 2026. With its experienced and insightful management team, Tian Runyun has advanced the layout of a series of blue sea races, such as remote agents, robot agents and VPC solutions, and has achieved rapid growth in recent years to take full advantage of new opportunities in the industry. According to the prospectus, as of 2021, the company's revenue from remote agents, robot agents and VPC solutions increased by 87.4%, 54.0% and 261.0% year-on-year, providing a strong driving force for sustained high-quality growth in the future, and further confirmed Tian Runyun's determination to lead the industry and innovate the way companies interact with customers.

With the expanding capacity of the industry, as the largest public cloud customer contact solution provider in China, it is expected to continue to benefit from the advantage of scale and enjoy the leading dividend. The important catch behind the sustained growth of performance is the absolute advantages and barriers that Tian Runyun has established over the years. According to the understanding of Zhitong Financial APP, as a pioneer in the industry, the company has developed a set of cloud native smart, secure, reliable and scalable customer contact solutions, while close interaction with leading customers gives it a first-mover advantage in solution upgrades, thus setting up high barriers to entry that are difficult for emerging enterprises to overcome. In 2019, Tianyun was the first customer contact solution provider in China to integrate the platform with Software-defined wide area Network (SD-WAN). The unique SD-WAN connection enables Tianyun's solution to ensure a stable and reliable connection even in the event of a sudden surge in service usage. And the company can provide services on two cloud computing platforms at the same time, becoming the only industry enterprise to achieve dual-cloud and dual-active deployment, achieving excellent reliability and availability, which is also what the head customers value most.

From the perspective of endogenous growth, the company increases the building of marketing capacity and strategically and effectively expands its customer base. Chinese companies are still in the early stages of digital transformation, and the need to replace traditional contact center systems with cloud-based solutions is expected to increase significantly over the next decade, according to the cautionary report. Tian Runyun will strengthen its sales capability by expanding its direct sales team, providing more training opportunities and upgrading its CRM system. At present, the company has regional sales offices in Beijing, Shanghai, Nanjing, Shenzhen and Guangzhou, and then plans to set up new regional sales offices in East, Central and Southwest China. The company will maintain its leading position in the technology and insurance industries and enter sizeable unsaturated markets such as banking, automobiles and consumer goods. Over the years, focusing on endogenous growth, Tian Runyun continues to consolidate its market position and maintain a high degree of certainty of performance growth.

In terms of exogenous growth, Tian Runyun will also focus on strategic acquisitions and investments, choosing strategic acquisitions and investments that can help the company enrich its products, improve its technology and expand its customer base, so as to form a sustainable and mutually beneficial relationship with it and consolidate its market position.

To sum up, the SaaS industry is an emerging industry, which represents the process of enterprise digitization, especially after the outbreak of the epidemic, the willingness of enterprises to digitize has increased greatly. Considering from this aspect, the future performance growth of SaaS enterprises can be guaranteed, and on the basis of stable growth expectations, Tian Runyun has steadily improved profitability, which can be said to have the advantages of both growth stocks and value stocks.