Source: Wall Street

Author: Han Xuyang

Michael Wilson said in a recent research report that in predicting stock market valuationsTwo components are very important-the 10-year Treasury yield and the equity risk premium (ERP).The price-to-earnings ratio and the yield on 10-year Treasuries can be observed from market prices at any given time. Therefore, the stock risk premium is only a derivative of these independent variables, making it relatively unstable.

He believes that the biggest driver of changes in the stock market so far this year has been the decline in valuations.The valuation of the s & p 500 is down about 20 per cent, while the point is down only 15 per cent; at its low a few weeks ago, valuations are down nearly 24 per cent and point is down 20 per cent.At that time, the average price-to-earnings ratio was 16 times earnings, which was exactly in line with Morgan Stanley's expectations for this year's rating, but higher than its current estimate of 14.6 times.(it assumes an equity risk premium of 370 basis points and a 10-year Treasury yield of 3.15%.)

Predicting stock market valuations may be one of the hardest things for investors to do, but it's easy to judge when valuations go off track, Michael Wilson concluded.

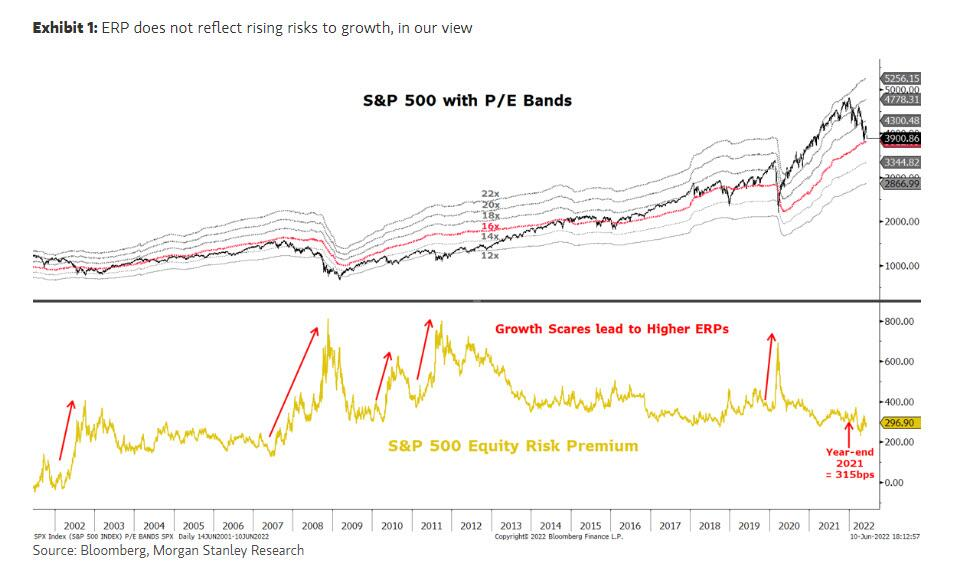

For example, in March 2020, stock market valuations plummeted as markets panicked about the impact of the epidemic blockade and the recession on growth and earnings.At market lows in 2020, the equity risk premium reached nearly 700 basis points; it has been exceeded only twice in the past 30 years-the global financial crisis in 2008 and the downgrade of US Treasuries in the summer of 2011.

He pointed out that both things are terrible for investors.But they all proved to be excellent buying opportunities.In 2020, the 700bp equity risk premium was the main reason why Morgan Stanley turned bullish at the right time.In this case, the market will always fall, but lower valuations provide a buffer for the wrong time.

The opposite was true at the end of last year, with a price-to-earnings ratio of 21.5 times. From the Michael Wilson's point of view, both interest rates and equity risk premiums seem to be mispriced. Obviously,Interest rates are more influenced by inflation expectations and Fed policies.

By the end of last year, 10-year Treasuries did not correctly reflect these two risks. This is not the case today. In fact, if economic growth remains sluggish and the risk of recession intensifies, 10-year Treasuries could "overreact" to the Fed's tightening policies, as consumer confidence data released on Friday suggest.

He also pointed out that, unlike interest rates, the equity risk premium largely reflects growth expectations.When growth accelerates or decelerates, the equity risk premium is lower or higher, respectively.

At the end of last year, the equity risk premium was 315 basis points, well below the average of the past 15 years and below JPMorgan's estimate of 335 basis points at the time. In short, the equity risk premium does not reflect the increase in growth risks that the agency expects this year. Even today, the equity risk premium is even lower, at 295 basis points, 75 basis points below JPMorgan's current estimate.

But given slowing growth and growing signs of profit risk, the equity risk premium is expected to rise further, which is why the S & P 500 will move towards 3400 before a low where it is easier to "buy on a bargain".

As growth remains a major risk to the stock market, Michael Wilson also points out that the agency's focus remains on companies that can make money in an unmanageable environment. With the S & P 500 still facing challenges, this is still a tough year for stock pickers.Morgan Stanley continues to favor typical "post-cyclical winners", namely defensive and energy companies, as well as companies with high operational efficiency.

Edit / Jeffrey