Source: Zhong Zhengsheng / Zhang Lu, Ping an Shoujing team

Author: Zhong Zhengsheng's Economic Analysis

In may 2022, us CPI reached 8.6 per cent year-on-year, exceeding market expectations again, underscoring the need for the fed to accelerate tightening. After the Federal Reserve officially opened the contraction table in June, money market interest rates are generally stable, but the superimposed impact of "contraction + interest rate hikes" on asset prices is still vigilant.

Core viewpoints

On May 4, 2022, the Federal Reserve announced that it would reduce its holdings by $47.5 billion a month, starting on June 1, and increase to $95 billion three months later.

How is this Fed contraction different from what it used to be? What are the changes in the impact on the market? This paper attempts to answer the above questions.

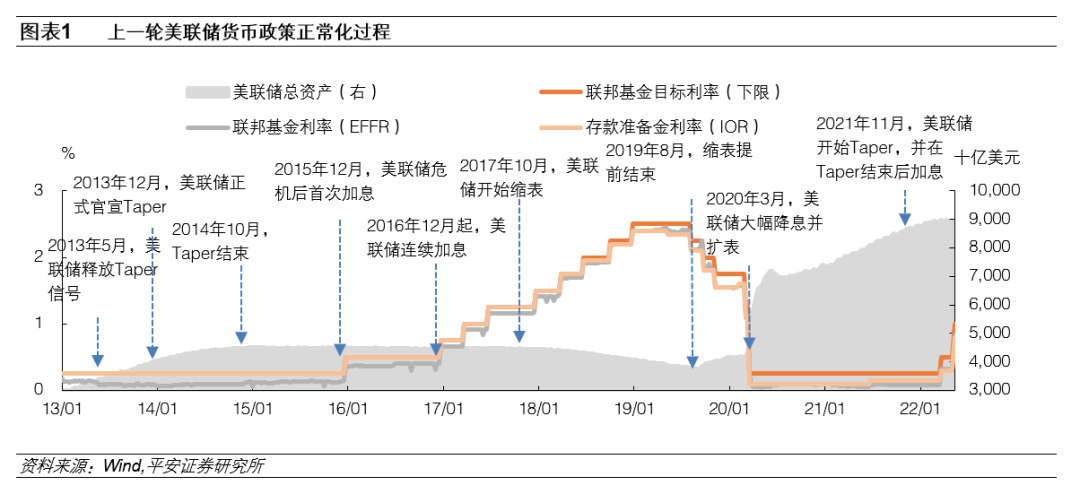

Looking back at the last round of Fed retrenchment, we can see that:

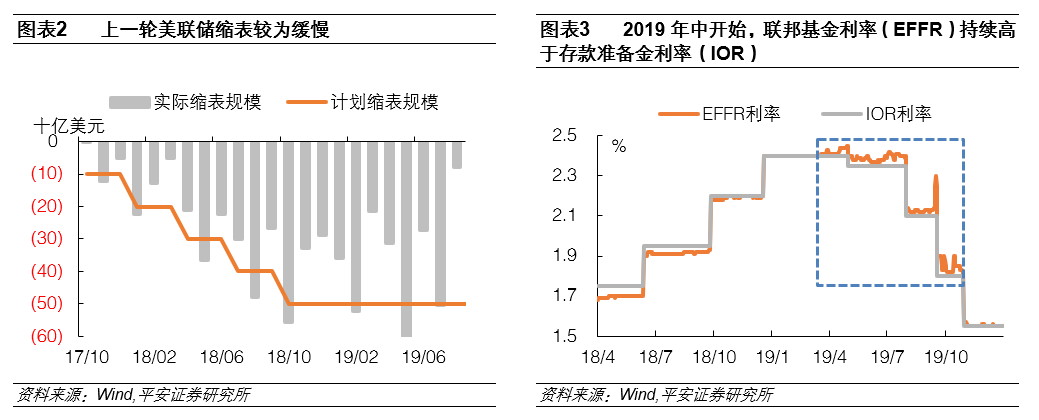

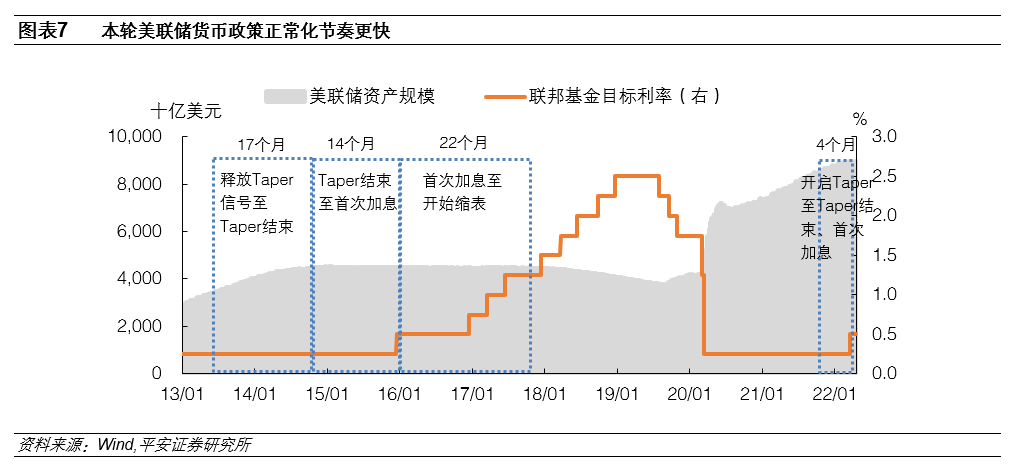

1)Due to the lack of effective reference, the Fed was more cautious in the last round of contraction, and the Fed was in no hurry to reduce its balance sheet on a large scale, from leading tightening to shrinking at a relatively slow pace.

2)In an effort to avoid simultaneous interest rate cuts and shrinking tables, and to ease liquidity shortages in financial markets, the Fed stopped shrinking ahead of schedule in August 2019, two months earlier than planned.

2)In an effort to avoid simultaneous interest rate cuts and shrinking tables, and to ease liquidity shortages in financial markets, the Fed stopped shrinking ahead of schedule in August 2019, two months earlier than planned.

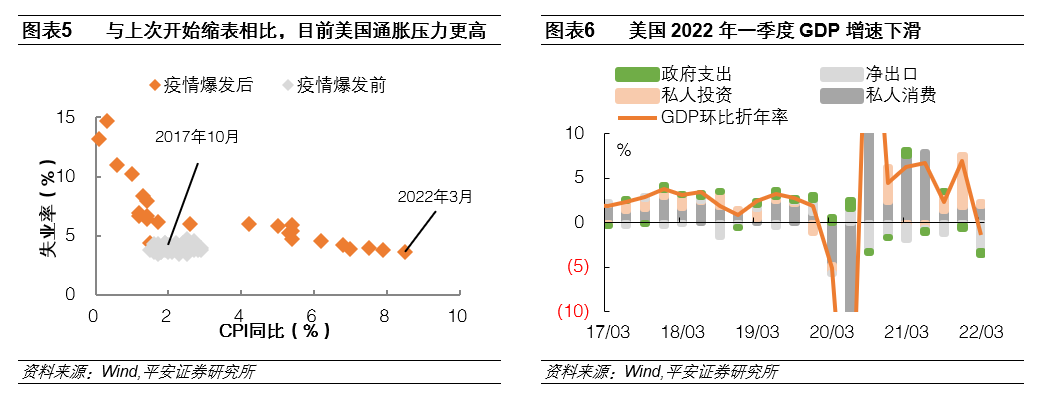

The macro context of the Fed's contraction this time is different, especially in terms of inflation.

The unemployment rate in the United States is lower but inflation is higher than in 2017. This determines that the purpose of the Fed's retrenchment is different from the past, and the pace is relatively faster. We estimate that the size of the Fed's balance sheet fell by about 15.7% in the 22-month period from October 2017 to August 2019. According to the Fed's shrinking plan, the Fed's balance sheet will fall by the same percentage in about 16-17 months (around October 2023).

Looking back, the Fed may show more flexibility in this contraction.

On the one handAt present, the employment situation in the United States is still relatively strong, and if inflationary pressures intensify, the Federal Reserve may accelerate its pace of contraction, just as it accelerated Taper in December 2021.On the other handConsidering that interest rate hikes and shrinking tables are alternative to some extent. If inflationary pressures ease in the United States, the Fed is also likely to slow its pace of contraction in order to avoid a "hard landing".

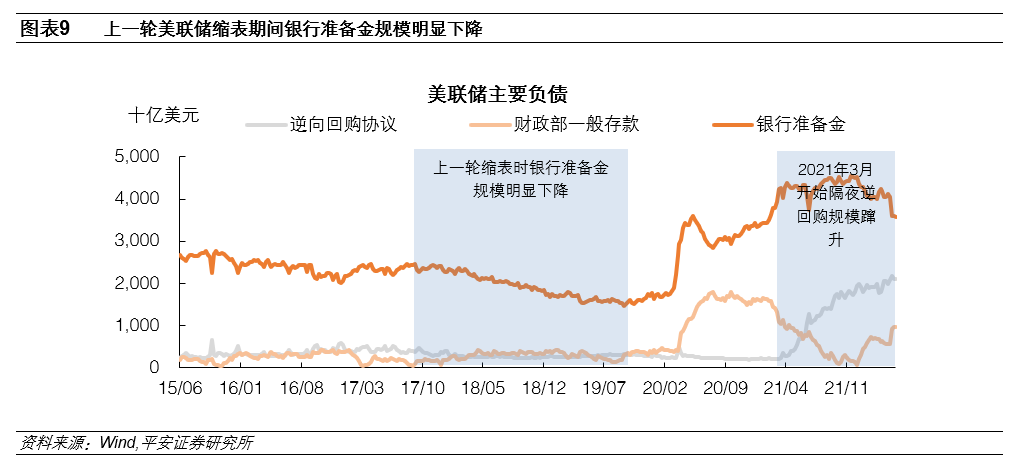

At present, great changes have taken place in the balance sheet structure and policy tools of the Federal Reserve, especially the reverse repurchase agreement on the debt side and the obvious increase in the size and proportion of general deposits of the Ministry of Finance, which makes the disturbance of the shrinking table to liquidity relatively low.

First,From the asset side, the proportion of MBS with great uncertainty in scale change decreases, which reduces the uncertainty of the shrinking table.

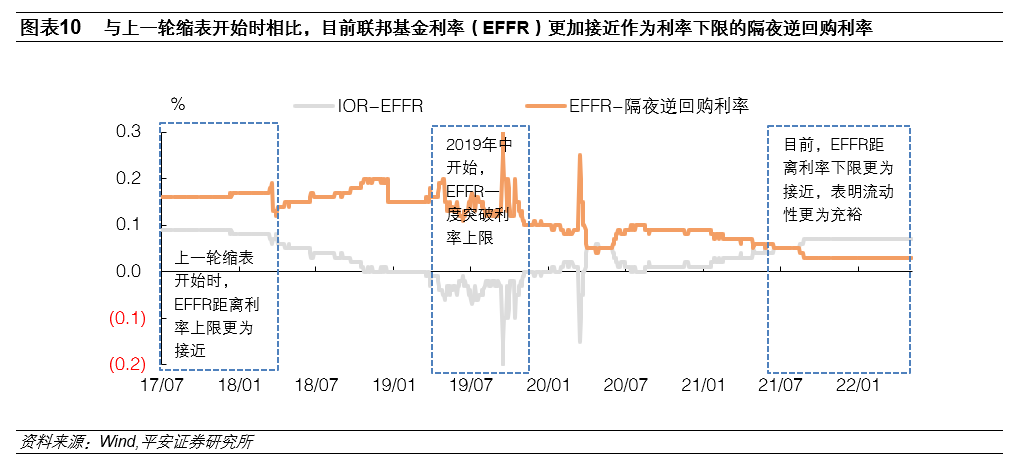

Second,The sharp rise in the size of reverse repurchase agreements and the fact that short-end interest rates are closer to the lower limit of interest rates means that market liquidity is more abundant than before the start of the last round of contraction, providing a thicker cushion for liquidity shocks.

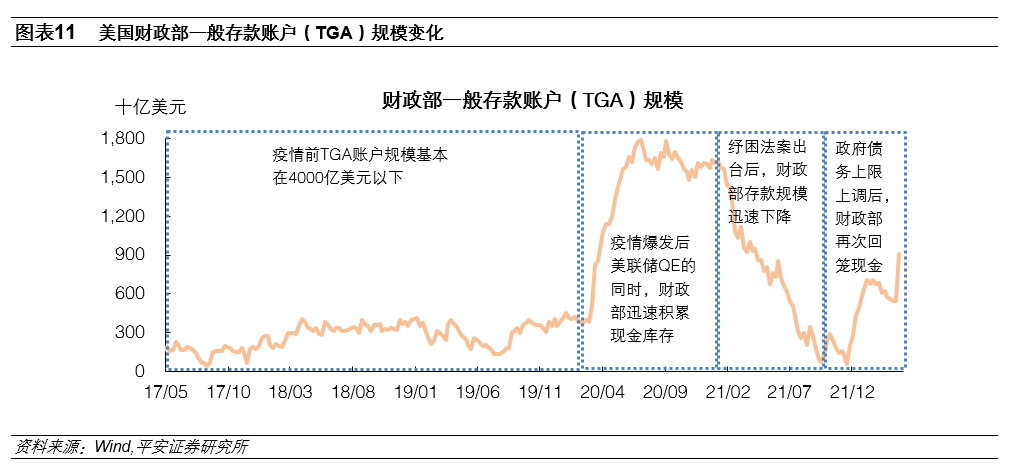

Third,With the gradual normalization of US fiscal policy, the general deposit size of the Treasury may slowly fall back to its pre-epidemic level in the second half of the year, thus releasing some liquidity to the market and mitigating the impact of the shrinking table.

Fourth,The introduction of standing repo facilities can provide liquidity under certain conditions, stabilize market confidence and reduce the probability of liquidity shortages.

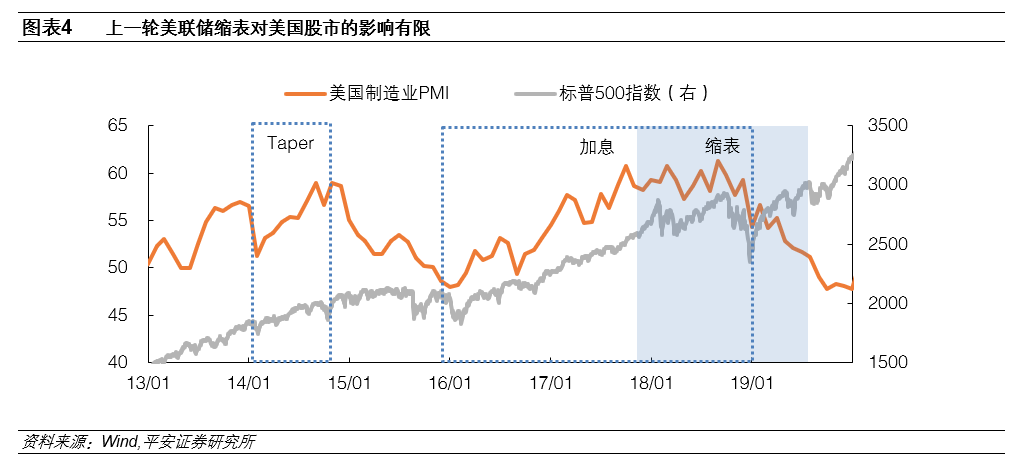

It should be noted that although market liquidity may not be greatly disturbed at the initial stage of the contraction, the impact of the Fed's contraction on asset prices should not be underestimated.. Since the Fed's interest rate meeting in May, 10-year Treasury yields have risen above 3% at one point, especially the return of real interest rates from-0.90% on March 1 to 0.34% on May 10, reflecting the further impact of the market taking into account the deflation table. The rise in interest rates on US debt has become an important catalyst for the adjustment of US stocks.

Edit / irisz