Source: clear written conversation

Author: Mingming Bond Research team

Core viewpoints

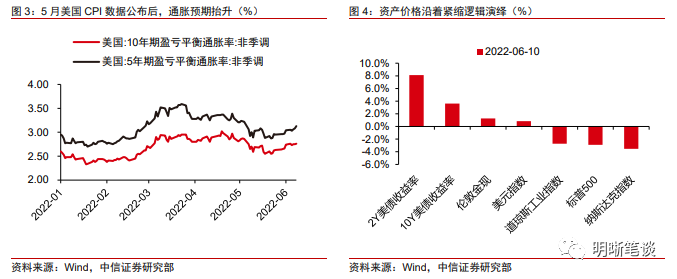

With the "fresh release" of US inflation data in May, market expectations of inflation peaking were dashed, and rising tightening expectations pushed asset prices to follow the tightening logic.

Looking ahead to the second half of the year, commodity price hubs are likely to remain high, making it difficult for global inflation to fall back quickly.

The US economy is on a downward trend and implies a multi-tiered recession risk, but there is little chance of a hard landing this year, and the market is still repricing the Fed's path to raise interest rates in July and beyond. Crude oil prices are expected to remain high throughout the year; US stocks are facing valuation and profit pressure, and the main trading logic may switch back and forth around the expectations of austerity and recession; the upside risk of US bond yields is still high, and the front high of 3.2 per cent is the key point in the short term; the US dollar index still has an upward risk in the short term, and the expectation of a US recession in the second half of the year is the main downside risk. Poor expectations of the strength of the US economy may be the key to affecting the price of gold.

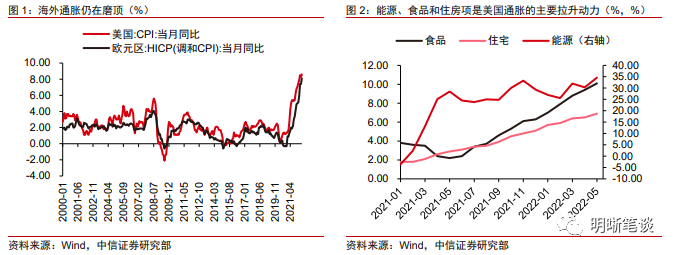

Global inflation is still at its peak.

In May, inflation data in both the US and Europe surpassed market expectations, dashing expectations that inflation would peak and fall. In terms of readings, the eurozone's harmonized CPI in May continued to rise from a year earlier, with an initial value of 8.1 per cent, higher than market expectations of 7.8 per cent, while US CPI also hit an all-time high of 8.6 per cent in May from a year earlier, well ahead of market expectations of 8.2 per cent. Itemized, inflation is spreading to a wider range.

Inflation expectations push up tightening expectations, and asset prices follow the tightening logic: major US stock indexes have fallen significantly, with the Nasdaq index represented by growth stocks and technology stocks falling by 3.5%; Treasury yields have risen in all maturities. short-end interest rates rose more significantly; the dollar index returned to the high of 104, and the price of gold rose slightly.

Prospect of overseas Macro situation in the second half of the year

Commodity price hubs may remain high

In terms of the conflict between Russia and Ukraine, the impact of the panic caused by the war on the market has been watered down, but the disturbance from factors such as supply chain, sanctions against Russia and anti-sanctions against Russia may continue into the second half of the year, and the commodity price center may remain high.

A downward trend in the US economy has emerged and implies the risk of a multi-tiered recession, but there is little chance of a hard landing this year.

Specifically, the US labor market is growing steadily, and the "wage-price" spiral remains the main risk.

Good household balance sheet, income growth and the arrival of traditional holidays at the end of the year may support the resilience of American personal consumption, but in the follow-up, we should also pay attention to the pressure on household consumption caused by persistently high inflation and the wealth contraction effect of falling stock market.

Both corporate and real estate investment have entered the downward channel, but the growth rate is still not low, and its support to the economy will not suddenly stall.

The stronger the tightening expectations, the worse the market expectations for the Fed's monetary policy in the fourth quarter.

On the monetary policy front, the inflation data that burst in May catalyzed tightening expectations in the market, which is still repricing the Fed's path to raise interest rates in July and beyond. The release of higher-than-expected inflation data on June 10 further catalysed market expectations of raising interest rates. According to the FedWatch, the probability of the Fed raising interest rates 25bps in September fell to zero, while the probability of raising interest rates 50bps or even 75bps was significantly higher than before.

How does inflation anxiety affect large categories of overseas assets?

1. Crude oil:Short-term supply and demand gap is difficult to fill, long-term attention to economic recession signals, crude oil prices may remain high throughout the year, the Iranian nuclear issue and the completion of OPEC+ 's production plan will still be the two major uncertainties in the crude oil market.

(2) US stocks:Valuation and earnings pressures persist, and the main trading logic may switch back and forth around expectations of tightening and recession, with overall volatility rising. In the face of inflationary anxiety and the expectation that the Federal Reserve will continue to raise interest rates by 50bps, US stocks are still under great pressure in the third quarter.

(2) US stocks:Valuation and earnings pressures persist, and the main trading logic may switch back and forth around expectations of tightening and recession, with overall volatility rising. In the face of inflationary anxiety and the expectation that the Federal Reserve will continue to raise interest rates by 50bps, US stocks are still under great pressure in the third quarter.

(3) U.S. Debt:The upside risk of US bond yield is still high, and the front high of 3.2% is the key point in the short term. Pay attention to the statement of this week's Fed interest rate meeting.

(IV) USD:Expectations of interest rate increases from the European Central Bank and the Federal Reserve have not been settled, the dollar index is difficult to say inflection point, there are still short-term upside risks, and the expectation of a US recession in the second half of the year is the main downside risk. For the RMB, the dollar index will rise again in the short term or put pressure on the RMB in the short term, but domestic economic fundamentals are still the key factor in determining the RMB exchange rate in the medium to long term.

(5) Gold:In the short term, high inflation and a strong dollar may keep gold volatile during the Fed's tightening repricing process. In the medium to long term, the key expectation difference affecting gold prices may be whether the speed and magnitude of the US economic downturn can significantly exceed market expectations.

Risk factors:Overseas inflation continued to worsen and monetary policy in major overseas economies exceeded expectations.

Edit / irisz