Original title: CICC | Hong Kong stocks: external fluctuations in Hong Kong stocks show resilience

Author: Wang Hanfeng, Liu Gang, etc.

Source: CICC strategy

Abstract

Although risk aversion hung over global stock markets last week and US stocks continued to be volatile, overseas Chinese stock markets still showed rare resilience. Positive policies continued to stack economic data to improve the overseas Chinese stock market continued to strengthen last week, especially the Hang Seng Technology Index rose 9.75% on the marginal improvement of the regulatory environment. The overseas Chinese stock market has continued to rebound since mid-May, with the MSCI China index rising more than 17 per cent, with technology growth stocks leading the way in anticipation of a marginal improvement in the regulatory environment.

look forward,We believe that a relaxed regulatory stance and still attractive valuations will continue to support the market. In addition to policy factors, economic data also played a positive role in the recovery of epidemic prevention and control measures last month.

However, in the process of repair, we still need to alert investors to potential volatility due to profit-taking, external market volatility and poor market expectations (the actual repair of growth and corporate earnings).

Looking forward, we believe that the core contradiction that investors are concerned about may turn to whether policy measures can have a practical effect. In the early stages of a market rally, valuations and sentiment tend to be the first to repair, while a bottoming rebound in the macro environment and earnings is a key factor in the market's continued rise.

Taken together, although the market turmoil caused by policy tightening and economic recession in the external market may still be the main source of volatility in the overseas Chinese stock market, we expect that the Hong Kong stock market is still expected to show considerable resilience, mainly due to the support of more positive policies, more attractive valuations and the continued inflow of southbound capital.

In other words, while fluctuations may occur, they also provide better opportunities for intervention.

Text

Market Review:Positive policies continued to stack economic data to improve the overseas Chinese stock market continued to strengthen last week, especially the Hang Seng Technology Index rose 9.75% on the marginal improvement of the regulatory environment.

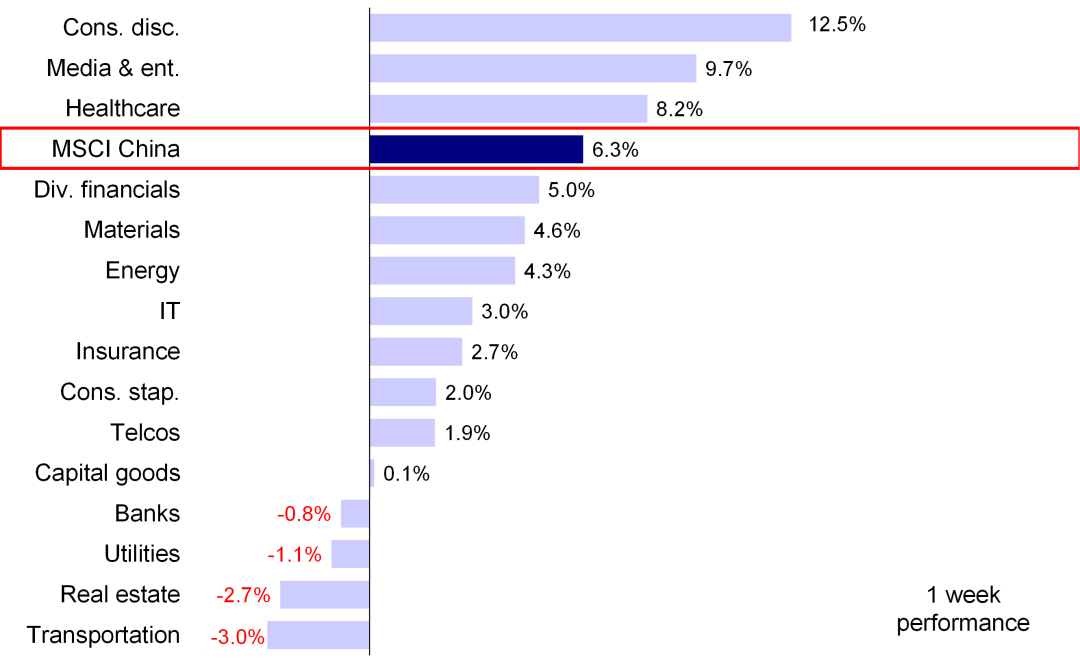

The MSCI China Index, the Hang Seng China Enterprises Index and the Hang Seng Index rose 6.3 per cent, 4.7 per cent and 3.4 per cent respectively.

In terms of the sector, the growth sector led the rise, with optional consumption, media entertainment and health care rising 12.5%, 9.7% and 8.2% respectively, while transportation, real estate and utilities lagged behind, falling 3.0%, 2.7% and 1.1%, respectively.

Chart: the MSCI China Index rose 6.3% last week, led by growth stocks.

Source: FactSet, China International Capital Corporation Research Department

Market outlook: since mid-may, the overseas Chinese stock market has continued to rebound, with the MSCI china index rising more than 17%, with technology growth stocks leading the way in anticipation of a marginal improvement in the regulatory environment.

Hong Kong Internet growth stocks, represented by the Hang Seng Technology Index, rose nearly 10 per cent last week, hitting a three-month high, and significantly outperformed A shares (up 4 per cent on the gem) and US counterparts (down 5.6 per cent on the Nasdaq).

In fact, since the Politburo meeting of the CPC Central Committee said at the end of April that it would increase policy support to deal with short-term macroeconomic challenges, specific policy measures to stabilize growth have been introduced one after another. Thanks to this, even in the environment of rising volatility in external markets, the previous pessimism in the Chinese stock market has been repaired by policy efforts.

At the end of May, the State Council issued a package of policies and measures to stabilize the economy, while 60 domestic online games were approved last week, the highest number since July 2021. Investor sentiment is expected to be boosted by the gradual normalization of the regulatory environment in the Internet sector, as can be seen from the large inflows attracted by the main Chinese ETF traded overseas.Looking forward, we believe that the marginal loosening of regulatory positions and still attractive valuations will continue to support the market.

In addition to policy factors, economic data also played a positive role in the recovery of epidemic prevention and control measures last month.After the epidemic eased, factories rushed to digest the backlog of orders, and May trade data were better than expected. Car sales grew by more than 50% month-on-month in May. In addition, financial data rebounded significantly in May from the April low. Overall, improved marginal economic activity and positive policies have boosted market sentiment and attracted the return of overseas capital, which in turn has contributed to the sharp rise of An and Hong Kong stocks over the past few weeks despite the turmoil in external markets.

However, in the process of repair, we still need to alert investors to potential volatility due to profit-taking, external market volatility and poor market expectations (the actual repair of growth and corporate earnings).

Although the policy of stabilizing growth is being carried out, the downward pressure on economic growth cannot be ignored. For example, there is still downward pressure on China's real estate industry and more policy support is needed. The May CPI data and loan structure remain weak, suggesting that policy needs to further boost aggregate demand. Looking forward, we believe that the core contradiction that investors are concerned about may turn to whether policy measures can have a practical effect. In the early stages of a market rally, valuations and sentiment tend to be the first to repair, while a bottoming rebound in the macro environment and earnings is a key factor in the market's continued rise.

In addition, some current risk factors are also worth paying attention to, such as the possible recurrence of the epidemic, the possible approval of the relevant bill by the United States to accelerate the delisting of Chinese stocks from the US market, and the faster-than-expected monetary tightening by overseas central banks. Externally, CPI in the United States rose faster than expected in May, which may further aggravate the pace and intensity of Fed tightening. A sharp rise in Treasury yields, a significant appreciation of the dollar and a sharp fall in the US stock market do not rule out further volatility.

On the whole, although the market turmoil caused by policy tightening in the peripheral markets and economic recession may still be the main source of fluctuations in the overseas Chinese stock market, weThe Hong Kong stock market is still expected to show considerable resilience.It is mainly supported by more positive policies, more attractive valuations and the continued inflow of southbound funds.

In other words, while fluctuations may occur, they also provide better opportunities for intervention. Variables worthy of close attention in the future include:

1) the change of epidemic situation and its impact on supply chain.

2) the landing of follow-up policies

3) volatility of US stock market, US yield and US dollar exchange rate

4) the trend of Sino-US relations and regulatory cooperation. Specific to the plate allocation, we believe that the target of high dividend yield and high-quality growth stocks will provide more protection for investors in the current market fluctuations. If more policies are introduced in the future, the benefits of stable growth are also worthy of attention.

Specifically, the main logic that underpins our point of view and the factors we need to pay attention to last week include:

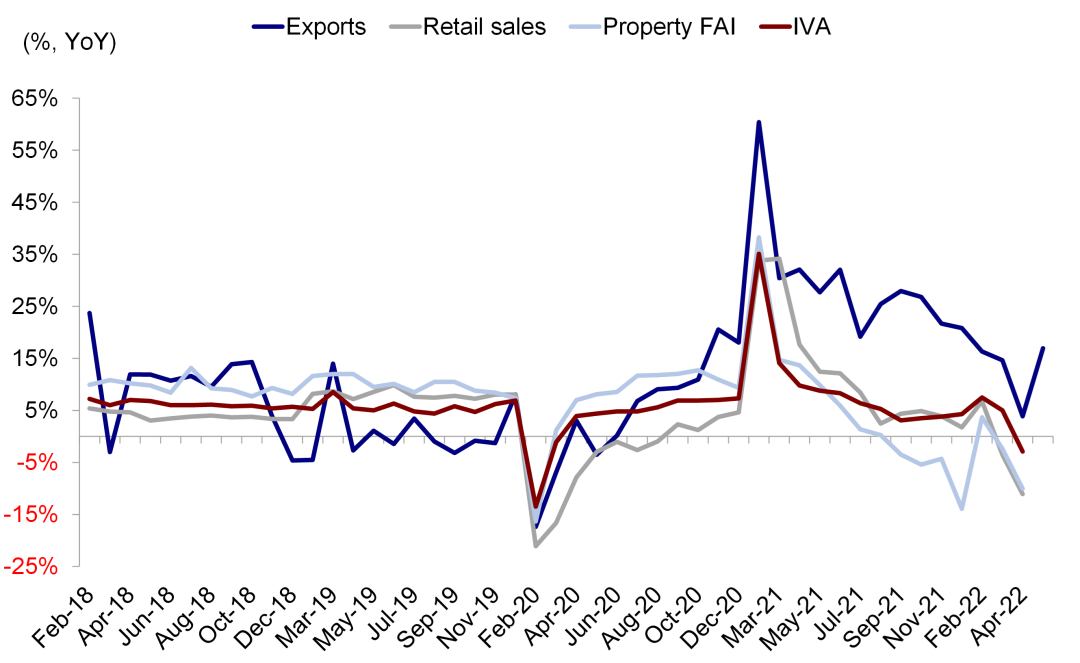

1) the rush to work after the epidemic led to a significant rebound in China's exports in May.Specifically, China's exports rose 16.9% in May from a year earlier, significantly faster than 3.9% in April, while imports rose 4.1% year-on-year, the same rate as in April, and both imports and exports exceeded market expectations. China's trade activity rebounded in May, mainly due to factories resuming work and production after the epidemic eased, speeding up the digestion of the April backlog of orders. However, it remains to be seen whether the strong external demand will decline in the future. As US consumers shift demand from goods to services, some large US retailers have said some goods are already in excess inventory. We believe that the slowdown in overseas growth may further weaken demand for Chinese goods.

Chart: epidemic prevention and control measures to ease the rebound in exports in May

Source: Wind, China International Capital Corporation Research

2) Financial data in May exceeded expectations, but demand in the real economy remained sluggish.On Friday, China released better-than-expected credit and financial data for May. Specifically, monetary easing continued to work, with M2 growth climbing to 11.1%, the highest since 2020. Thanks to increased government bond issuance, the year-on-year growth rate of social finance rebounded to 10.5 per cent in May from 10.3 per cent in April. However, although liquidity is relatively loose, the demand for credit in the real economy remains low. New RMB loans reached 1.89 trillion yuan in May, an increase of 390 billion yuan over the same period last year, but the new loans were mainly short-term financing rather than medium-and long-term loans to the real economy.

Chart: M2 and social finance grew faster than expected in May

Source: Wind, China International Capital Corporation Research Department

Chart: but demand for credit remains sluggish

Source: Wind, China International Capital Corporation Research Department

3) in May, CPI rose 2.1% from a year earlier. The gap between PPI and CPI scissors continued to narrow.Although overseas inflation has risen sharply, China's CPI rose by only 2.1% year-on-year in May, the same as in April, and easing supply constraints and weak demand recovery continue to dampen prices. Year-on-year PPI growth slowed to 6.4 per cent in May from 8 per cent in April, pushing the scissors gap between PPI and CPI to narrow sharply.

4) the approval of 60 domestic online games indicates that the regulatory level tends to be normalized.Last Tuesday, the State Press and publication Administration announced the approval of domestic online games in June 2022, with a total of 60 domestic new games approved, the largest since July 2021, up from 45 in April. The resumption of the approval of game version numbers has prompted the market to rekindle optimistic expectations that regulatory pressure on domestic Internet platforms is expected to gradually normalize.

5) the pace of southward capital inflows has accelerated, and the scale of overseas capital outflows has narrowed.Last week, mainland investors accelerated their purchases of Hong Kong stocks, with southbound capital inflows averaging HK $1.4 billion a day, up from HK $600m the previous week. Meanwhile, data from EPFR showed that overseas capital outflows from the Hong Kong market fell sharply to $38 million last week (as of Wednesday). Among them, active funds turned into net inflows last week after four consecutive weeks of outflows.

Chart: southbound capital inflows continue to be strong

Source: Wande Information, EPFR, China International Capital Corporation Research Department is narrow

Chart: the scale of overseas capital outflows narrowed last week

Source: Wande Information, EPFR, China International Capital Corporation Research Department

Investment建议:We believe that recent policy signals are expected to provide some support to the market, but a sustained rebound in the market still requires more substantive policy measures.We judge that opportunities outweigh risks in the medium term.

On the sector side, we believe that high dividend targets and low valuation targets, such as some financial, telecommunications and energy sectors, will provide investors with more protection from the current market volatility. At the same time, we recommend that we focus on the high-quality growth stocks that have fallen a lot in the previous period. In addition, with the easing of the epidemic in Hong Kong, the targets of local consumption and finance in Hong Kong are also worthy of attention.

Key pass注事件:1) China's economic growth and policy changes; 2) geopolitical tensions in Europe; 3) epidemic changes; 4) Sino-US relations.

Edit / irisz