Authors: Xiong Yuan, Liu Xinyu

Source: bear Garden observation

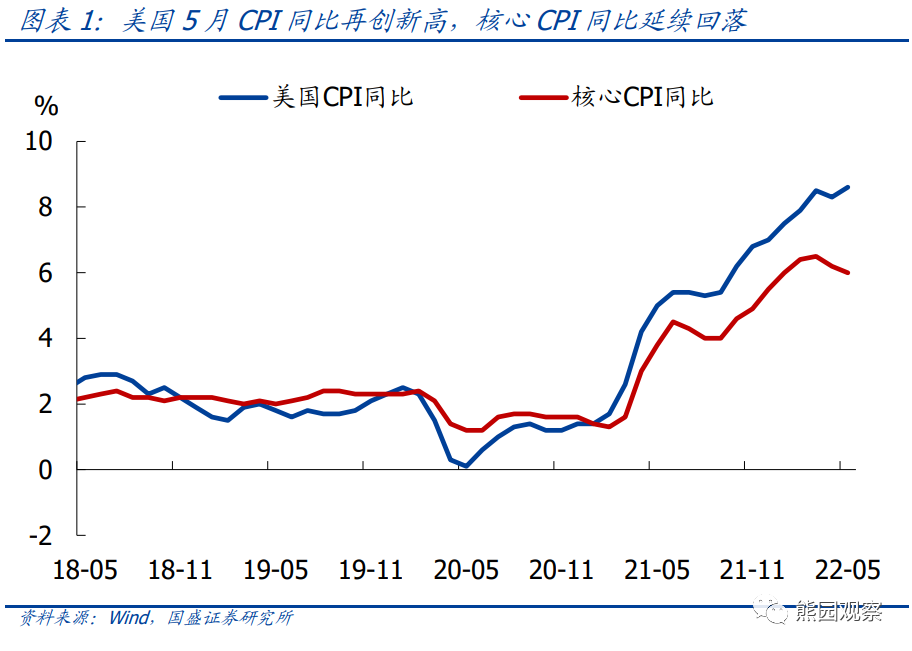

Events:In the United States, CPI in May was 8.6% year-on-year, with an expected and previous value of 8.3%.

Core conclusion:CPI in the United States hit a 40-year high in May, and the market basically made a "collective miscalculation", mainly due to the escalation of the conflict between Russia and Ukraine. Affected by this, US stocks fell sharply, US bond yields rose, and the Fed's expectation of raising interest rates rose sharply. Subsequent US inflation expectations have risen again and are expected to remain high in the third quarter. In the short term: the Fed's interest rate meeting on June 15 will most likely increase 50bp, focusing on the updated path of raising interest rates, especially the possibility of increasing 75bp in July and September; in addition, we still need to be wary of global stagflation and short-term adjustment pressure on US debt and US stocks, and the conflict between Russia and Ukraine is still a big disturbance.

1. CPI in the United States hit a new high in May compared with the same period last year, mainly due to the escalation of the conflict between Russia and Ukraine, which led to a sharp rise in energy prices; the core CPI continued to fall from the same period last year, but still as high as 6 per cent.

2. After the release of the data last night (6.10), US stocks fell sharply, US bond yields rose, and the Fed's expectations of raising interest rates rose sharply.

3. Looking back, inflation expectations have risen again. Us inflation is expected to remain high in the third quarter and fall in the fourth quarter, but the overall decline may be limited.

4. In the short term, focus on three major points:

When the Federal Reserve holds an interest rate meeting on June 15, it is likely to raise interest rates by 50bp, focusing on the updated path of raising interest rates, especially the possibility of increasing 75bp in July and September.

We still need to be on guard against global stagflation, and continue to suggest that during the year, the United States is closer to "stagflation without stagnation", China is closer to "stagnation but not stagflation", and Europe is already "stagflation".

In the short term, the adjustment pressure on US bonds and US stocks will become greater, and historical experience shows that A-shares will also be under pressure.

The text is as follows:

1. In May, CPI in the United States exceeded expectations and reached a new high, mainly due to the escalation of the conflict between Russia and Ukraine.

> overall performance: the US unseasonally adjusted CPI in May was 8.6% year-on-year, higher than the expected value and the previous value of 8.3%, and higher than the March high of 8.5%, once again refreshing a 40-year high; non-quarterly core CPI was 6.0% year on year, slightly higher than the expected value of 5.9%, but lower than the previous value of 6.2%, falling for the second month in a row.

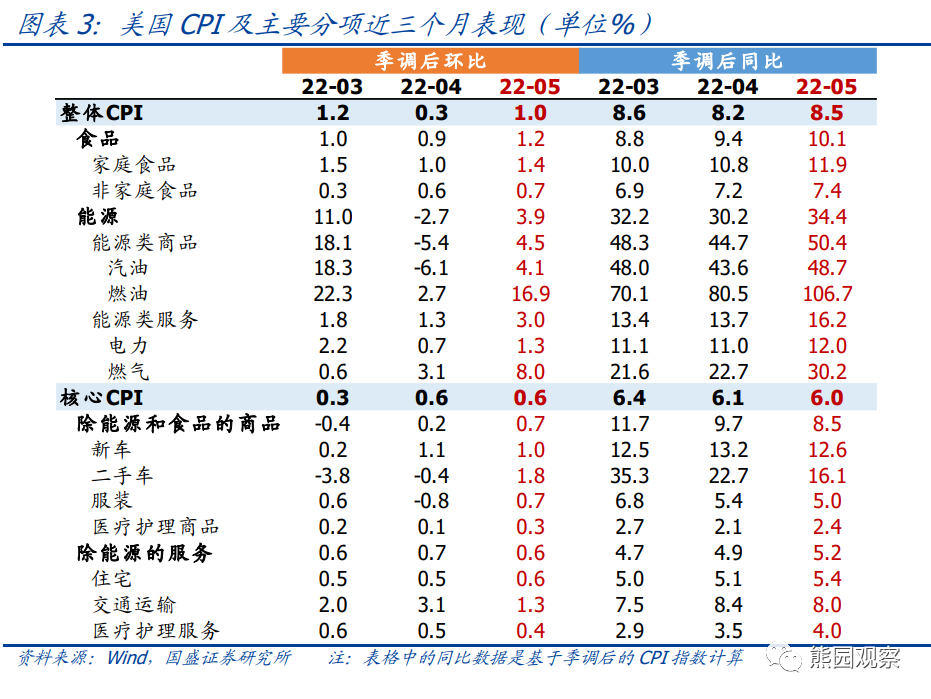

> Sub-performance: among the main CPI items in the United States, food and energy prices in May were 10.1% and 34.4% respectively compared with the same period last month, both rising sharply compared with the previous month, mainly due to the escalation of the conflict between Russia and Ukraine. Since April 25, Brent crude oil, NYMEX natural gas and CRB food index rose 20.3%, 32.0% and 2.5% respectively, which exceeded expectations, which also led to the market's collective miscalculation of this month's CPI.

In other categories, commodity prices excluding energy and food prices have fallen for three months in a row, and it is also the first time since April last year that the overall CPI has been lower than the same period last year. Previously, the largest increase in used cars continued to fall sharply compared with the same period last year; the service segment continued to rise slightly compared with the same period last year, with transportation falling slightly and housing rising faster.

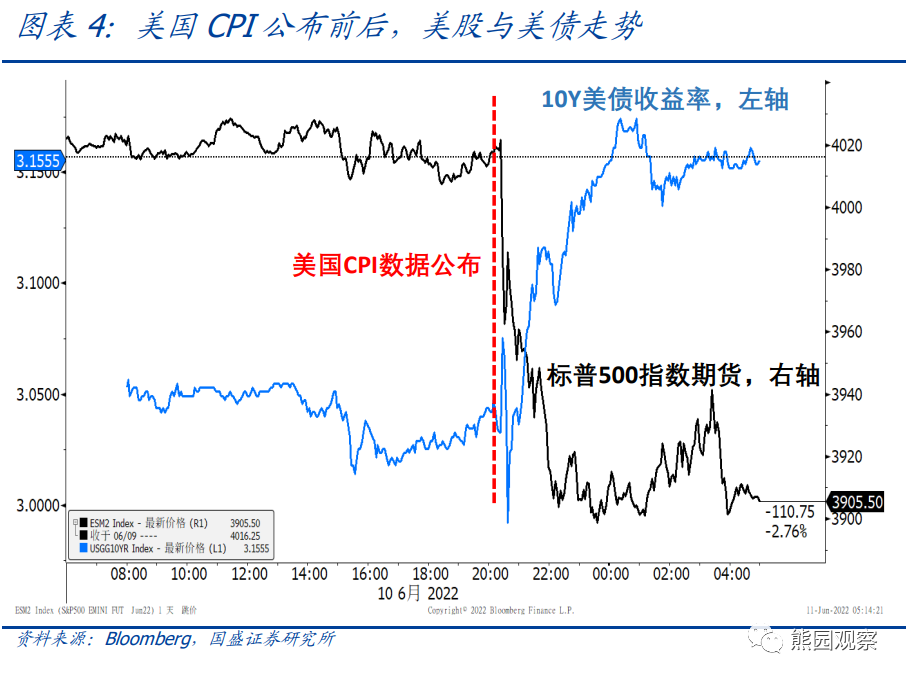

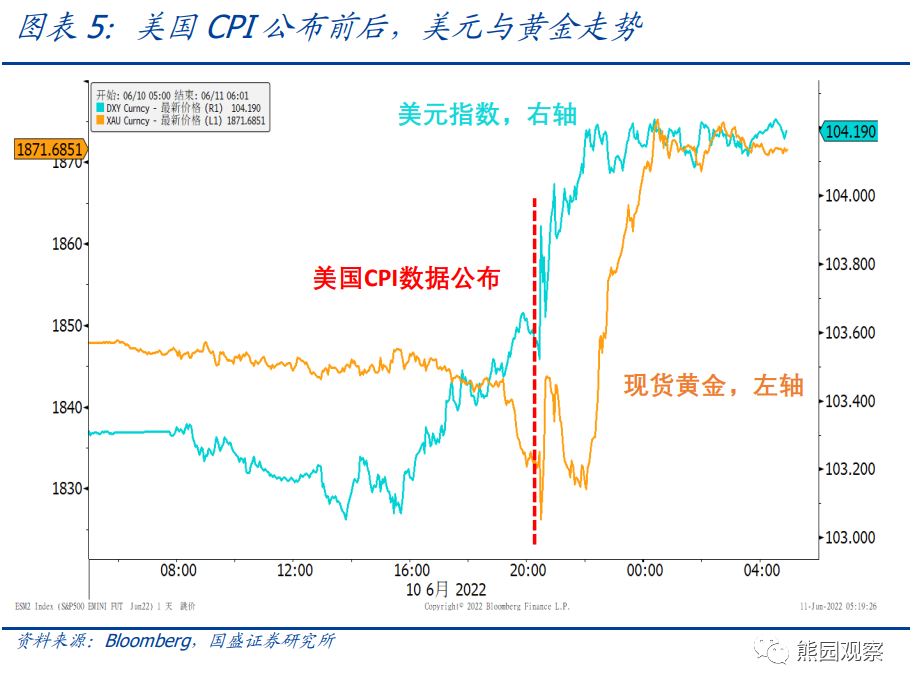

2. After the release of the data, US stocks fell sharply, US bond yields rose, and the Fed's expectation of raising interest rates rose sharply.

Performance of large categories of assets: after the release of US May CPI data last night, US bond yields, dollar index and gold prices all rose rapidly, S & P 500 index futures plunged rapidly, and the three major US stock indexes all opened sharply lower.

By the close, 10-year Treasury yields were up 11bp to 3.16 per cent, the dollar index rose 0.9 per cent to 104.2, spot gold rose 1.2 per cent to $1875 an ounce, and the S & P 500, Dow Jones and NASDAQ closed down 2.9 per cent, 2.7 per cent and 3.5 per cent, respectively.

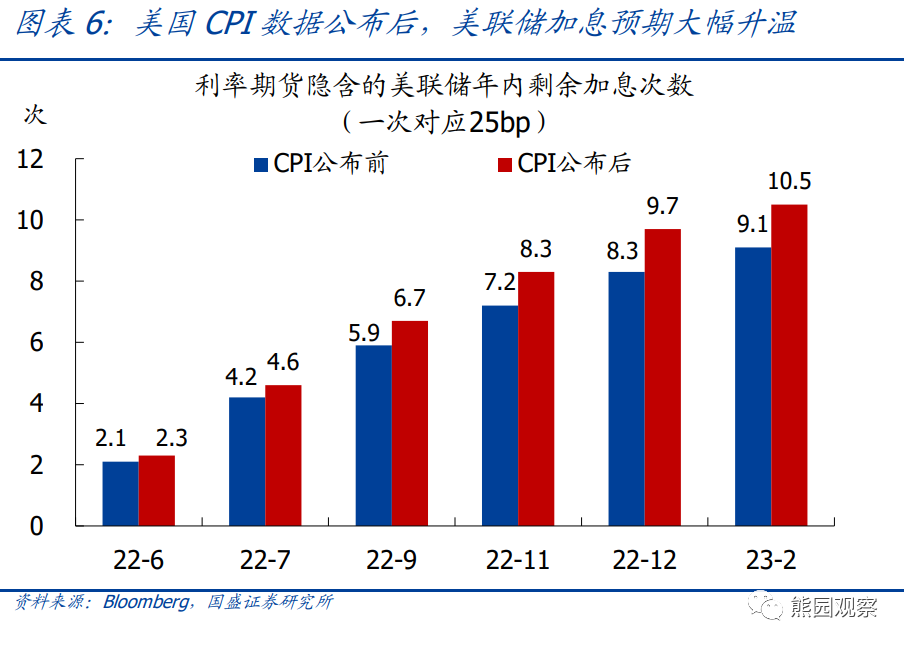

> expected changes in interest rate increases: before the release of CPI data, interest rate futures implied that interest rate futures would increase 50bp in June and July respectively. There is a more than half probability that interest rate increases will be increased in September. The remaining number of interest rate increases during the year is 8.3 times (each 25bp).

After the release of the CPI, the interest rate futures data changed to June plus 50bp, which is likely to increase in July and September, and the number of rate increases for the rest of the year rose to 9.7, reflecting a sharp rise in interest rate expectations.

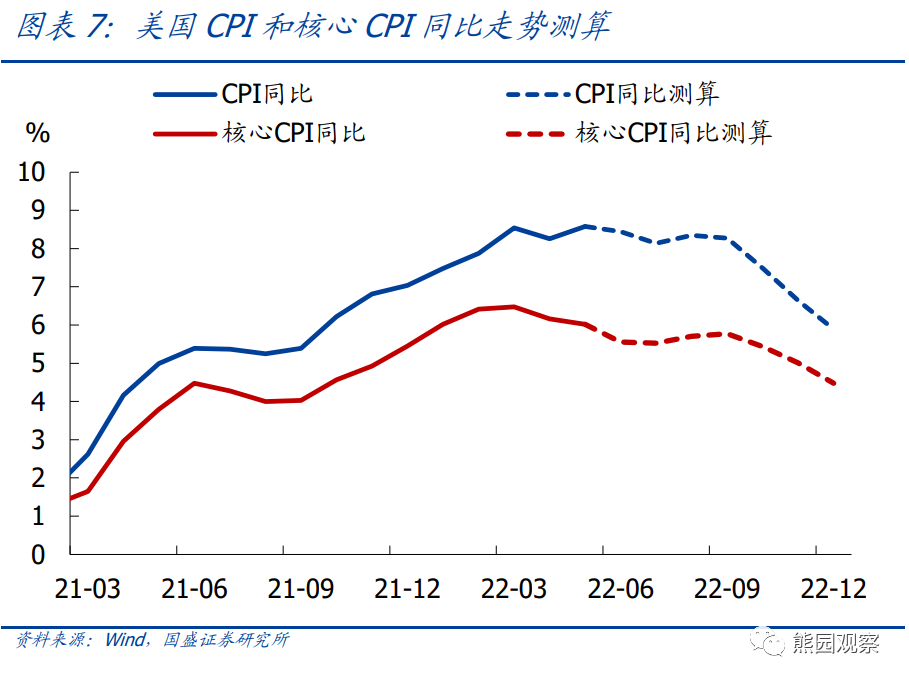

3. Looking back, US inflation will remain high in the third quarter, pointing to a further increase in the risk of global stagflation; if we keep a close eye on the path of raising interest rates after the 6.15 Fed meeting in the short term, we should also be wary of the risks of US bonds and US stocks.

Outlook for US inflation: in the previous report, we pointed out many times that US inflation basically follows the principle of "energy determines the direction, and other items determine the range."

In a neutral scenario, energy prices will remain high in the short term affected by the conflict between Russia and Ukraine, but in the medium to long term, due to the global economic slowdown and the fading of the conflict between Russia and Ukraine, energy prices will tend to fall; at the same time, with the slowdown in consumer demand, global supply chain repair and other factors, core inflationary pressure will gradually ease.

Based on this, it is estimated that the US CPI from June to September may remain at a high range of 8.2 per cent, 8.6 per cent year-on-year, and will not fall significantly until after October, which is expected to be around 6 per cent by the end of the year; core CPI may rebound slightly in the third quarter from the same period last year, fall in the fourth quarter, and is expected to fall around 4.5 per cent by the end of the year.

As a result, the risk of global stagflation will be further highlighted, and we continue to suggest that during the year, the United States is closer to "stagflation without stagnation", China is closer to "stagflation without stagnation", and Europe is already "stagflation".

Outlook for Fed interest rate hikes: the Fed will hold a meeting to discuss interest rates on June 15, and there is a good chance that it will still raise interest rates by 50 bp, focusing on the follow-up path predicted by the latest bitmap of interest rate increases, especially the possibility of increasing 75bp in July and September.

It tends to think that, although inflation remains high, due to the pressure of economic slowdown, the probability of the Fed raising interest rates 75bp is not high at present, and it is more likely that the Fed will raise interest rates by 50bp in June, July and September, followed by 25bp or 50bp, and when to stop raising interest rates, depending on the situation.

Outlook for large categories of assets: after the release of the CPI data, market inflation expectations have risen again, superimposed by the Fed's expectation of raising interest rates, and US bond yields will remain high in the short term, which does not rule out the possibility that they will rise above their previous highs, which means that US stocks will still have adjustment pressure in the short term, while gold may have a phased market.

Historical experience shows that when US bond yields rise and US stocks fall, the pressure on A-share adjustment will also increase significantly.

Edit / irisz