Source: macro meditation on investment promotion

Author: Zhang Jingjing

Core viewpoints

一、The framework of "demand determines direction, supply affects elasticity" is not applicable to crude oil.

(一)Demand does not determine the direction of oil prices.

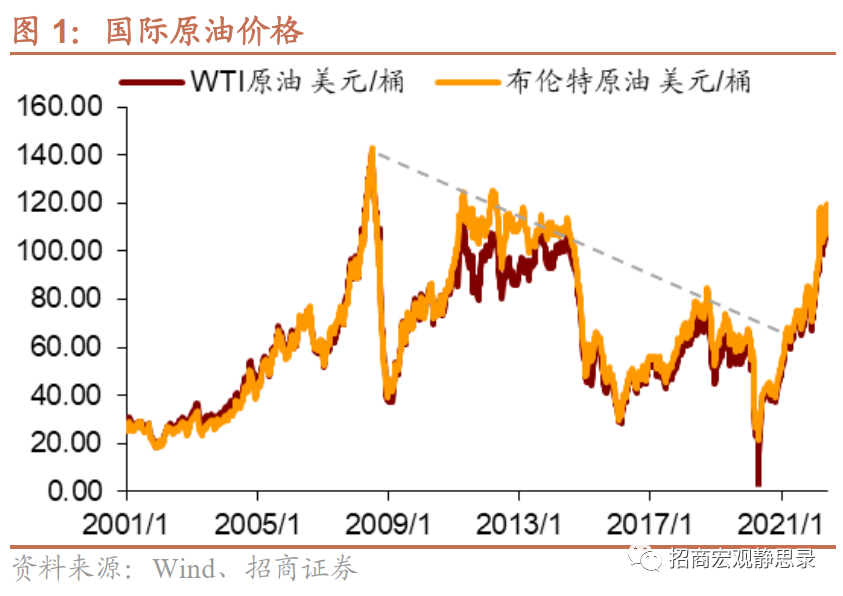

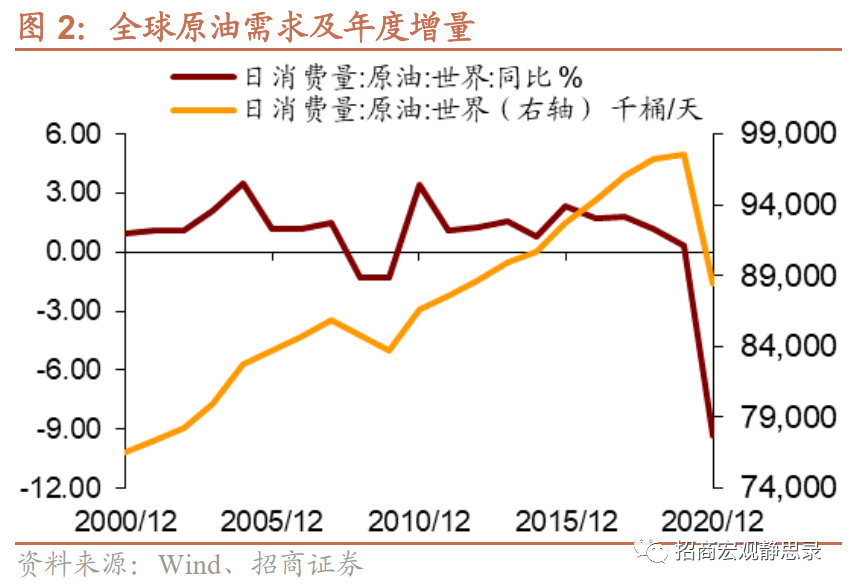

Oil prices have been falling from 2008 to before the epidemic, and crude oil has been in a bear market for 12 years. It is believed that many people will mistakenly think that crude oil demand is weak in the wake of the financial crisis, but the opposite is true. Crude oil demand grew at an average annual rate of 1.3 per cent in 2001-2008 and 1.6 per cent in 2010-2019.

(二)The transfer of pricing power and the improvement of marketization are the main reasons why crude oil has experienced a 12-year bear market.

The main cause of the crude oil bear market from 2008 to before the epidemic is the transfer of pricing power and the improvement of the degree of marketization.

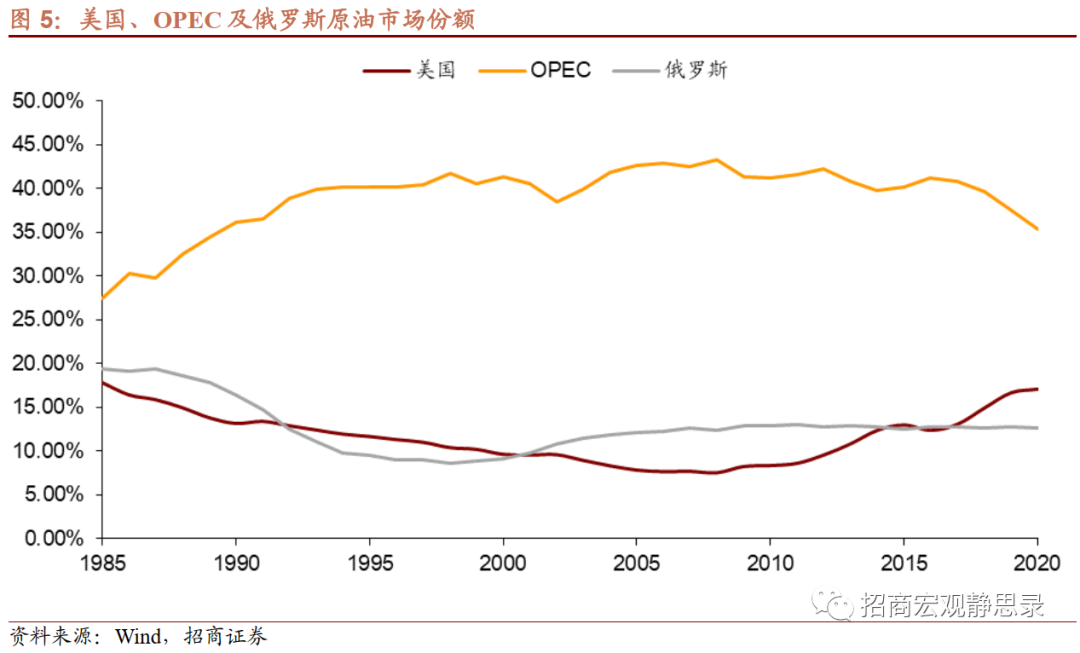

The United States has made great efforts to develop shale oil after the financial crisis. compared with traditional crude oil, American shale oil has three characteristics: shorter production cycle, more marketization, and technological progress driving the cost center down.

In turn, the United States gradually gained the pricing power of crude oil, and the bear market in the 12 years before the epidemic reflected the downward movement of shale oil costs.

(三)Supply and demand determine the direction of oil prices: the epidemic is the watershed of the bull-bear switch in crude oil prices; the bull market in crude oil is likely to last to 2025.Year or so

Supply and demand determine the direction of oil prices: the epidemic is a watershed switch between bulls and bears in crude oil prices; it is still in a bull market for a long time, but the risk of adjustment increases in the next 3-12 months.After Biden took office, the United States opened the era of new energy development, and also imposed policy constraints on traditional energy. The replacement of traditional energy by new energy is not achieved overnight, and the demand for crude oil may peak in 2025. With the epidemic as a watershed, international crude oil has ushered in a bull market with rising marginal demand and supply marginal contraction resonance, and the bull market logic will probably last until around 2025. But this is long-term logic. In terms of the medium-and short-term trend of crude oil, we need to pay more attention to two points: one is the marginal change in supply and demand, and the other is the "valuation" of crude oil reflected by inventory and price.

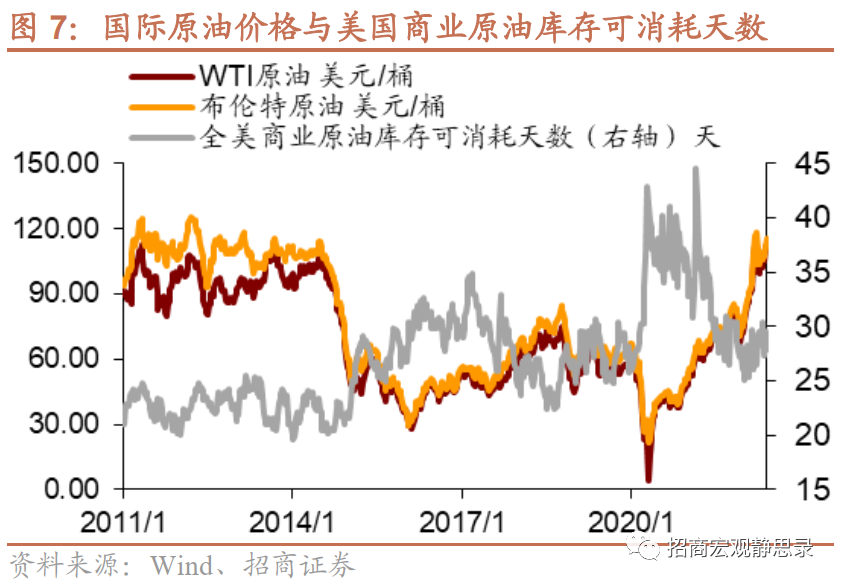

Second, is there a yardstick to measure oil prices? Inventory level

(一)Inventory level can be used as a yardstick to measure the price of crude oil.

Inventory levels show that the current "valuation" of oil prices is on the high side.Inventory level can be used as a yardstick to measure the price of crude oil. At present, US commercial crude oil inventories are still slightly higher than the 2018 low level, when the price of WTI crude oil was at a high of $75.10 / barrel and $85.00 / barrel, and as of June 3 this year, the price of WTI crude oil was $116.5 / barrel and $119.6 / barrel; the current consumption of crude oil in the United States is even equivalent to the 2019 level, when the average price of WTI crude oil is $57.20 / barrel and $64.20 / copper.

三、The current "valuation" of crude oil is a little high.

The current price of crude oil is significantly higher than the historical comparable stage, indicating that the "estimate" is too high, or includes the expectation of insufficient supply and a sharp rebound in global epidemic cooling travel demand.

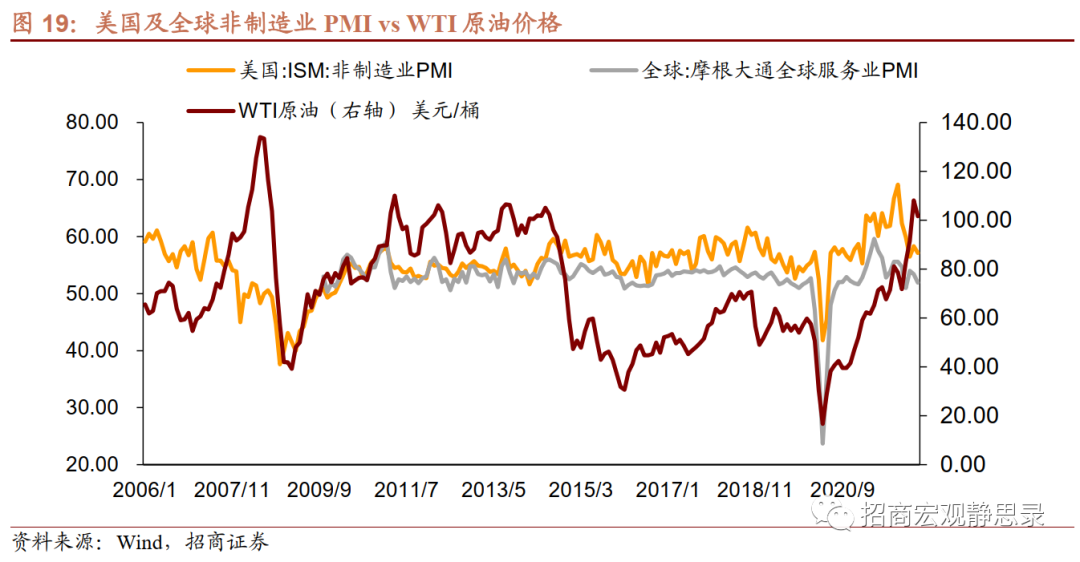

The operation of crude oil price since November 2020 is mainly driven by epidemic fluctuation and supply shock.

Sudden epidemic → oil prices fell sharply; epidemic cooling → oil prices rebounded; supply shock (expected) → oil prices will rise sharply; supply constraints cool → oil prices adjustment. In addition, the "buying and expected selling facts" in the international crude oil market after the epidemic have distinct characteristics.

The "long call" of crude oil may still be valid in the short term, but the "time value" is also declining.After a pulse boost such as overseas travel and the resumption of work and production in Shanghai, China, the contradiction on the demand side of crude oil may switch to weaker demand at some point in Q3. At that time, if there is no expectation or factual boost of supply shocks, then international crude oil prices will probably rise and fall. In addition, if the Iranian nuclear negotiations are reached, or if the situation between Russia and Ukraine improves, then oil prices may face greater pressure to adjust.

We should be on guard against the last rush of oil prices.

Crude oil prices do not necessarily turn into a downward trend in the early stages of weakening demand. In a state of excitement and uncrowded trading, the possibility of international oil prices pulsing upward again driven by sudden factors or short-term fundamental changes cannot be ruled out. Once that happens, risk appetite in the global market is also likely to tighten periodically and quickly, after which oil prices will fall sharply from high levels until demand picks up again.

Edit / irisz