Author: Guojun Gushi Qin Han, Liu Yi

The original title "the current stock market is the bond market at the beginning of the year"

Abstract: Guojun Gusheng Qin Han team believes that the current stock market expectations are highly consistent, investors are waiting for the index to fall below the previous low of 2638 before looking for opportunities to enter the market. Then the facts may go in the opposite direction, it may be difficult for the market to fall below the previous low, and the bottom of the market appears unwittingly.

The current stock market is the same as the bond market at the beginning of the year, and the continued decline in the market is the core reason for the continued decline in the market.However, under the unanimous bearish view of the market, the bottom of the market will appear unconsciously, and in the next stage, the market situation will switch to the pattern of strong stocks and weak debt, and the risks of the bond market are greater than the opportunities.

Buttocks determine the head, and there is a natural difference in economic expectations between stock and bond investors. Equity investors are born long in the economy, while bond investors are born short in the economy, which determines that even for the same factors, the economic expectations implied by the stock and bond markets may be very different.

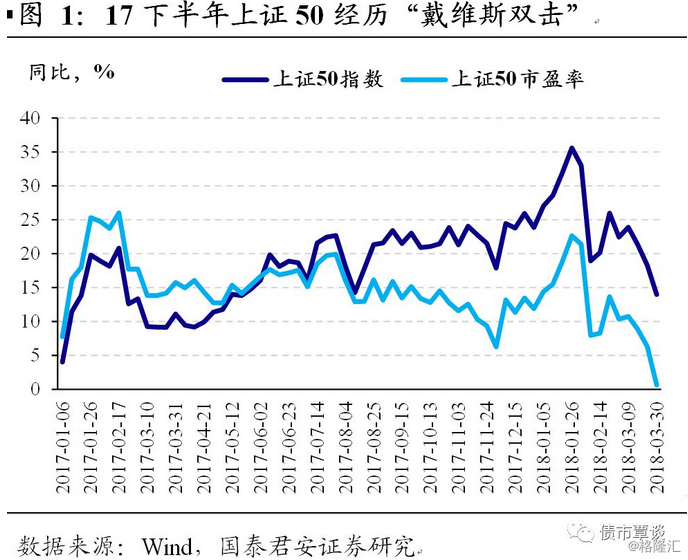

A typical case.In 17 years, the stock market and bond market can accurately reflect the difference between the two groups. In the past 16 years, there have been signs of macroeconomic stabilization. however, after 17 years, the expectations of bond investors and stock market investors have appeared obvious divergence. The judgment of bond market investors on the economy is mostly high in the front and low in the second, and the greatest opportunity for the bond market is in the fourth quarter. The main logic comes from the linear extrapolation of the economic downturn. On the other hand, stock market investors are relatively optimistic about the economy, and it is true from the point of view of the market. Blue-chip white horse stocks even saw a Davis double click in the second half of 17 years. The difference in economic expectations between these two types of markets finally ended in the way that the bond market converged to the stock market, at the cost of the collapse of the bond market in the fourth quarter of 17.

The recent expected performance of the stock and bond markets has been somewhat unusual. Since late July, a series of stable financing and economic policies have been issued at the policy level, including window banks to guide investment in low-rated credit bonds, relaxation of new financial regulations during the transition period, and more active fiscal policy setting. But this time, for the two main players of the stock and debt market, it does not continue the usual style that stock investors are more optimistic than bond market investors. on the contrary, bond market investors are more optimistic about the economy than stock market investors.

(1) long-end interest rates continue to adjust while credit debt improves significantly. Since late July, yields on tradable varieties such as 10-year government bonds and Guokai began to pick up, rising from lows to highs once close to 20bp. At the same time, the yields of low-rated credit bonds, which represent a high risk appetite in the bond market, have declined rapidly. This essentially reflects that under the stability maintenance policy, the overall risk appetite of the bond market is rebounding rapidly, and the expectations of bond market investors for the future economy are not particularly pessimistic.

(2) the expectation of the stock market for the economy is not as optimistic as the bond market. Looking back at the trend of the stock market since policy easing, the market seems to reflect that investors do not have much confidence in financing and economic stabilization. Since late July, the stock market has fallen below 2700 again from 2900 and hit 2653 at one point this week, less than 20 points below the pre-2638 low formed during the stock market crash. Although the Politburo meeting in the second quarter redefined the tone of deleveraging, the trade war was not optimistic, and fluctuations in emerging markets had a certain negative impact on the stock market, in the final analysis, the reason for the continued decline in the stock market is still the lack of investor confidence in future economic stabilization.

Looking back, we believe that this round of pessimism about economic expectations in the stock market is related to the market that has been falling since the beginning of the year, and is expected to be substantially repaired in the future. this round of differences in economic expectations between the stock and bond markets may end with the convergence of the stock market to the bond market.

From a market point of view, a reversal of consensus expectations is more likely.

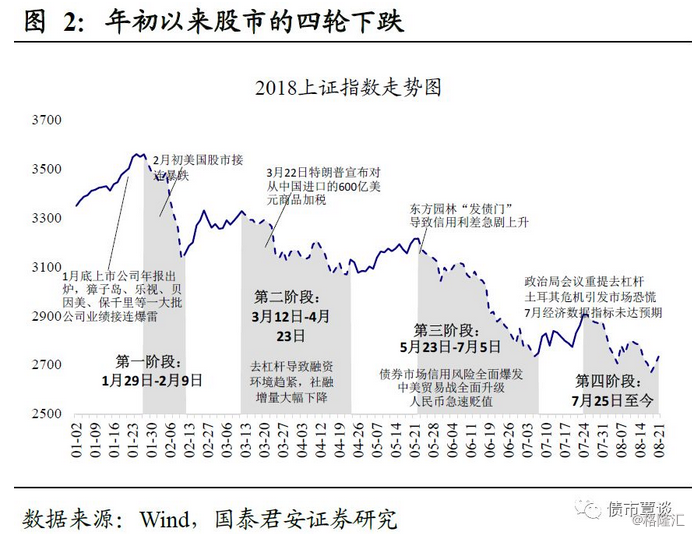

The four stages of the stock market decline since the beginning of the year. The decline of the stock market over the past 18 years can be roughly divided into four stages: (1) from the end of January to the beginning of February, the collapse of US stocks superimposed frequent performance mines of listed companies led to a sharp decline in the stock market; (2) from mid-March to late April, the initial signs of a trade war fermented superimposed financing contraction triggered the stock market to fall sharply after a small rebound. (3) from late May to July, credit events represented by "Oriental Garden" entered the eyes of investors, leading to a rapid decline in risk appetite and a decline in the market; (4) since late July, the Politburo meeting again mentioned that deleveraging led to less-than-expected policy easing and the Turkish crisis led to continuous stock market adjustments.

After continuing to fall sharply, the good news has become a story of "here comes the wolf".Since the beginning of the year, the stock market has fallen by nearly 25%. Although there have been periodic rallies in February, May and July, they all ended with a new negative rebound. The continued sharp fall in the stock market has caused heavy losses to all investors who try to do long or bottom. When the broad credit policy continues to hit the ground, it turns into a story of "wolf coming". The mentality of "would rather miss it" makes the stock market's expectations for the future economy more and more pessimistic.

The bond market at the beginning of 18 is a replica of the current stock market. Since the fourth quarter of 17 years, bond yields have continued to climb as a result of a series of negative releases, such as better-than-expected superimposed regulation and tighter regulation. In the process of rising yields throughout the fourth quarter, bulls kept bottoming out to stop losses. Finally, after the intensive release of a round of regulatory documents at the beginning of the Lunar New year, the 10-year Guokai station reached a high of 5.13%. In the process, all investors who tried to long bonds were badly hurt, so when yields were really at their highest point, everyone became extremely cautious. It is precisely because everyone is bearish, the overall position often falls to a very low position, from the trading marginal point of view, at this time no one can continue to short, the market will form a bottom, there will be a rise.

The current stock market expectations are highly consistent, so the facts may go in the opposite direction. After repeated defeats, bulls have higher and higher safety margins for long, which makes investors wait for the index to fall below the previous low of 2638 before looking for a chance to enter. This consensus bearish expectation is the same as that of the bond market at the beginning of the year, and the end result is that it may be difficult for the market to fall below the previous low.

From a fundamental point of view, the future opportunity of the stock market is significantly greater than that of the bond market.

(1) wide credit will take effect quickly. It is not difficult to find that the lag from broad money to broad credit is getting longer after comparing the three times of social integration in the history of 2008 (November 2008, June 12 and December 15). In particular, the stabilization of social finance in December 15 lagged behind the monetary policy for a full 20 months, and there are three main reasons: first, financial idling reduces the efficiency of funds entering the entity. Second, the physical operation situation deteriorates, and its own financing demand drops obviously; third, the principal contradiction in 14-16 years is internal, compared with the external contradictions in 2008 and 12 years, the strength of policy hedging will be relatively small.

Compared with history, this round of wide credit policy has the basis of quick effect: first, the financial idling has been basically eliminated in the process of deleveraging in 17 years, the stock of interbank financial management has been almost halved in 17 years, and the growth rate of M2 has begun to converge to nominal GDP; second, corporate profits have improved driven by supply-side reform, and the financing demand of entities is not weak, and the essence of this round of financing contraction is actually the contraction of financing supply caused by deleveraging policy. The last round of the 2008 financial crisis, like the 12-year European debt crisis, is also facing larger external contradictions, and the control of external contradictions is far less than internal contradictions, so the amount of policy advance is often more sufficient. This round of easing actually began before there were obvious signs of economic decline.

(2) from the point of view of the trade war, the game of the harvest of the enlightened continues. No matter from the experience of the trade war between the United States and Japan, or from the current situation between China and the United States, it is unlikely that the trade war will end quickly in the short term, which means that for the stock market, the trade war may become a negative factor that suppresses valuations for a long time. But for transactional varieties, expectations are always ahead of time. At a time when investors have fully responded to the repeated pessimistic expectations of the trade war, the marginal change of the situation is the more critical factor affecting the trend.

At present, the Sino-US economic and trade issues have re-entered the consultation process, and the impact of the trade war will at least not worsen in the short term. from this point of view, this is the most important marginal change of the trade war factors to the stock market. Although from the perspective of monetary policy transmission, the policy shift may not mean that the credit risk will converge quickly in the short term, but for low-rated credit bonds, seeing the policy shift may be more important than the policy effect itself. The rush of epiphany makes the yield of low-rating credit bonds decline rapidly by 80-90bp. The same is true of the current stock market, according to previous experience, do not rule out the possibility of negotiations come to an end, but this does not affect the sustained rise of the stock market in the short term.

Generally speaking, we think that in the next stage, the market situation will switch to the pattern of strong stocks and weak debt, and the risks of the bond market outweigh the opportunities.