值得关注的是,这已经不是罗普金斯第一次高溢价关联收购了,在2020年公司就曾以1.93亿元现购买苏州中亿丰科技有限公司(以下简称“中亿丰科技”)80%股权,形成了1.43亿商誉。

值得关注的是,这已经不是罗普金斯第一次高溢价关联收购了,在2020年公司就曾以1.93亿元现购买苏州中亿丰科技有限公司(以下简称“中亿丰科技”)80%股权,形成了1.43亿商誉。

Product: Sina Finance listed Company Research Institute

Author: cici

On November 16th, Luopskin announced that the company intends to purchase 100% of the shares of Suzhou founder Engineering Technology Development and testing Co., Ltd. (hereinafter referred to as "founder Test") held by Zhongyifeng holding Group Co., Ltd. (hereinafter referred to as "founder Test"). The total transaction price is 89.1007 million yuan, and the other party, Zhongyifeng Holdings Group Co., Ltd. is a related party legal person, so this transaction constitutes a related transaction.

It is worth noting that this is not the first high premium related party acquisition by Lopkins. In 2020, the company bought an 80 per cent stake in Suzhou Zhongyifeng Technology Co., Ltd. (hereinafter referred to as "Zhongyifeng Technology") for 193 million yuan, forming a goodwill of 143 million.

It is worth noting that this is not the first high premium related party acquisition by Lopkins. In 2020, the company bought an 80 per cent stake in Suzhou Zhongyifeng Technology Co., Ltd. (hereinafter referred to as "Zhongyifeng Technology") for 193 million yuan, forming a goodwill of 143 million.

At the same time, in the asset evaluation report in which the intermediary is out, there are big errors in the determination of many key indicators of valuation, such as the β coefficient of the key index when determining the rate of return on equity, the determination of the growth rate of free cash flow after the stable period, and so on. Therefore, we have doubts about the accuracy of the final results of asset evaluation.

In addition, in terms of business coordination and strategic alignment, the business coordination of Lopkins and founder testing is poor, and the acquisition being tested by the other party is obviously not in line with its strategic plan. Can Lopkins' related party transaction acquisition be digested successfully to achieve the effect of 1: 1 > 2 without harming the interests of minority shareholders?

There are doubts about the accuracy of the asset evaluation report.

For the value evaluation of unlisted enterprises, there is nothing wrong with choosing the income method as the value evaluation method, but in the asset evaluation report of Vaughson's proposed acquisition of related party transactions for Ropskins, we found that in the determination of several key indicators, there is a lack of rigor, overestimating the value of the target of the transaction.

Suspect one: a growth rate of 3% after 2022 is too hasty.For the detailed forecast of the subsequent growth rate of enterprises, the company announced that because the annual output value of Suzhou construction industry grew by 7% year-on-year in 2020 and 3% annually after 2022.

We all know that after 2021, the fundamentals of the real estate and construction industries have changed. Therefore, using only the 2020 data to predict the growth rate after 2022 does not seem to be very convincing.

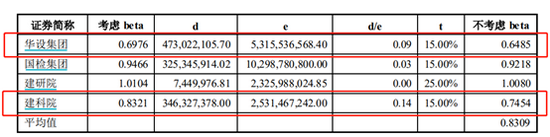

Doubtful point 2: the determination of β coefficient is inaccurate and can be lower than that of enterprises.The final evaluation value is seriously affected. The reference of the β coefficient of Huashi Group and the Academy of Construction Sciences is not great, and their β coefficient is low, which makes the net interest rate of equity underestimated, the discount rate underestimated, and the valuation on the high side.

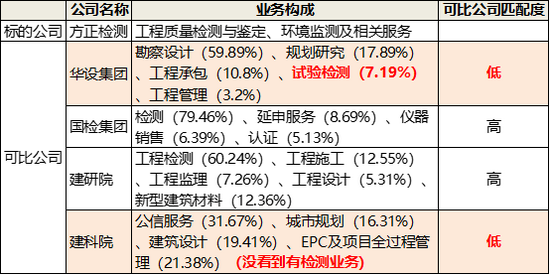

Founder's main business is engineering quality inspection and appraisal, environmental monitoring and related services. In the asset evaluation report, Waxson selected Huazhi Group, State Inspection Group, Construction and Research Institute and Academy of Construction Sciences as comparable listed companies, but did not give the basis for selecting comparable companies.

However, after looking at the composition of the main income of these four comparable listed companies, we find that there is a big difference between the main business and the target companies of Huashi Group and the Academy of Construction Sciences.

(source: Sina Finance)

(source: Sina Finance)

Among them, the revenue of Huashi Group's experimental testing business accounts for only 7.19%, and its main business is survey, design and planning research, which account for about 80% of the revenue; the testing business of the Academy of Construction Sciences accounts for even less. Its main business is public trust services, urban planning, architectural design, etc., accounting for about 80% of the main business.

(source: Sina Finance)

(source: Sina Finance)Through the asset evaluation report issued by Walkerson, we can also see that the value of β of Huashi Group and the Institute of Construction and Research is obviously lower than that of the State Inspection Group and the Institute of Construction and Research. We should know that the coefficient of β is the key index for calculating the rate of return on equity. It plays an important role in the valuation of enterprises, because it is mixed with more asset appraisers and supervisors to select comparable companies, β value ranges and other human controllable factors. It is also the index that is most likely to be arbitrarily modified.

Therefore, from the point of view of the selection of comparable companies, among the four companies selected by Volkson, the reference significance of Huashi Group and the Academy of Construction Sciences is not great, and it is unfair to be used to evaluate the key coefficient of β value.

In the asset evaluation report issued by the intermediary, the data of the asset method are listed in detail, but the key income method does not explain the calculation of FCFF and WACC in detail. in the public information, we find the above two doubts, which may seriously affect the accuracy of the valuation of the target company.

Target situation: poor business coordination, low matching degree of strategic planning

From the operational point of view, the cooperation between the main business of Lopskin and founder testing is poor, and the integration of manpower and management after the acquisition is more complex and not easy to "digest"; from the perspective of strategic planning, Lopskin's future strategic planning focuses on the aluminum industry chain and smart city layout, while founder testing obviously expects little relevance in strategic development. Below, we will focus on.

First of all, from the perspective of business composition, Lopskin's main business during the reporting period is mainly the research and development, design, production and sales of new aluminum alloy casting bar materials, aluminum alloy profiles, aluminum alloy system doors and windows; however, the main business of founder testing of the target company is engineering quality inspection, environmental monitoring and lightning protection system testing. As a result, Lopskin and founder detection of the main business cooperation is poor.

Because of the poor business coordination, after founder testing's acquisition, Lopskin will integrate the engineering quality inspection business in the later stage, or will pay more human resources, working capital, etc., thus unable to achieve synergy.

Secondly, from the perspective of strategic relevance, in the 2020 annual report, the development strategy put forward by Lopskin in the company's development strategy section is "carry out the transformation and upgrading of the aluminum industry, and devote itself to the extension and value promotion of the aluminum profile industry chain." gradually developed into an influential provider of system doors and windows, aluminum alloy profiles and solution service providers in the industry. At the same time, focus on the development of smart cities and be an expert in the service of smart cities in China. "

Generally speaking, the company's future development strategy mainly focuses on aluminum industry chain and smart city services, while founder testing's main business is engineering and environmental testing, it is obvious that the acquisition of the target founder testing is not in line with the development strategy.

Finally, from the point of view of the target quality, the testing industry where founder testing is located mainly presents the pattern of "big market and small companies", and the total market share of testing institutions with annual income of 10 million or more is only 13.11%. The downstream areas such as construction engineering testing, building materials testing and environmental monitoring show regionalization characteristics, while the business development of founder testing is mainly concentrated in Jiangsu Province.

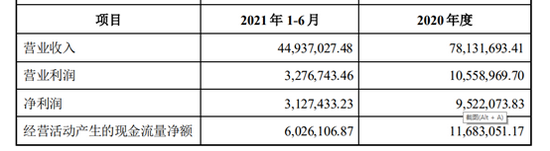

Construction engineering testing, building materials testing and environmental monitoring due to the capital threshold, technical threshold is low and other factors, the industry competition is more fierce. From January to June in 2021, founder's net profit was only 3.1274 million, which was only 32.84% (less than half) of the 2020 net profit.

(source: company announcement)

(source: company announcement)

Under the circumstances of the fundamental changes in the real estate industry and the intensification of competition in the real estate industry, founder tests whether it can achieve the audited annual deduction of non-net profit in 2022,2023 and 2024 (note: only the net profit tested by founder in the Lopskin announcement. Here, in order to deduct non-net profit, non-recurrent profit and loss need to be deducted). It is still a mystery that the performance commitment is not less than 10.5 million yuan, 11.05 million yuan and 11.6 million yuan respectively.

The scale of related party transactions has been further expanded.

It is worth noting that this is not the first time that Lopkins' high premium acquisition involves related party transactions. In 2020, the company bought an 80 per cent stake in Zhongyifeng Technology for 193 million yuan, forming 143 million goodwill. This time, the value-added value of Lopskin acquisition founder is 42.9673 million yuan, and the value-added rate is 93.14%.

It is understandable for listed companies to increase business diversity through mergers and acquisitions. However, at a time when the performance has just improved and the acquisition of Zhongyifeng Technology has not been fully digested, it has opened the acquisition that the other party is testing. With such frequent mergers and acquisitions, can Lopskin, whose market capitalization is only 3.2 billion yuan, stand it?

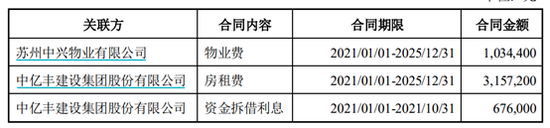

In addition, with the completion of this acquisition, the scale of Lopskin related party transactions rose instead of falling, with a further increase of 4.8676 million yuan.